After a somewhat worrying October report, November’s labor market data shows lower recession risk.

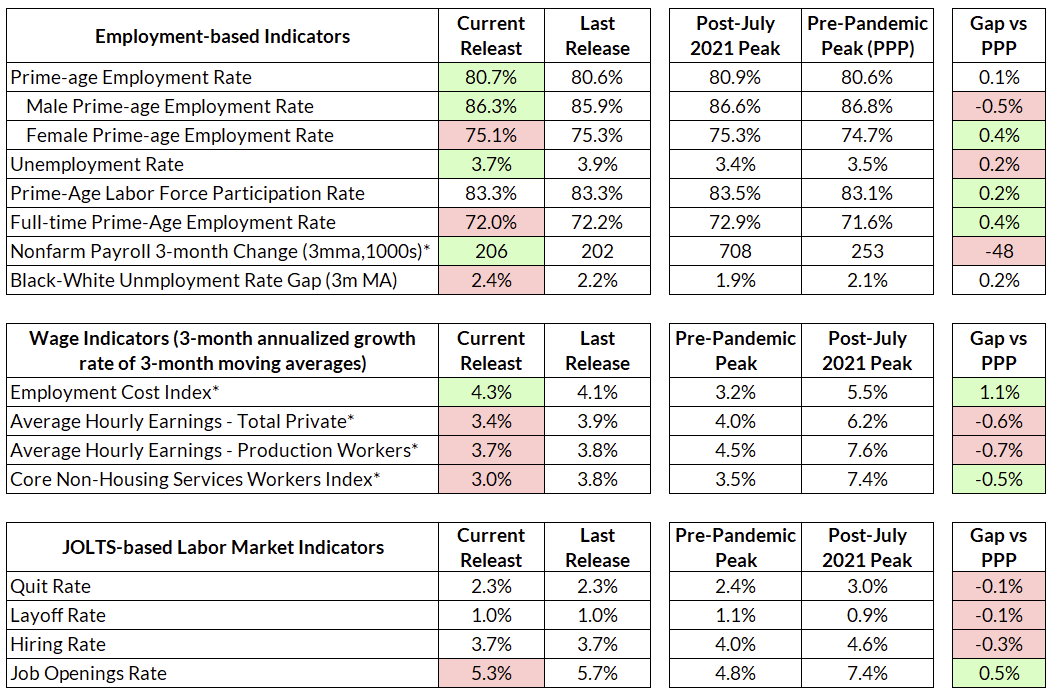

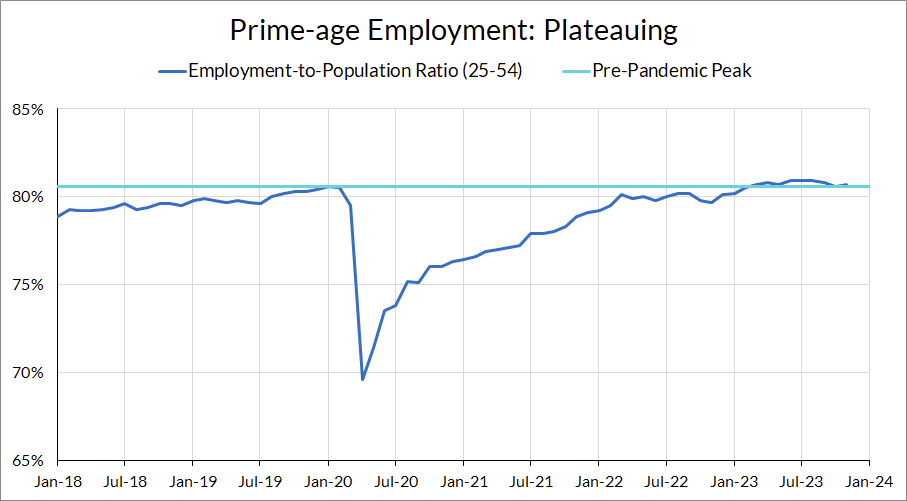

The headline unemployment rate fell to 3.7% from 3.9%, and the establishment survey showed 199,000 jobs added in November, with slight downwards revisions of 35,000 to both September and October. After a somewhat worrying October report, which put us on “Sahm rule watch,” November’s report offers some relief with improvement in the household survey numbers. Prime-age employment employment rates, which have been plateauing, ticked upwards to 80.7% from 80.6%. On the wage front, monthly wage growth came in relatively strong, with average hourly earnings growth for overall private workers at 4.3% annualized and 5.0% for production workers. Wage growth in core non-housing services—where the Fed claims to be most concerned about wage-price pressures—fell to just 3.0% on a 3-month basis. JOLTS indicators were mostly unchanged, with quits, hires and layoffs moving sideways, and job openings falling.

Overall, there isn’t anything too interesting from November’s labor market data. For supporters of full employment, the Fed, and people generally looking to avoid a recession, that’s a good thing. The economy continues its path of deceleration and normalization even as the labor market remains intact.

Labor Market Dashboard: November 2023

Stepping Away from the Edge

With last month’s increase in the unemployment rate, I wrote that the slowdown in the labor market should be cause for concern that the risks have shifted further towards unemployment. While that general trend remains, the most recent labor market data show some relief from that risk.

The headline unemployment rate fell to 3.7% from 3.9%. Most of the improvement in the headline numbers came from non-prime-age workers, with large gains in the 16-24 age category. The improvement in the prime-age category is less sanguine, but thankfully does not show a decline as feared. The prime-age unemployment rate remained constant at 3.2%.

After declining last month, prime-age participation rates moved sideways in November:

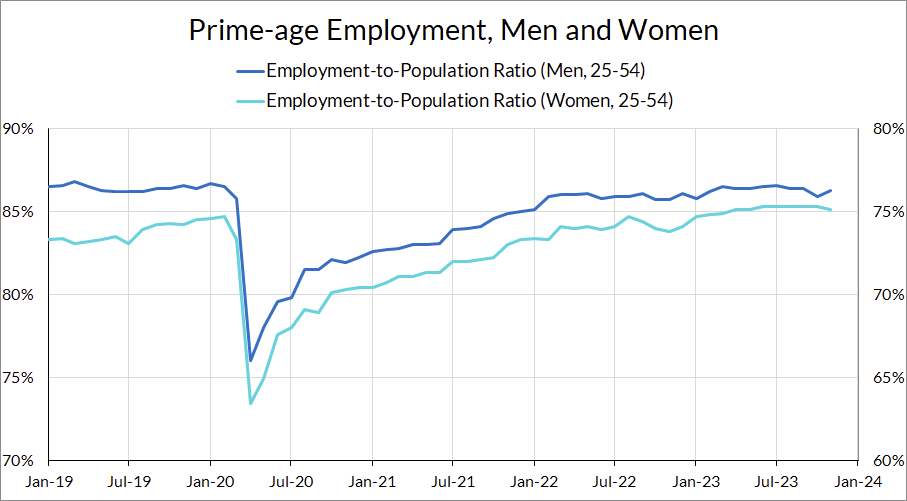

For the first time in a year, prime-age employment for women fell, from 75.3% to 75.1%. Meanwhile, prime-age employment rose to 86.3% from 85.9% for men. These changes are modest, but they undo the rise (decline) of employment for women (men) over the past six months. The larger story still shows a better employment recovery for women than men, with prime-age employment rates for men and women 0.4pp above and 0.5pp below pre-pandemic highs, respectively. Much of this improvement has been attributed to childcare support policies during the recovery. The flip side, of course, is that covid-era childcare support ended in September, prompting fears that the “childcare cliff” could lead to deterioration in women’s employment and labor force participation. While it is too early to tell, this could be the first sign of trouble that the end of childcare support will drag on employment outcomes for women.

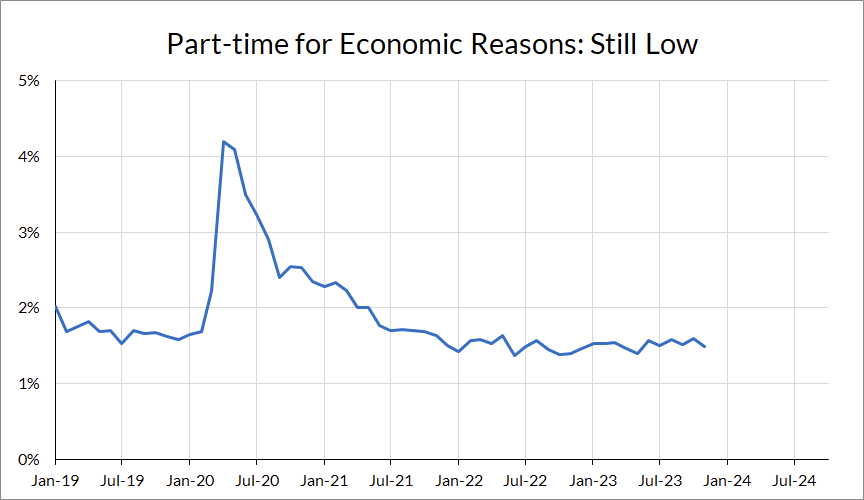

Besides the headline numbers, the details of the household survey also do not show any sign of concern that a recession is imminent. The number of part-time workers for economic reasons is still low, and the number of unemployed for less than five weeks (the household survey sign of layoffs) ticked down slightly.

November Wage Growth was Hot, but Core Non-Housing Services is Still Slow

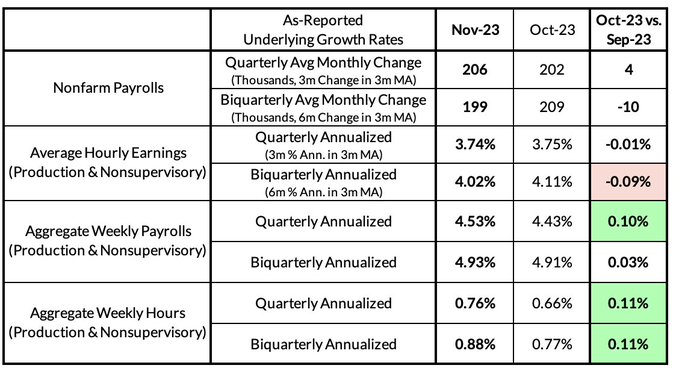

One stand-out in this month’s report was the relatively hot wage print. Average hourly earnings came in at 4.3% annualized in November, with wages for production workers coming in at 5.0%. Nevertheless, taking a longer and more smoothed view of wage growth still shows a clear deceleration.

Should the Fed worry about this? By Powell’s own statements, the reason why he might be concerned about wage growth is potential pass-through to prices specifically in the core non-housing services sector. Looking specifically at that sector, core non-housing service wages are growing very slowly now, with 12-month growth at 3.2% and the 3-month growth rate of the 3-month moving average a tad below 3.0%.

The average hourly earnings number can move around a lot month-to-month, so as always it’s good to take any one month’s print seriously. The important thing is that the overall trend for wage growth—especially in the sectors that the Fed claims to care about—is towards slowing.

Policy Risks and Implications

Overall, relatively to last month, not much has changed in the labor market. With unemployment backing away from triggering the Sahm rule, there’s marginally less recession risk. Job and wage gains are still solid and generally following a downwards trend.

What does this mean for the Fed? They like to talk about the “balance of risks” between unemployment and inflation. Relative to last month, the past few weeks of data have thankfully shown less risk on both fronts thanks to a lower unemployment rate and core PCE falling to sub-3.5% levels. While today’s report marginally reduces the chances for an earlier cut in 2024, the large drop in core PCE inflation takes precedence here.