Causal Theme: The Cautious Case For Productivity Optimism

From the outset, I should say that I am a bigger skeptic of productivity data than most. Once you know how the sausage is made, you will be more skeptical of how it is typically served to customers. Nevertheless, I'm about to lay out three reasons, based on both fundamental and measurement considerations, why I see productivity data improving after the previous five quarters appeared so weak.

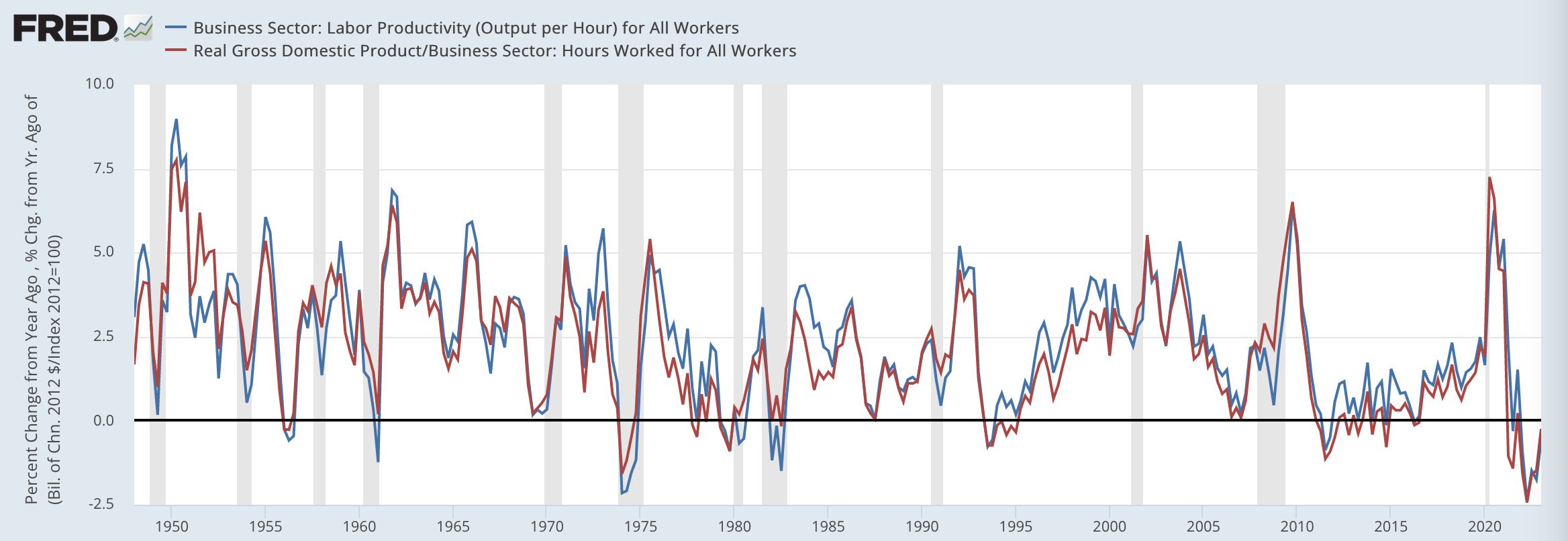

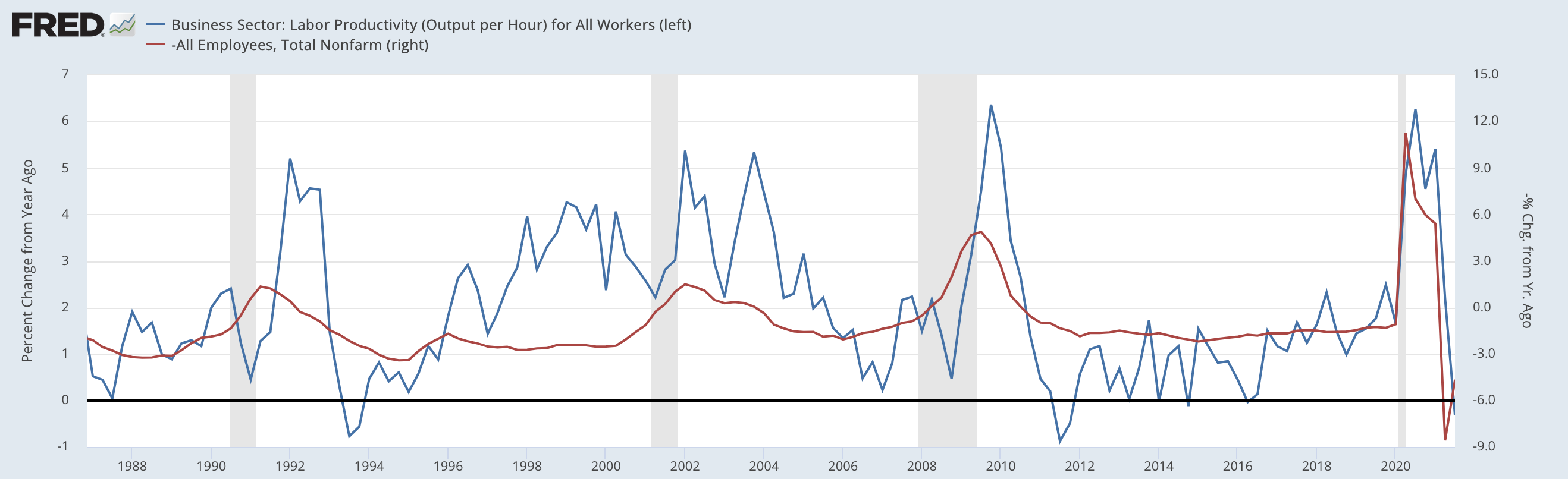

First, let’s take a look at what the productivity data is actually measuring – the everyday intuition that it measures “how productive” the average firm is is a poor guide to the structure of the measurements themselves. Productivity, as most commonly cited in economic reporting, is calculated by dividing total real output by total hours worked. Remember that hours worked is in the denominator; growth in hours worked, all else equal, lowers productivity. All else is obviously not equal, but for now let’s work through the behaviors of the relevant aggregates.

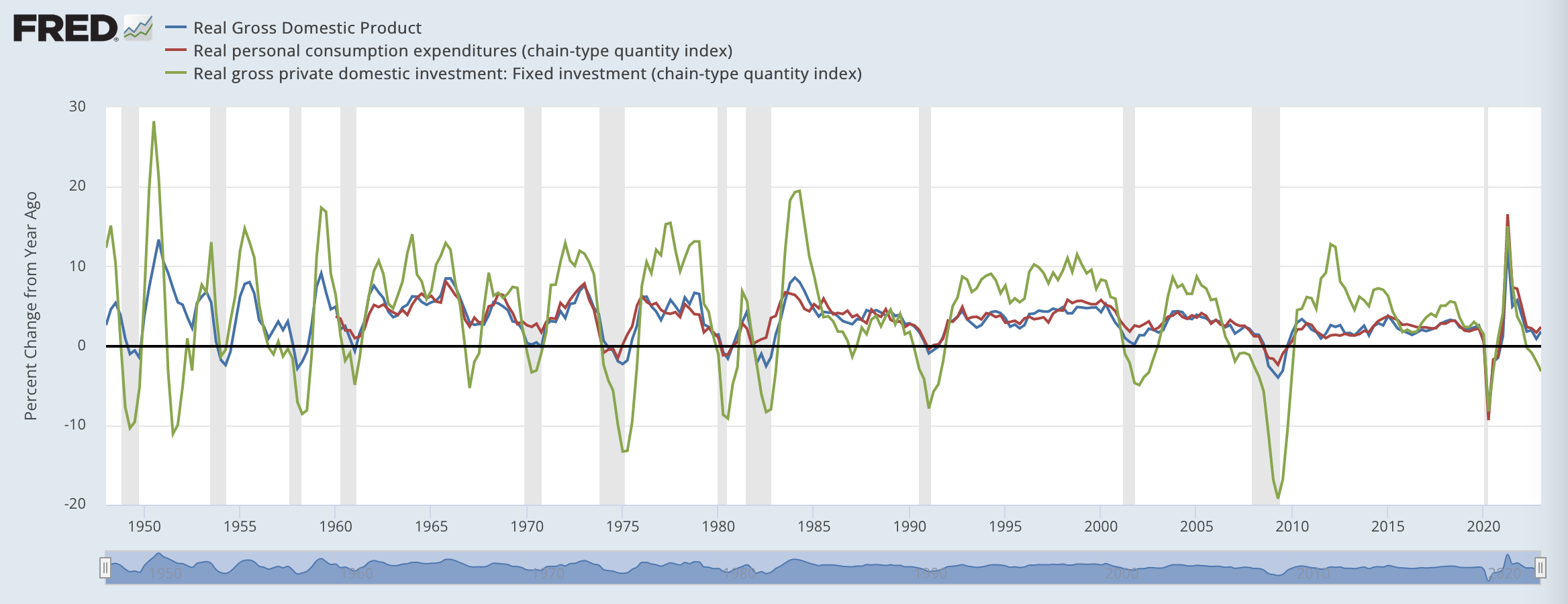

While most output serves a consumption purpose, output growth tends to vary as a result of more substantial variation in fixed investment growth, despite fixed investment comprising only 17% of GDP. Aggregate real consumption growth tends to be very smooth by comparison.

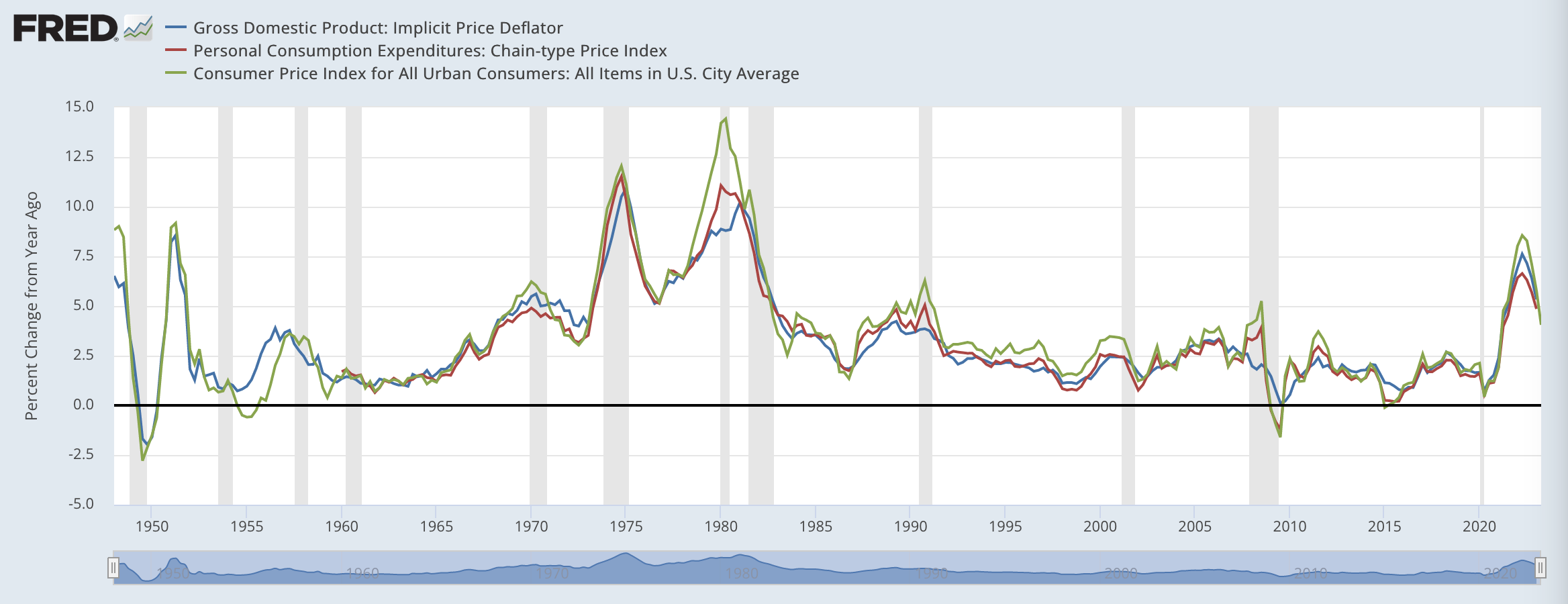

Real output is generally estimated indirectly, by first measuring total dollars spent/earned on a particular set of transactions and then dividing those dollars by a corresponding price index. So in that sense, inflation is negative for productivity, all else equal (again, all else is never equal).

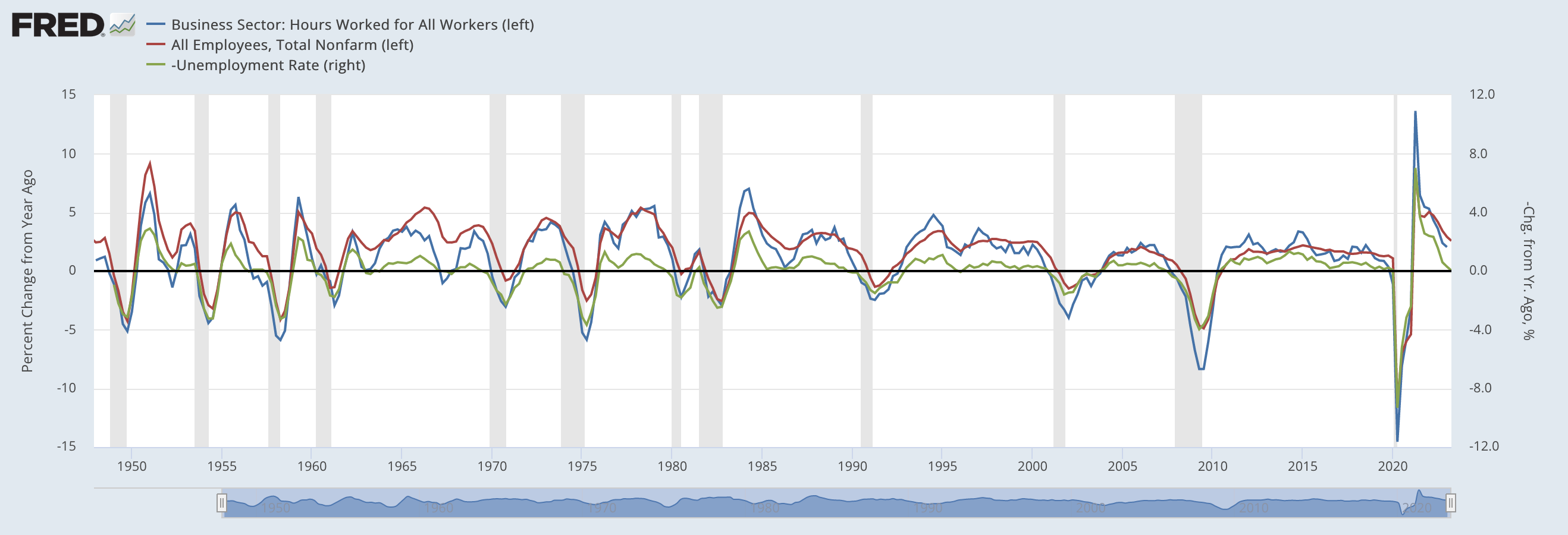

Hours worked tends to grow more cyclically with employment, which also tends to move with the business cycle.

An unfortunate aspect of the productivity estimates available to us is that they are both too-aggregated, and problematically aggregated from disjointed datasets. They do not track productivity at the firm, establishment, or production process level. Instead, the measurement involves an independent estimate of output and hours worked, divided only at the aggregate level. All of the problems associated with “composition bias” when dividing two aggregates are also present here; if lower value-add and lower-wage activities outperforms during a recovering phase of an expansion, productivity growth will slow. While employment and output generally correlate over long periods of time, there is no tight linkage in the data that says job X corresponds to output Y, especially over the lengths of time relevant to the pandemic and recovery.

It can take time for a newly employed person to contribute to output, especially in an economy that produces goods and services that are increasingly more complex than the simple "widgets" of macro textbooks. We should not expect rapid job growth to immediately yield rapid output growth. In the messy bullwhipped pandemic-affected economy of the past three years, real output and employment dynamics can substantially decouple for all sorts of reasons that have little to do with per se labor inefficiency.

As a result, jobs can easily be lost, as measured in various surveys, even as output may not fall so quickly. In the past four recessions, we have seen that productivity actually grows faster as a result of jobs lost.

Viewed in the correct light, productivity gains during recessions and jobless recovery periods (see 1992-93, 2002-03, 2010-11) can be seen for what they are: empty calorie productivity gains. The number goes up, but the real economic capacity the number is meant to measure is steadily falling. It's possible to suddenly squeeze more productivity while rapidly downsizing, but over time, capacity and productivity will ultimately dwindle without efforts to support investment in technology, capital, and labor. Any victory to be claimed here can only prove pyrrhic.

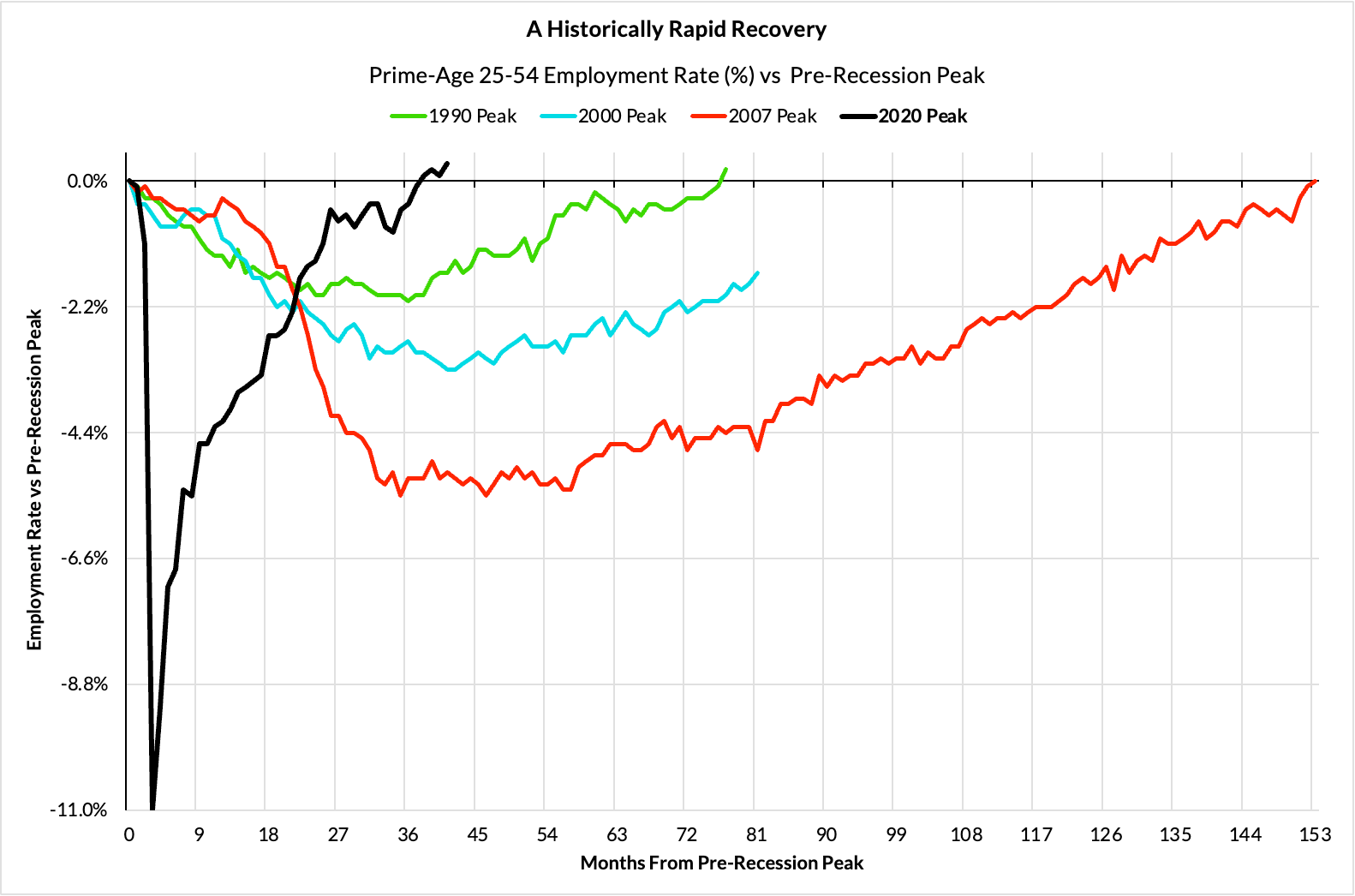

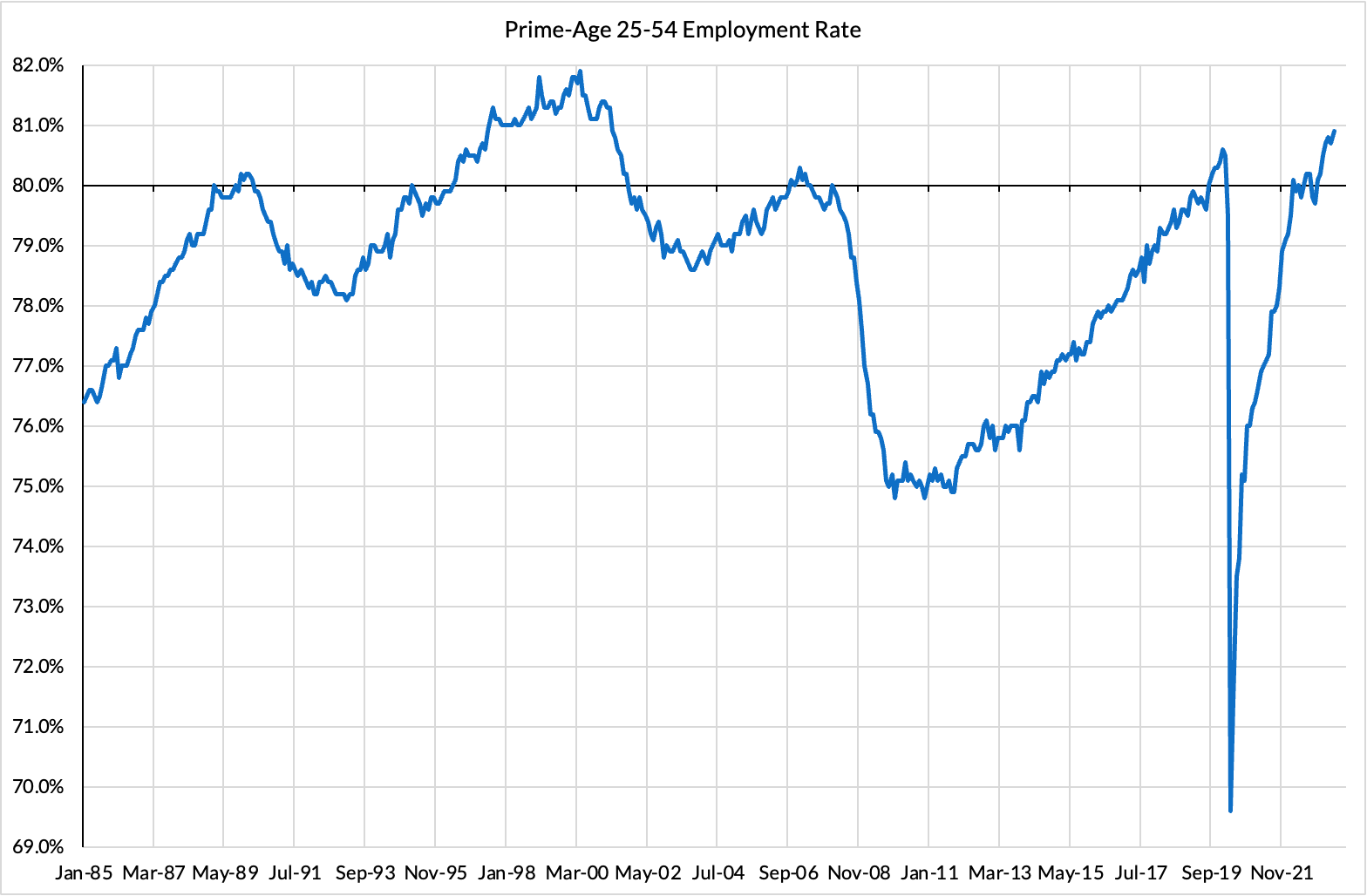

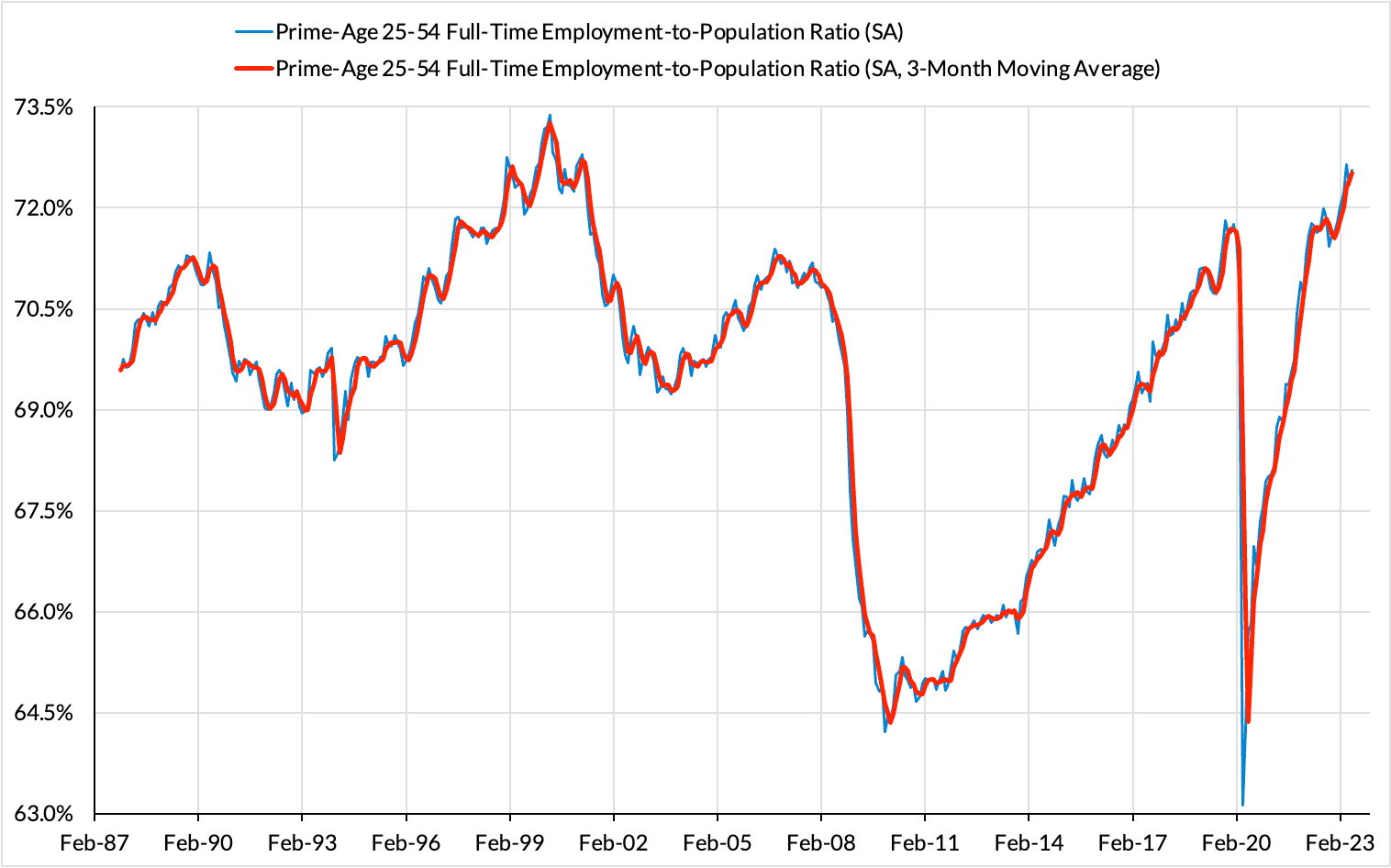

It should thus come as no surprise that productivity growth tends to be very weak when employment recoveries are in their early innings, still far from maturity. From 1994-96, productivity growth was under 1%. As prime-age employment rates incompletely recovered from 2004-2007, productivity growth decelerated back down from 3-4% back to 1%. And the slogging 2010s recovery, where prime-age employment rates took over a decade to fully recover, productivity growth was basically 1%. Speaking purely in terms of the dynamics of measured data in the short-run, there is a clear tradeoff between job growth and productivity growth in slack labor markets.

Rapid job growth can be partially "blamed" for weak productivity estimates in 2021 and 2022. Yet beyond the obvious welfare benefits associated with fully recovered employment, that recovery has now set the stage for the labor market to actually mature and develop. Rapid recoveries help avoid the loss of skills, and more time in a given job increases the scope for training and new skill acquisition.

Strictly from a data construction perspective, job growth normalizing to a steadier pace gives more room for the good kind of productivity growth to shine. The last time we really saw this dynamic was in the late 1990s. In this kind of economy, nominal and real wage gains are sufficient to support ongoing production of consumed goods and services, while real fixed investment growth can outperform and even accelerate, driving further job gains and defanging the recession threat.

Prioritizing a rapid jobs recovery as we did in 2020 is a natural reflex: it directly improved the welfare of American workers. But those first-order benefits are not the only ones. Appropriately managed labor markets come with a wide array of secondary benefits to a rapid recovery, including a more mature workforce.

For the past four quarters, real fixed investment has contracted, an outcome that would normally be associated with recession if taken at face value. Look under the hood and you'll find three key drivers.

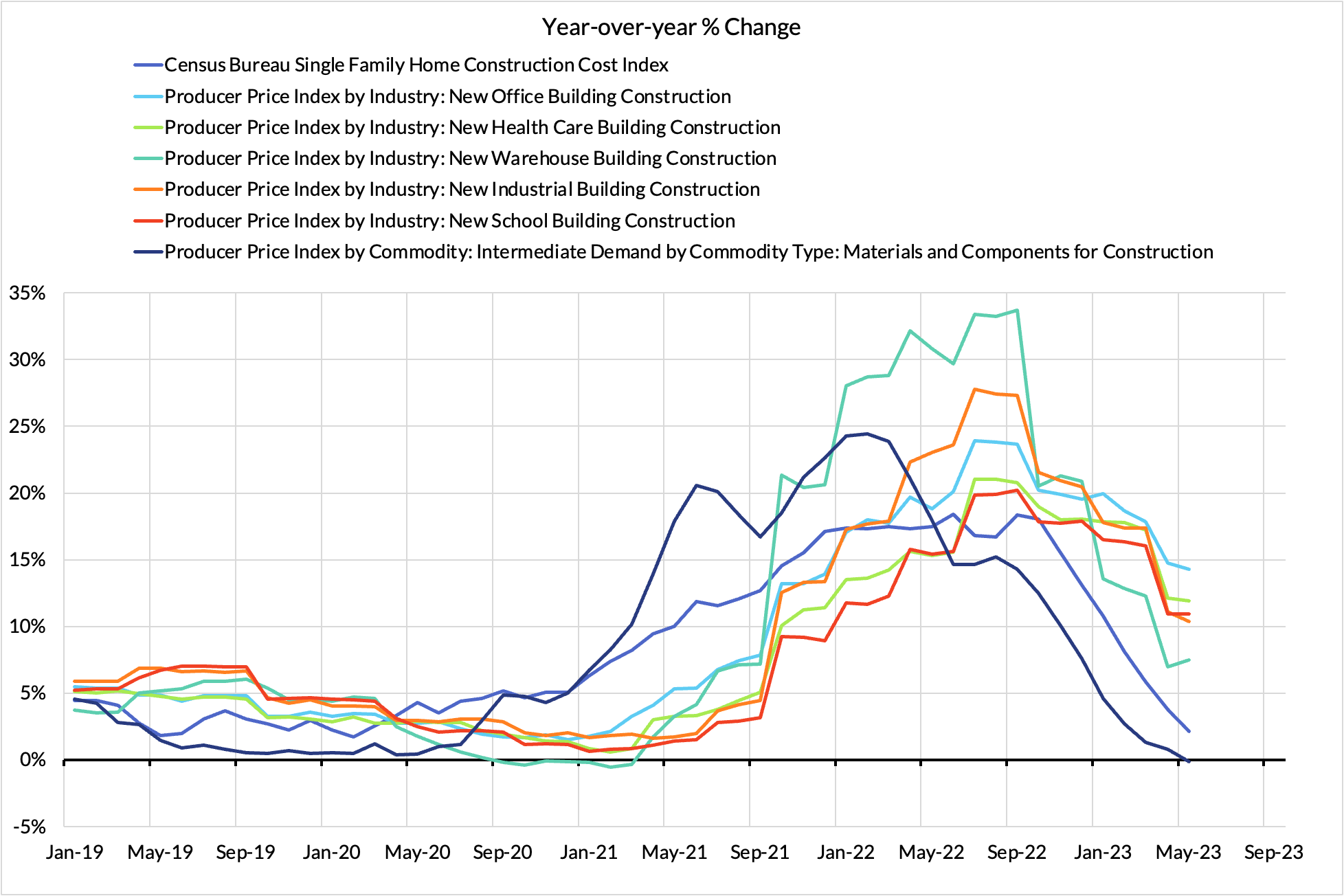

On all three points, things are clearly getting better now. Construction costs have been decelerating on a year-over-year basis and outright deflating on shorter-run metrics.

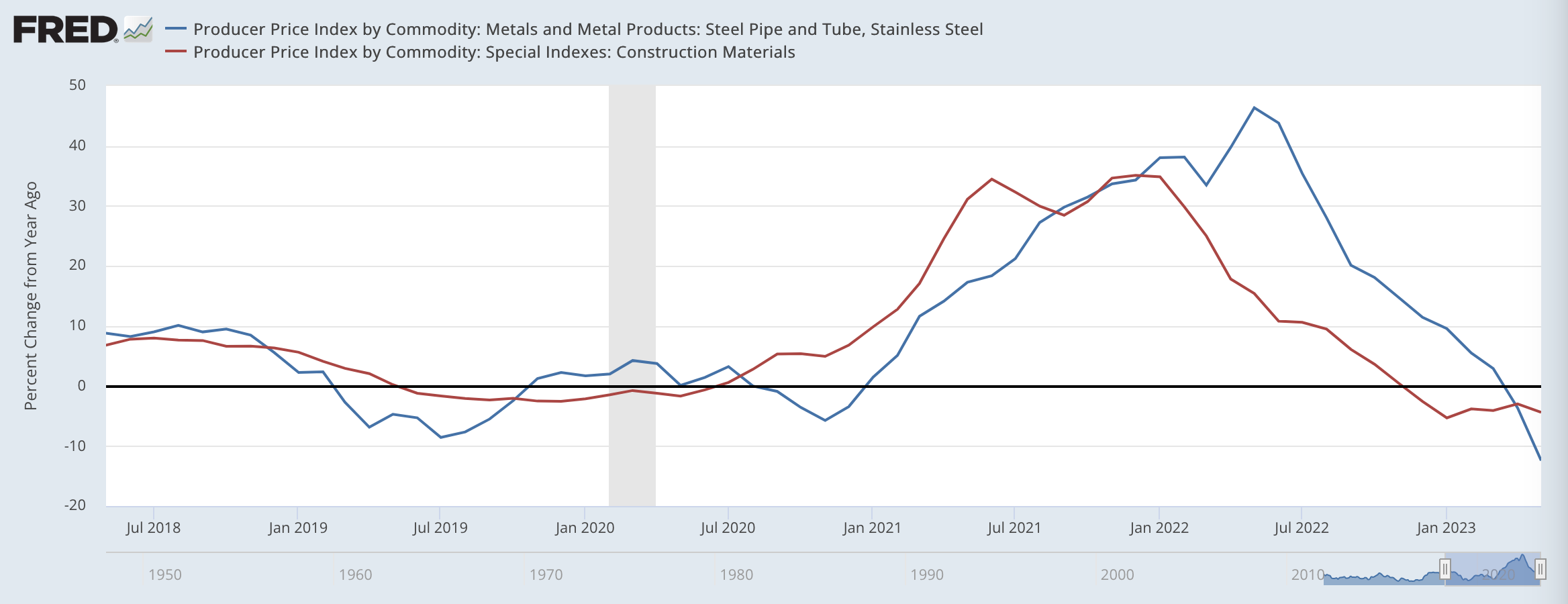

While much attention is given to labor costs, it was really the volatility in material costs that drove so much of the price pressure captured in these indices. The costs of steel, aluminum, cement, and sand have all shot up, and are only now beginning to deflate back from elevated price levels.

Much of this reflected the difficult challenge of scale in proportion to demand, but there were other factors underplayed during the initial phases of the surge. Global prices for aluminum and steel are largely set in China given their outsized share of global capacity. When China enacted "Olympic Blue" policies to curtail aluminum and steel production for the sake of lower pollution ahead of the Winter Olympics, supply and cost challenges in the domestic construction sector were likely exacerbated.

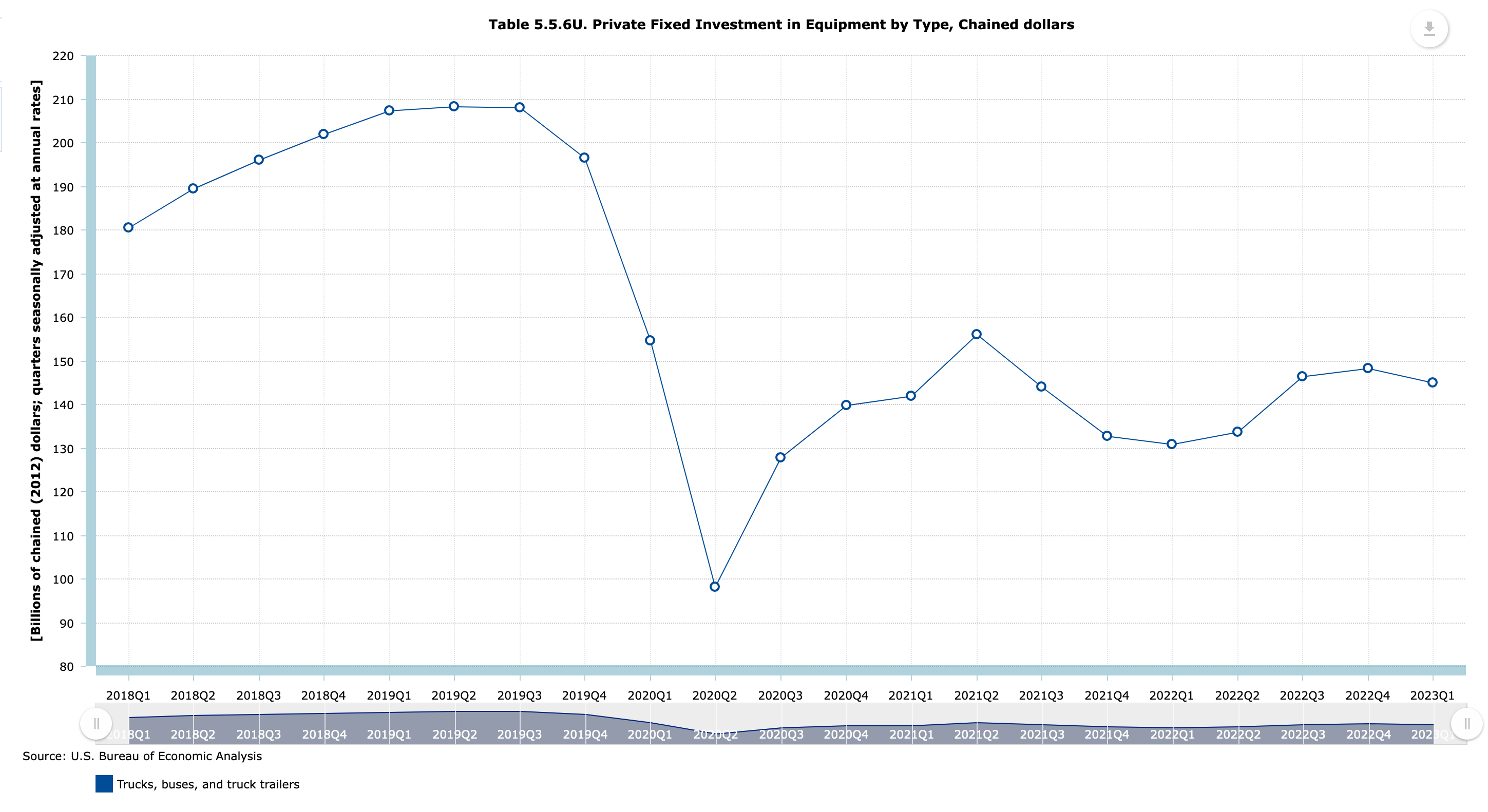

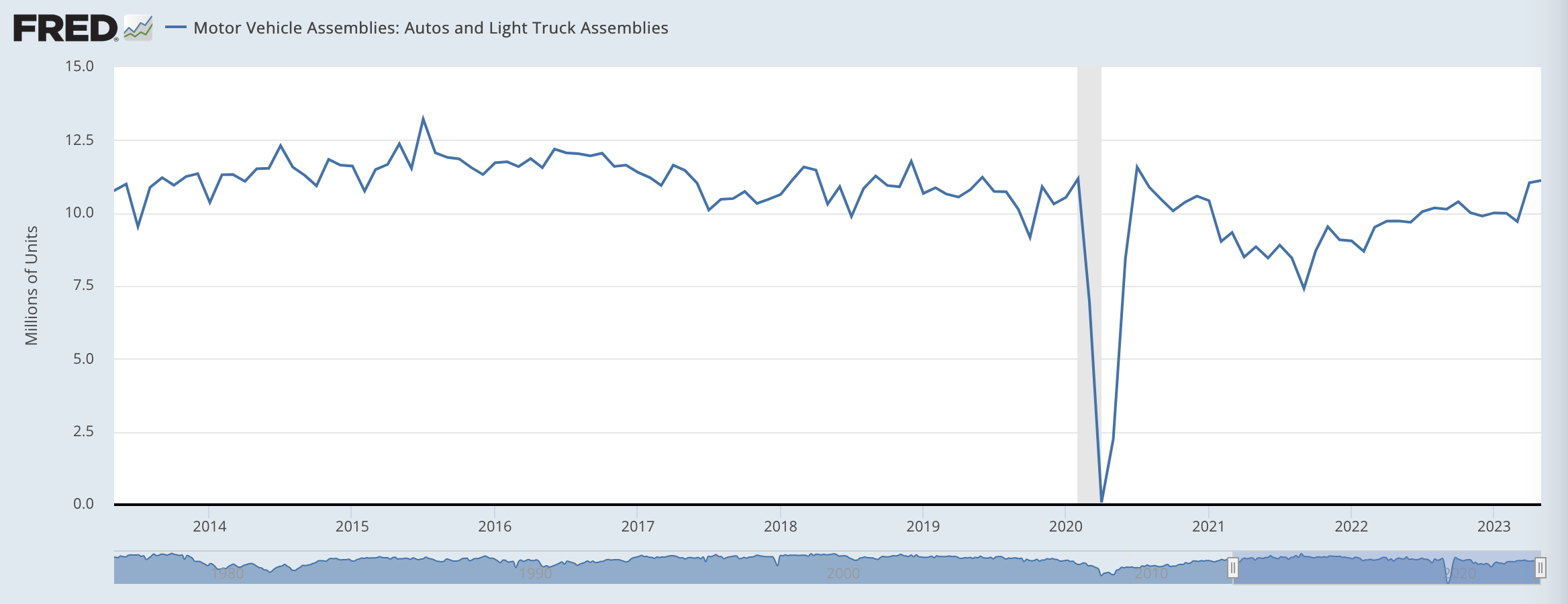

We have already written at substantial length about the implications of the (legacy) microchip shortage for motor vehicle production. While it might be an old story, it remains relevant because of its whipsawing effect on core inflation.

Only over the past couple months are we seeing improvement in motor vehicle assemblies back to pre-pandemic levels.

And if the cyclical trucking sector is providing any indication, it doesn't look like business demand for motor vehicle units and parts are slowing.

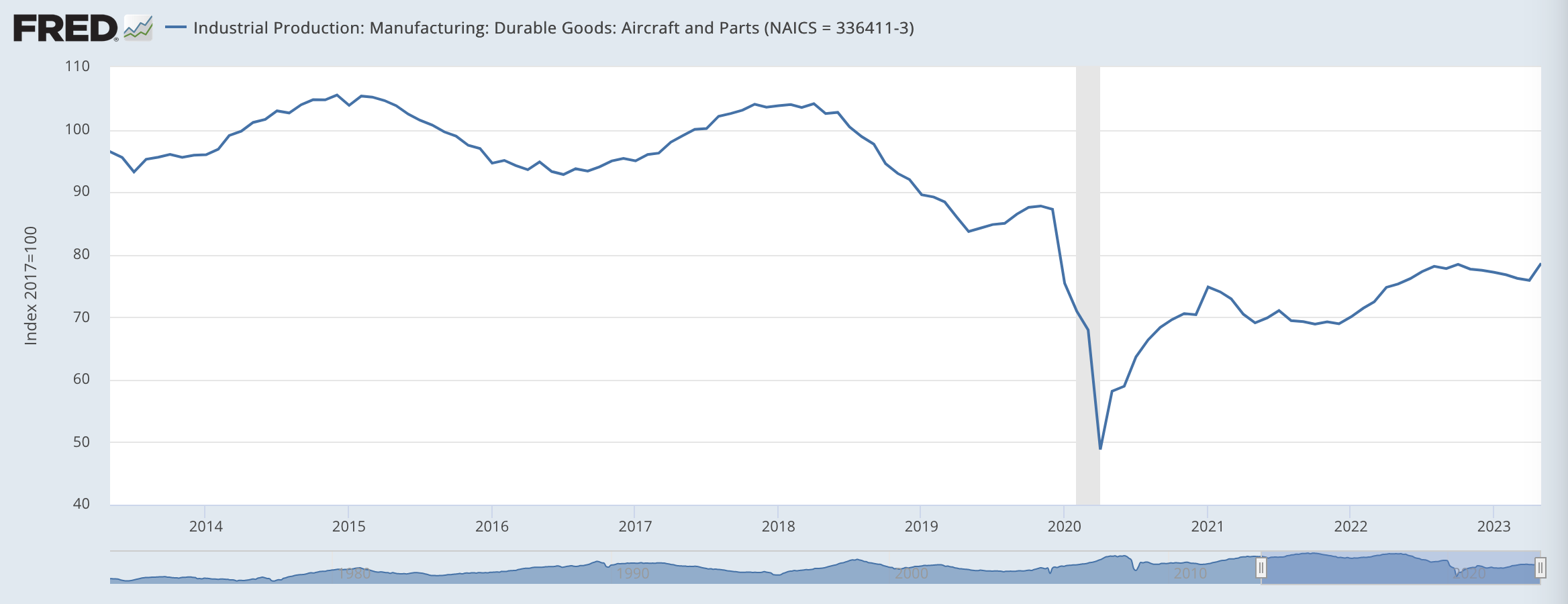

Aerospace production in the United States was suffering even before the pandemic hit due to Boeing-specific challenges with the 737 MAX.

But if you've been following aerospace industry color closely (and if you see the last spike in aircraft production in May), production is ramping up to deal as airlines play catch-up to air travel demand and Boeing. The runway for further aircraft investment is looking quite robust.

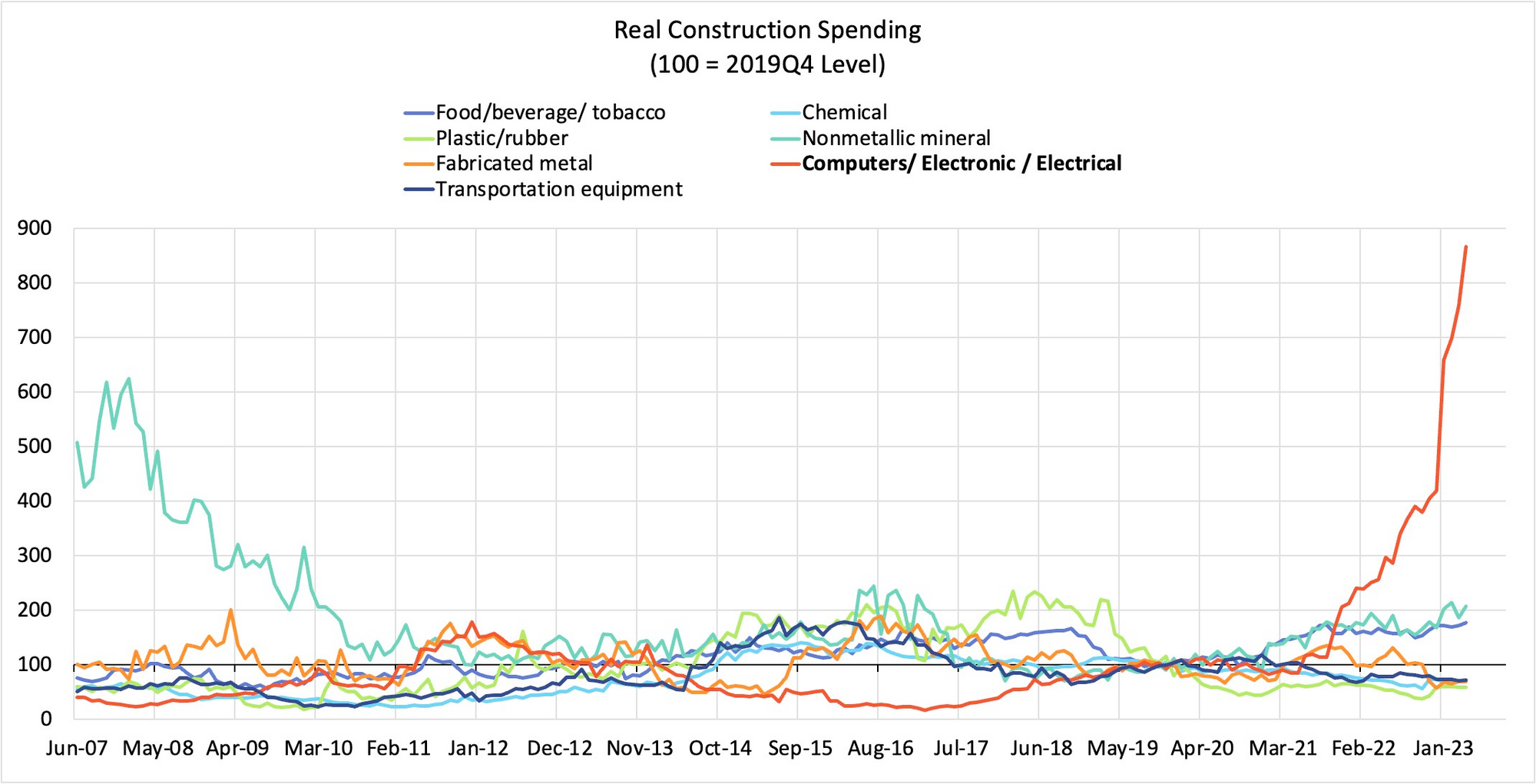

Finally, we would like to highlight the fact that the effects of IRA, IIJA, and CHIPS are beginning to meaningfully snowball and pull in more private fixed investment in the process. Nonresidential construction has undergone a substantial shift towards industrial and infrastructural end-uses and away from office, retail, and leisure sectors.

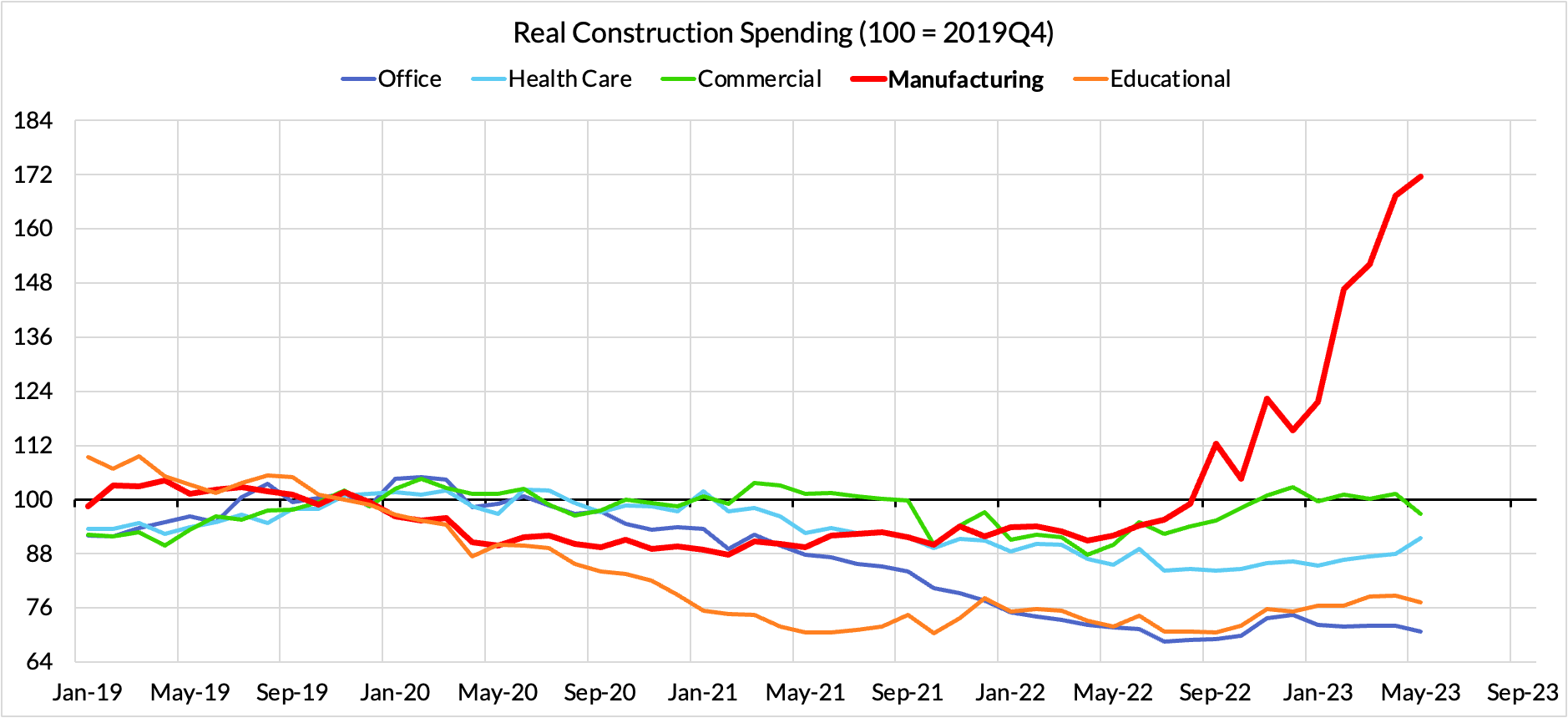

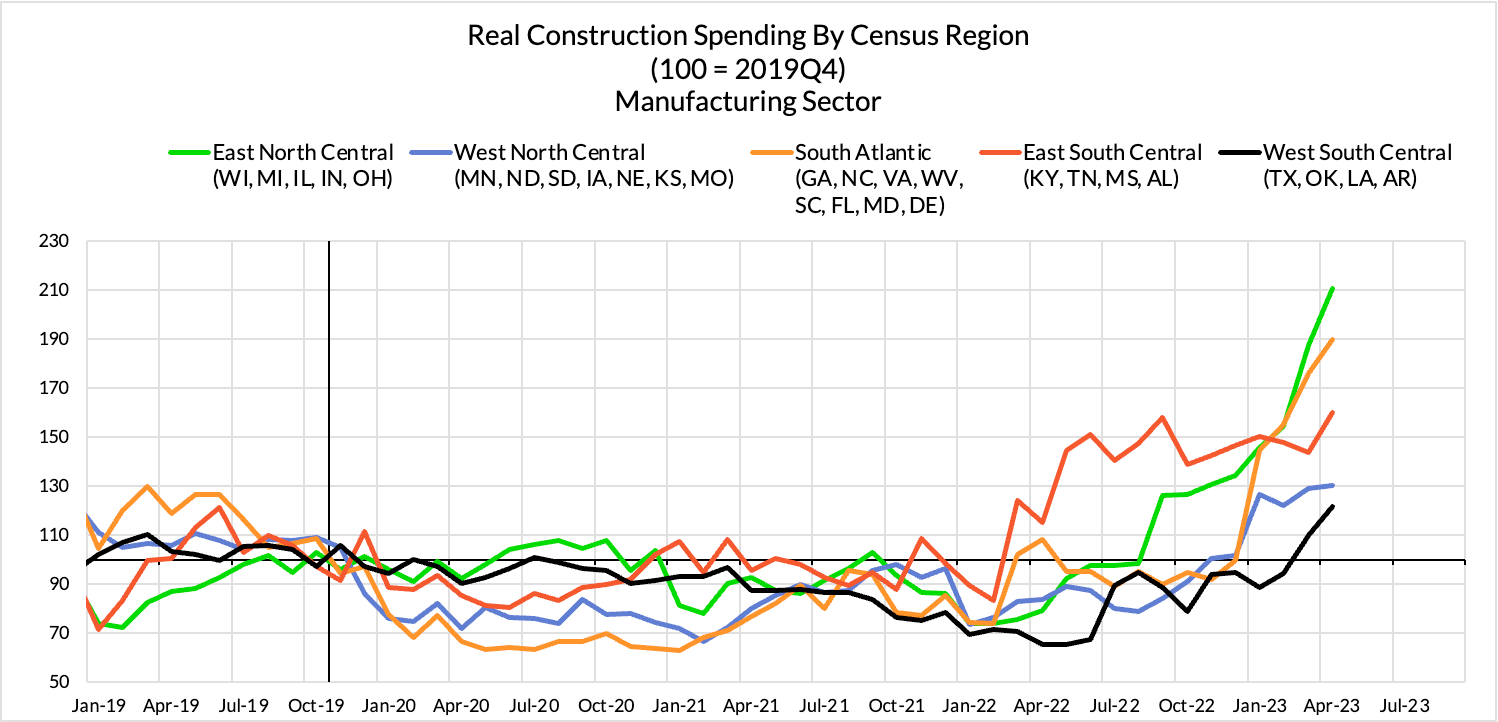

Construction spending for the manufacturing sector is in a historic boom even in inflation-adjusted terms.

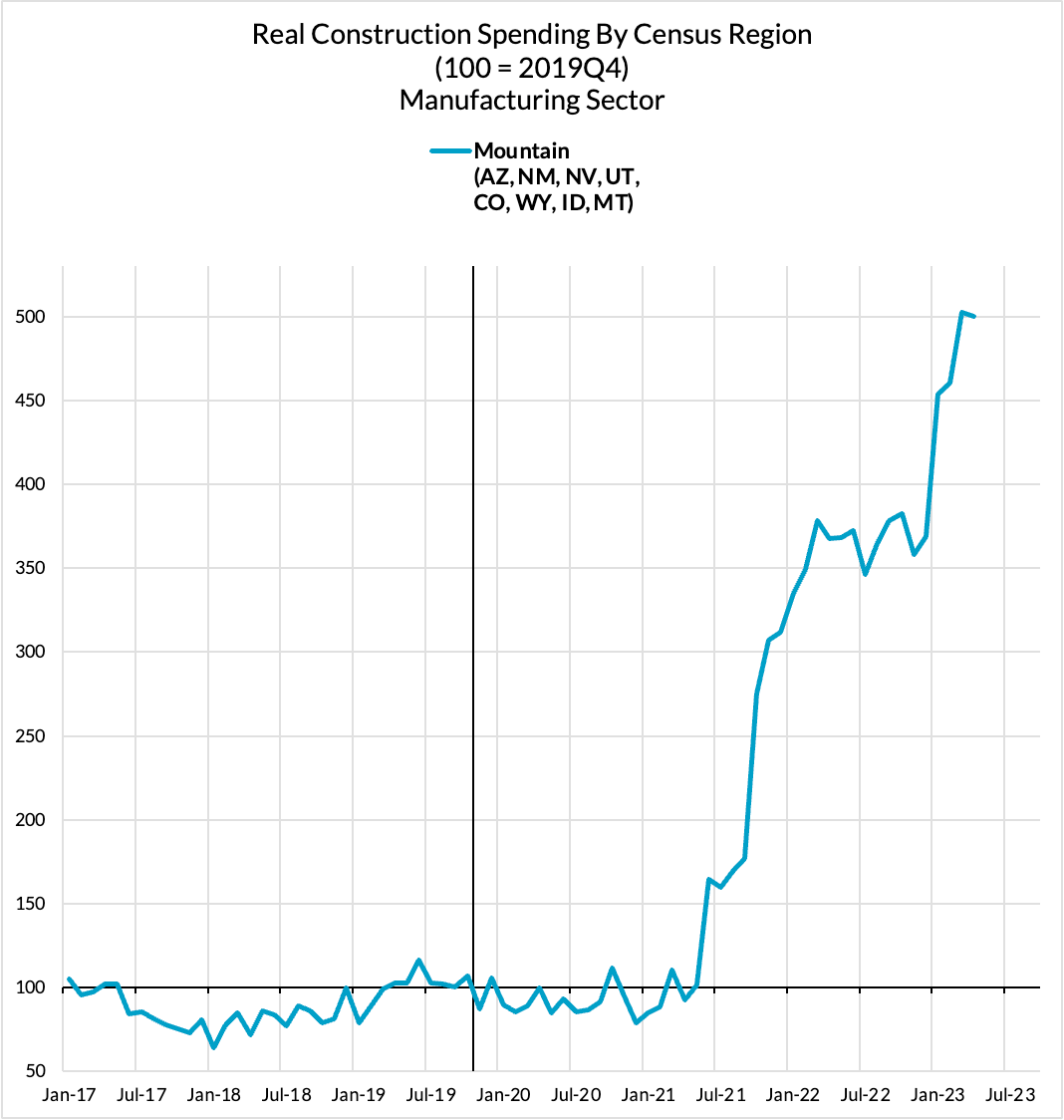

And if we look at the regional cross-sections, we see that fixed investment in manufacturing construction in the areas most relevant to CHIPS (Mountain West) and the IRA (battery and automaking investments in the midwest and sunbelt).

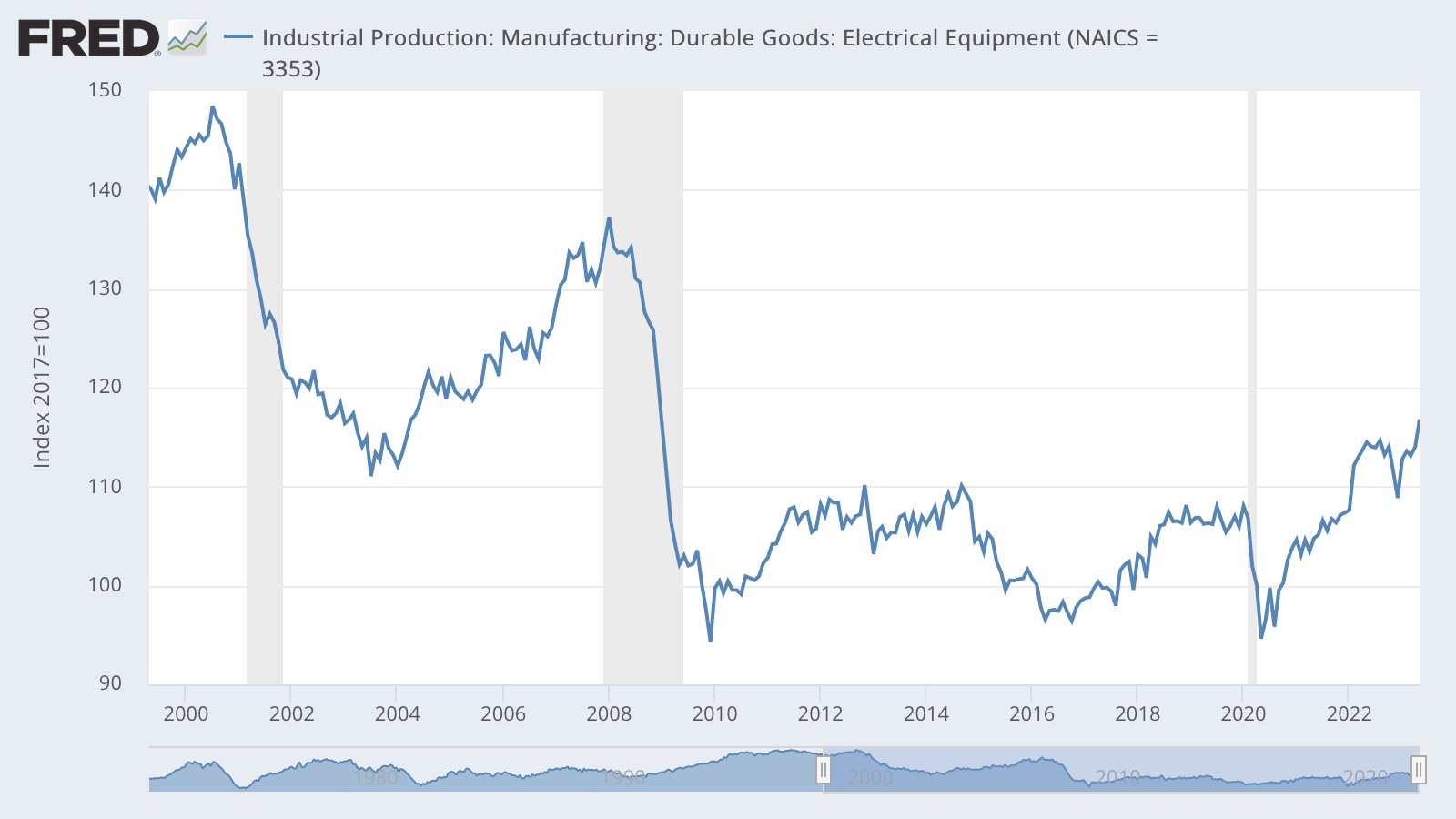

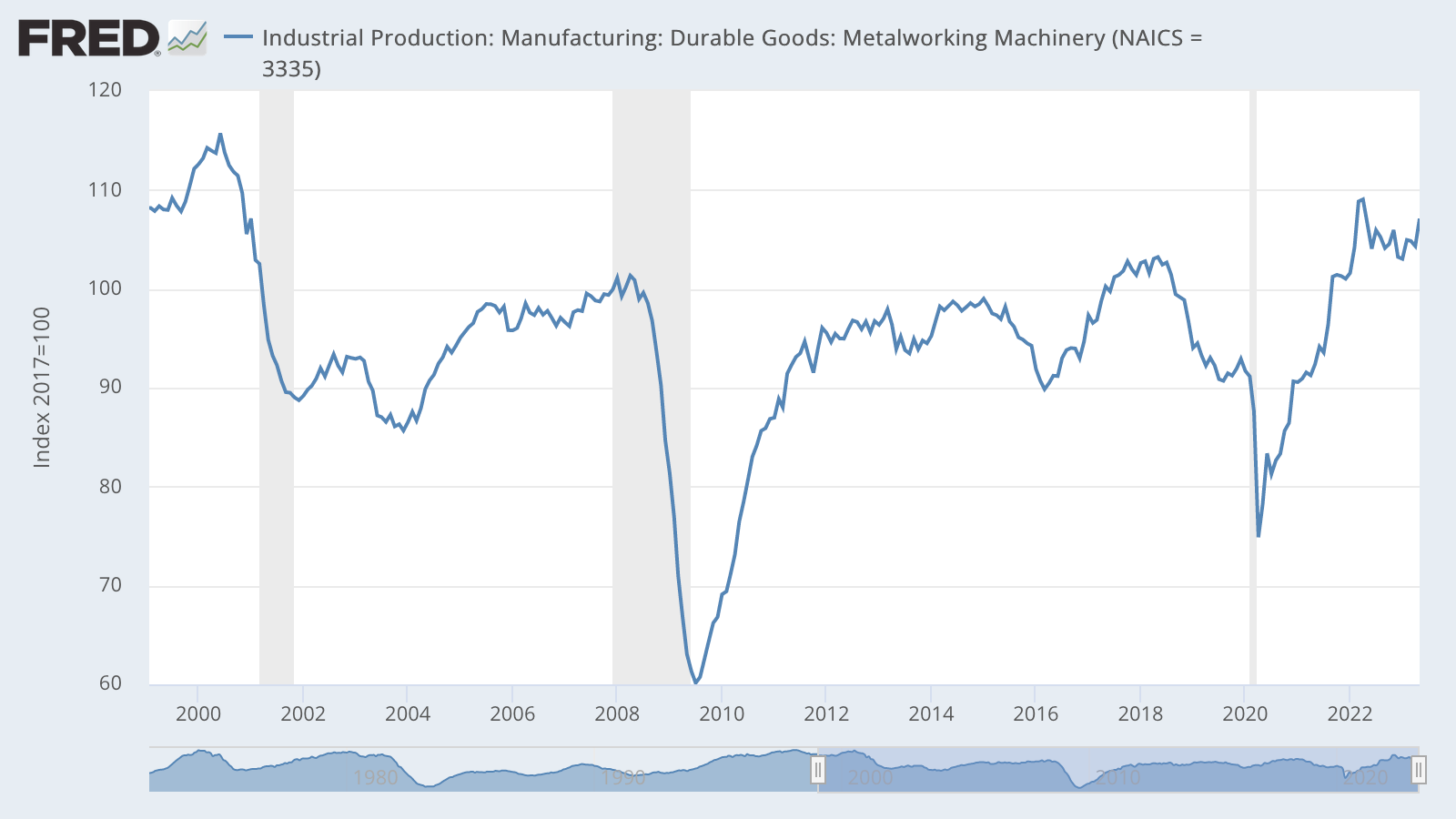

Of course, the purpose of construction is ultimately to produce additional goods (and services). We are beginning to see how the presence of major public investment legislation can help private firms overcome sticky hurdle rates with greater confidence in market and government support for final demand. Key capital goods relevant to the capacity to manufacture are showing signs of unique life, that too at a time when recession risks have dominated media discussion of the macroeconomy. Electrical equipment and metalworking machinery production are among the better guides to manufacturing fixed investment trends. In both cases, they are starting to kick into higher gear.

While it is true that public investment programs might invite a hawkish Fed to hike rates, it's also not the case that the two must have equivalent offsetting impacts on private investment patterns. Whereas Fed hikes operate through more linear cost-of-capital channels, the injection of public investment dollars, if marshaled well, can deliver more nonlinear confidence-enhancing benefits to the private sector. Fiscal policy can open up valuable sums of free cashflow and keep order books full. Those features are uniquely important for (typically capital-intensive equity-financed) industries that maintain high and sticky hurdle rates that are relatively insensitive to funding cost changes. CHIPS and IRA can offer direct pathways to overcoming the key sources of irreducible uncertainty holding back additional private investment.

While some might view this economic activity as a detriment to the Fed's inflation-fighting effects, we would strongly caution that these dynamics are critical to expanding supply and fixed investment, and are largely not targeted at consumption. The Fed on the other hand is hoping and focusing on slowing consumer prices through the demand side, nominal consumer spending. Slowing nominal consumer spending may have some justification but the Fed should not be trying to slow the kind of real fixed investment gains that CHIPS, IRA, and IIJA are poised to help catalyze.

Capital deepening is a major and identifiable ingredient to productivity growth. By ensuring that fixed investment is growing and outperforming relative to labor input has a chance to deliver more sustained gains in welfare and technological improvement where it is most necessary. The upward revisions to manufacturing construction spending are already set to push up Q1 productivity estimates. The monthly data for Q2 is suggesting a more impressive upturn in capital goods output and demand that should be productivity-additive.

Should corporate guidance and continued policy implementation seek to promote the right kind and scale of investment, we may be at the start of something more encouraging.