Labor Market Recap: The Risks are Shifting

The labor market is really softening now.

The labor market is really softening now.

The labor market is really softening now.

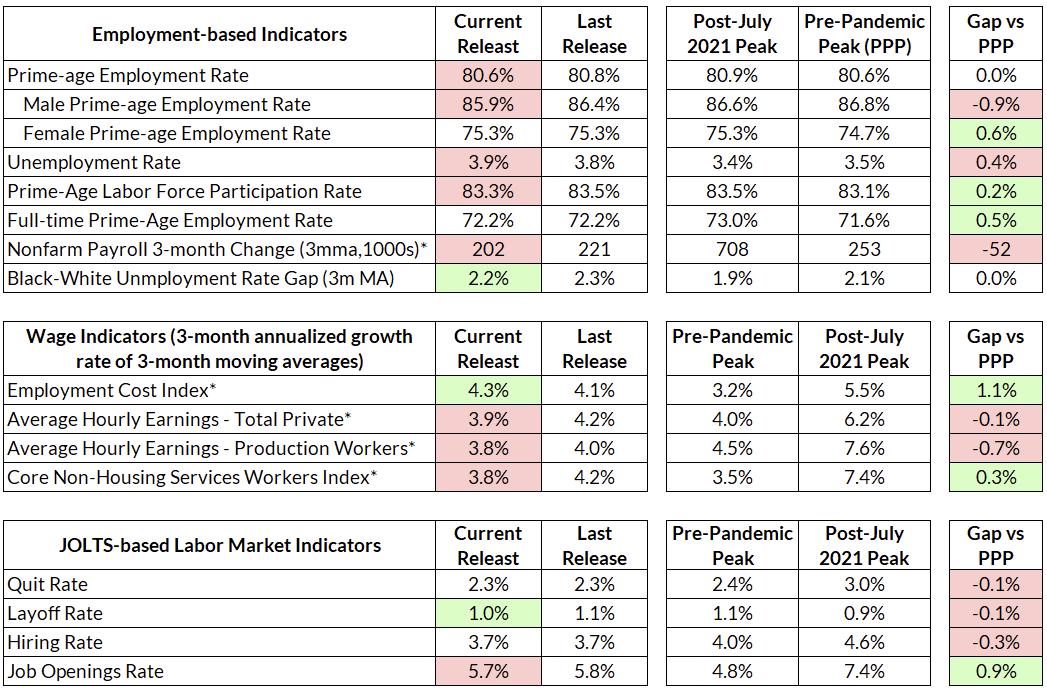

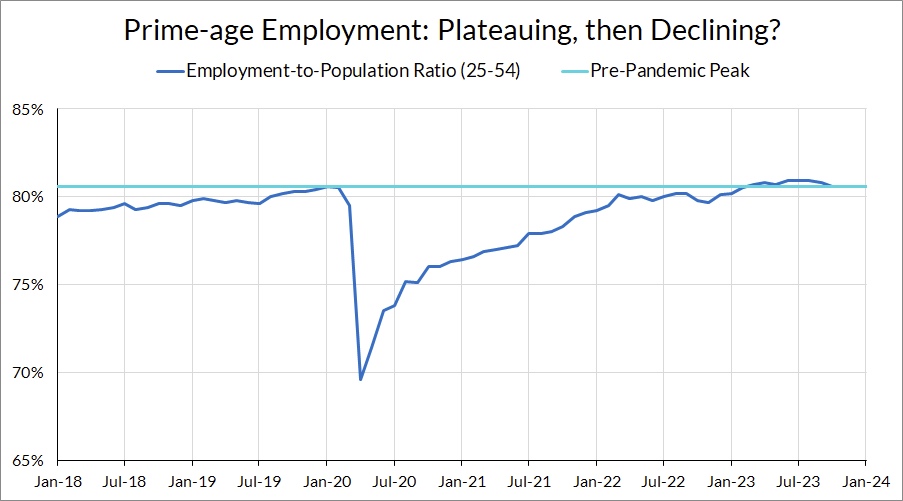

The headline unemployment rate increased to 3.9% from 3.8%, and the establishment survey showed 150,000 jobs added in October, below consensus—alongside downward revisions of 62,000 and 39,000 jobs in August and September. A large part of the slowdown in the nonfarm payrolls was attributable to strike activity (an increase of 30,400 this month according to the BLS’ strike report data), but the poor performance in employment showed in the household survey as well. Household survey measures of employment declined, with prime-age employment falling from 80.8% to 80.6% (its pre-pandemic peak), driven almost entirely by a fall in men’s prime-age employment. After a somewhat warm ECI print earlier this week (covering Q3 2023), average hourly earnings growth slowed a touch in October.

Three takeaways from this month:

For months now I’ve been describing the labor market as “strong, but slowing”, then “slowing, but strong.” Now, with slower payrolls growth, an outright decline in employment rates, and an increase in the unemployment rate to 3.9%, the labor market is noticeably weaker.

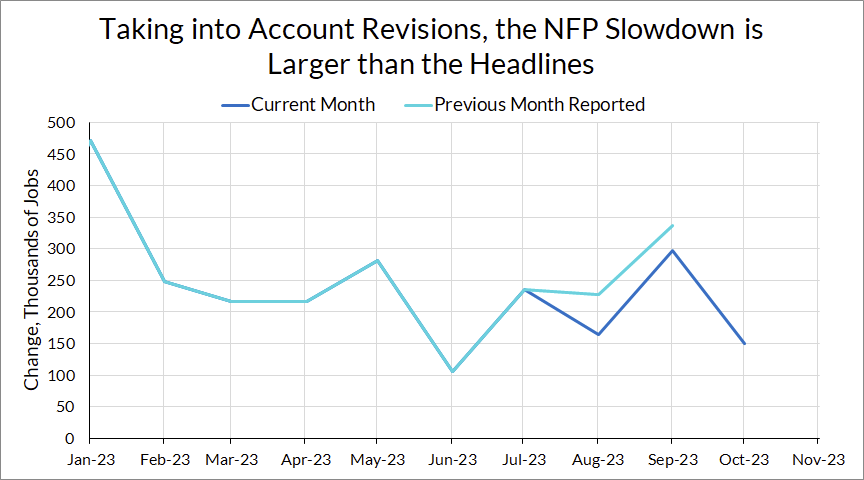

The headline nonfarm payrolls number disappointed, but looking through the revisions, the story is even worse. Payrolls for August and September were revised down, and the apparent reacceleration over the past few months has largely vanished.

These revisions largely took place in the government and leisure and hospitality sectors.

Change in Employment, 1000s | Current Release | Previous Release | Revision |

August | |||

Leisure and Hospitality | 8 | 44 | -36 |

Government | 51 | 50 | 1 |

Other | 106 | 133 | -27 |

Total | 165 | 227 | -62 |

September | |||

Leisure and Hospitality | 74 | 96 | -22 |

Government | 51 | 73 | -22 |

Other | 172 | 167 | +5 |

Total | 297 | 336 | -39 |

One unknown going into this report was how various strikes (most noticeably by the UAW and SAG-AFTRA) would affect the payroll numbers). According to the BLS, 48,100 employees were on strike in October, an increase of 30,400 from September.

That might give some comfort to the headline nonfarm payrolls number, but the weakness in job growth shows up in the household survey as well (striking workers are still counted as employed in the household survey). First, prime-age employment has turned from plateauing to declining, and is now matching, not beating, the pre-pandemic peak.

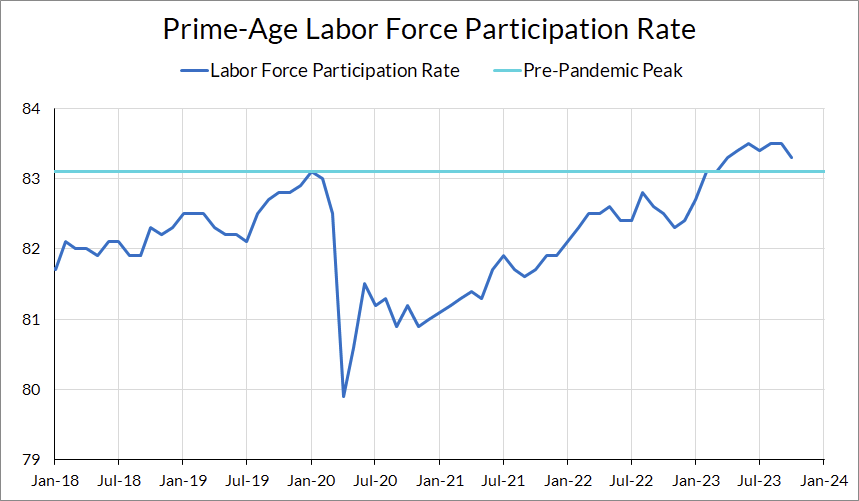

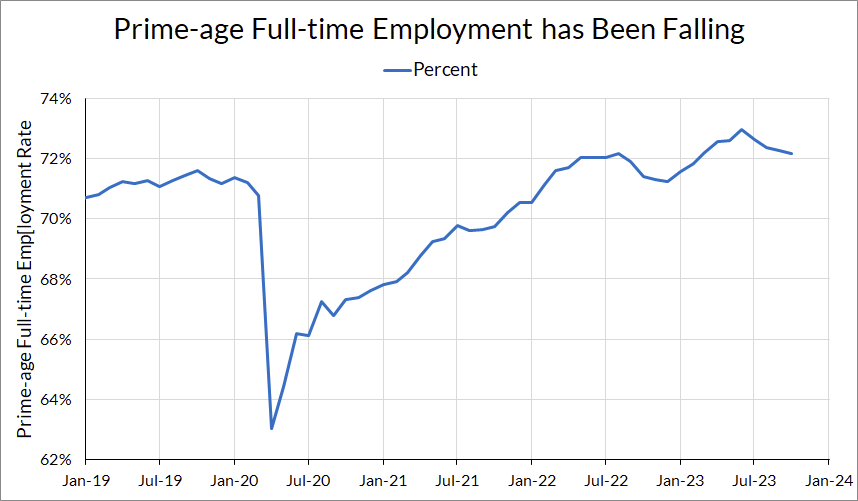

Labor force participation and full-time prime-age employment have also declined:

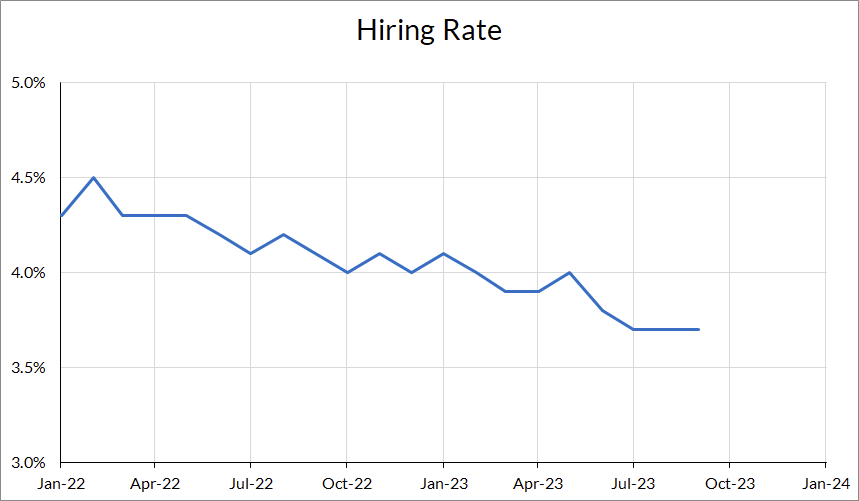

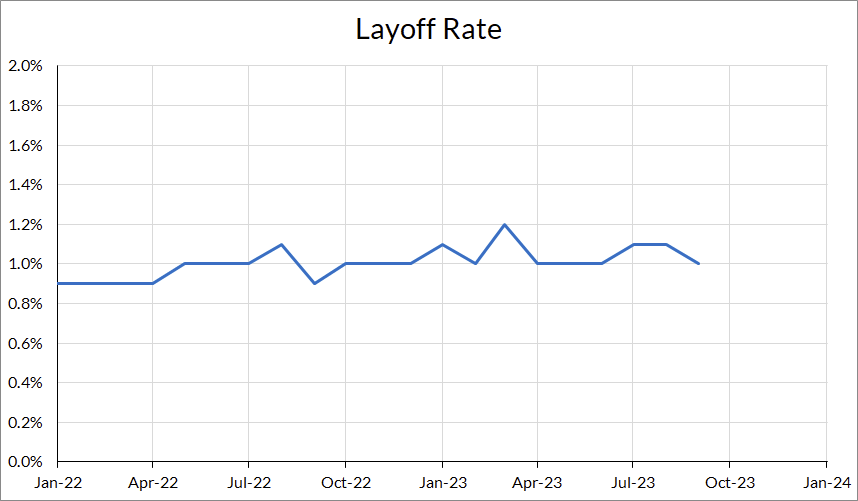

The weakness in the labor market appears to be coming primarily from a decline in hiring, not layoffs. While the headlines are largely dominated by high-profile layoffs, the aggregate data shows a large slowdown in the hiring rate, while the layoff rate has been largely unchanged since the beginning of this year.

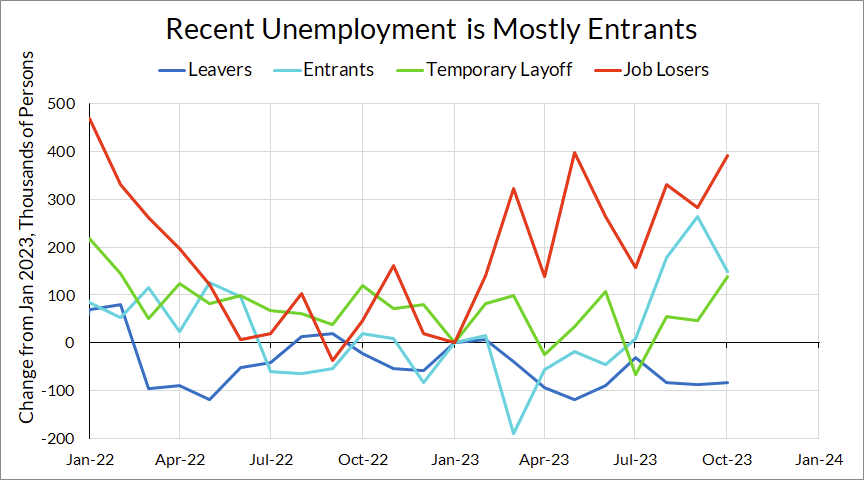

For another perspective, one can look at the composition of unemployed people. Over the course of 2023, there was a mild increase in layoffs, primarily in white collar jobs. That dynamic has mostly stabilized since the early part of 2023, but over the past six months the increase in unemployed people is coming mostly from an increase in unemployed labor market entrants and reentrants.

As I’ve written about before, the trajectory of unemployment and employment are driven as much by declines in hiring as they are by layoffs. On one hand, the absence of an obvious wave of layoffs is heartening, as recessions often begin with a short-lived wave of layoffs. However, lack of layoffs does not preclude recession; historically speaking, the primary driver of unemployment increases is a fall in the hiring rate. The recent rise in unemployment is a direct example of that.

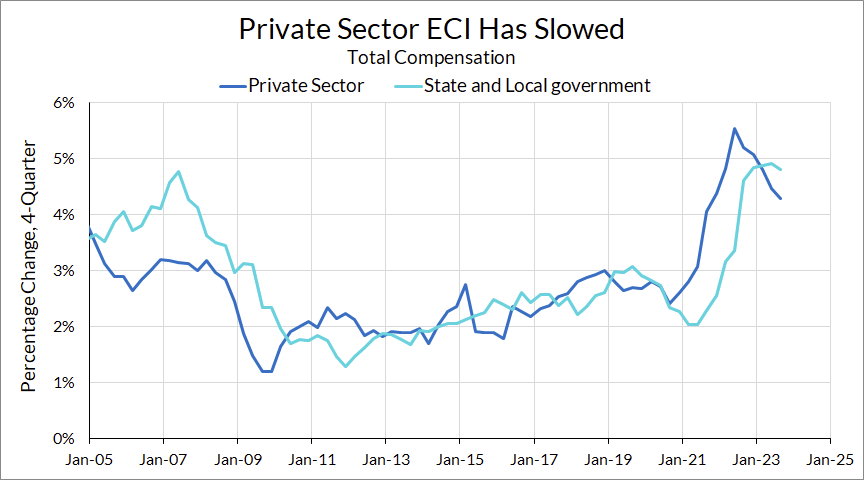

On the wage growth front, wage growth continues to slow. ECI came in somewhat warm in Q3 2023, but this was mostly driven by higher wage growth in state and local government jobs, which traditionally lag private sector wages.

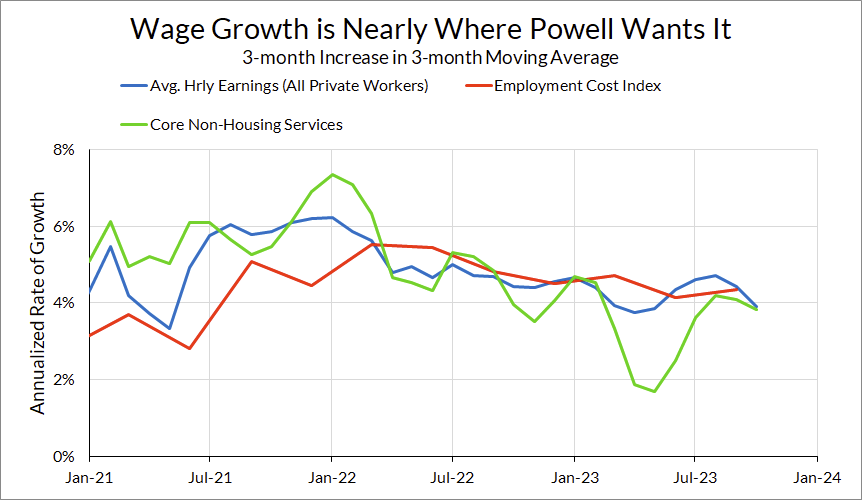

The 3-month growth rate in the 3-month moving average of average hourly earnings is now just under 4.0% for private workers, production workers, and the core non-housing services sector.

Last month, I made reference to statements Powell made to the concept of “wage growth consistent with inflation.” He’s suggested that wage growth should be approximately equivalent to inflation plus productivity growth. At the November FOMC press conference, he put some more specific numbers on this idea: he sees trend growth at “just around 2 percent”, which would put the wage growth number at 3.5% given a 2% inflation target and a 0.5% adjustment for trend population growth. In other words, wage growth is very close to where Powell’s rule would dictate. Our view is that it’s possible that productivity outperforms as churn falls and people get settled into their new jobs, in which case the current level of wage growth is entirely appropriate and consistent with 2% inflation.

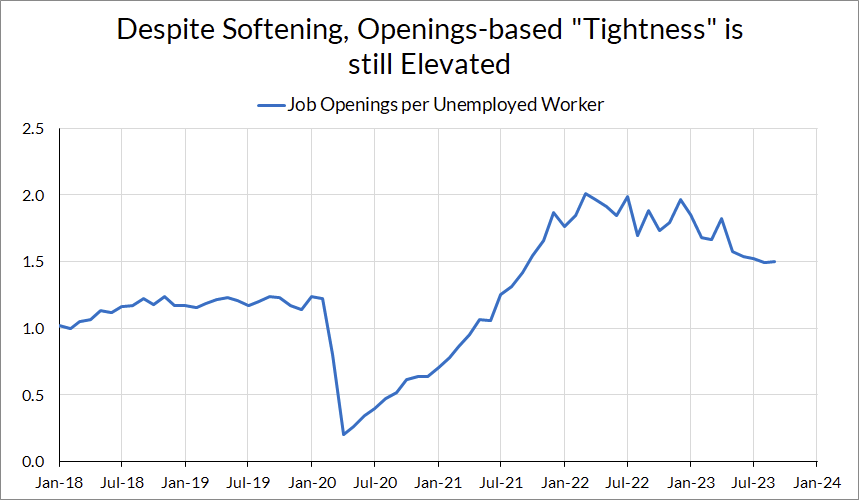

All of this has happened while the job openings rate is still elevated over its pre-pandemic level. As we’ve flagged many times before, relying on this indicator was a mistake due to measurement issues and secular increase in the job openings rate over time. As of now, the job openings rate, while lower than its peak, is showing a much tighter labor market than other indicators.

Thankfully, Powell has started to back off from his emphasis on the job openings numbers. In his speech at the Economic Club of New York in October, he brought up a larger variety of labor market indicators, such as soft data, the job switching premium, and the quits rate, to point out the softening in the labor market so far.

At face value, the labor market is still doing well by historical standards. 3.9% is still a low unemployment rate, we’re at the pre-pandemic peak for prime-age employment, and layoffs are low.

As for the Fed, it’s fair to say the labor market is basically where they want it:

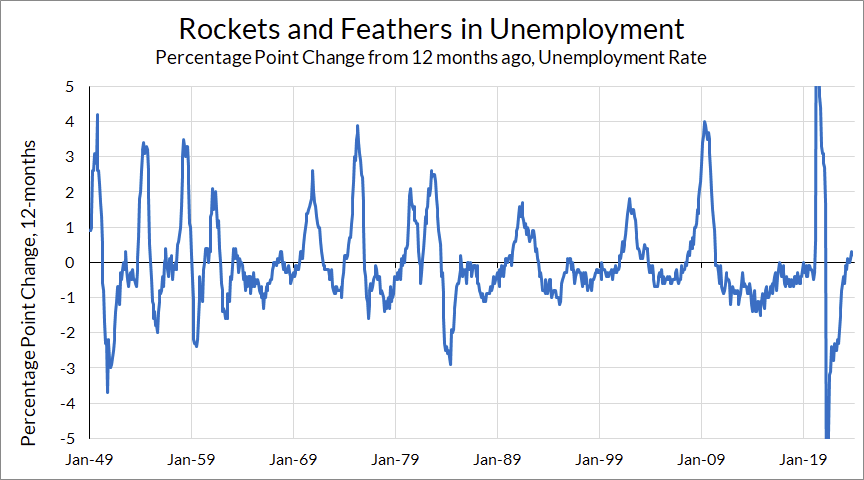

All of these dynamics are things that Powell has explicitly said the Fed is looking for. The scary thing isn’t where we are now, but where we might be going—and the momentum is in the wrong direction. As of now, the Fed’s goal is to achieve a slight softening of the labor market without unemployment spiraling out of control.

Historically speaking, this would be unusual. Unemployment tends to increase very rapidly, very quickly, and then decline slowly over a longer period of time. Long periods of slight increases in unemployment are very rare.

That’s not to say it’s an impossibility—if there were ever a time for unprecedented events in the labor market, it would be this episode. The point is, this month’s jobs data should be cause for alarm at the Fed, and should significantly shift their perception of the risks towards unemployment. This should be the end of Fed hikes for the rest of the year.