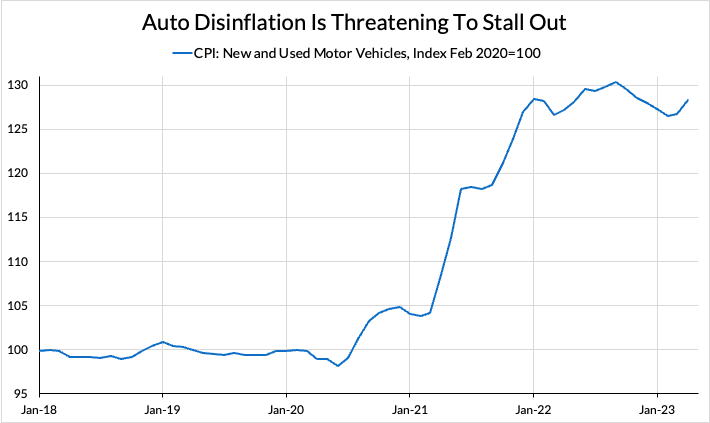

New industrial production data are suggesting that domestic auto production may be recovering. This would be a much-needed disinflationary force against a backdrop where disinflation in new and used autos is threatening to stall out.

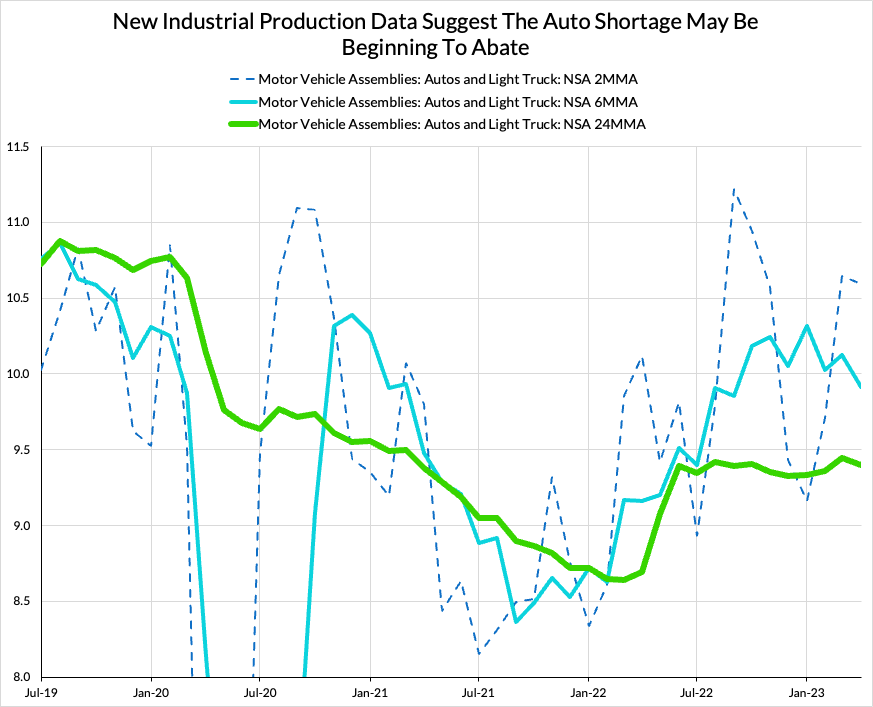

Yesterday, we got new industrial production data from the Fed, and there is encouraging news in auto assemblies. We’re interested in assemblies, because the inflationary problem in auto markets has been one of “too few finished cars,” mainly due to the semiconductor shortage. The headline production data for the auto and light trucks industry includes value-add that results in more vehicles that are closer to finished, but not actually available on the market, because they remain unfinished.

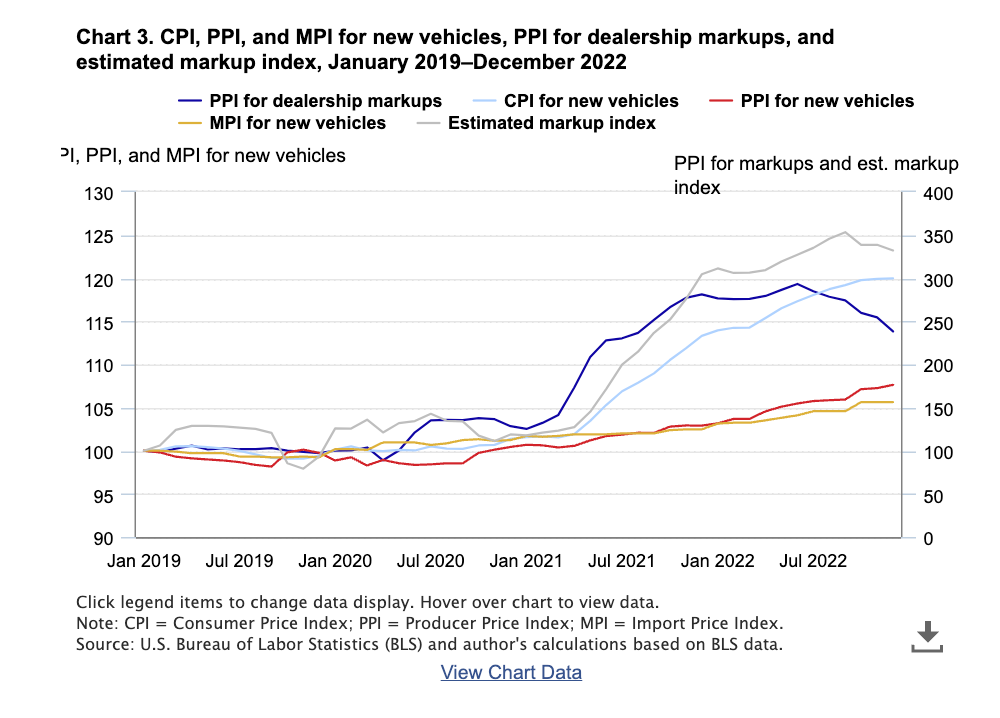

How the auto assemblies series moves is important for the inflation outlook for both new and used cars. In fact, the BLS recently published a study showing that the majority of CPI movements for new and used cars can be traced back to higher margins for dealers of new and used vehicles.

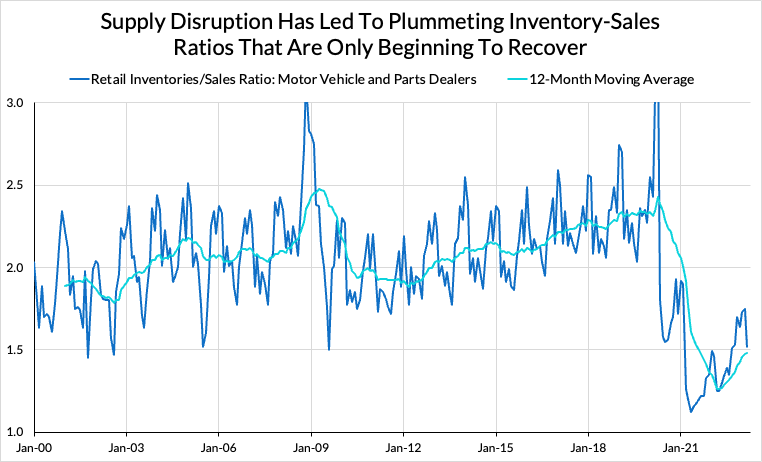

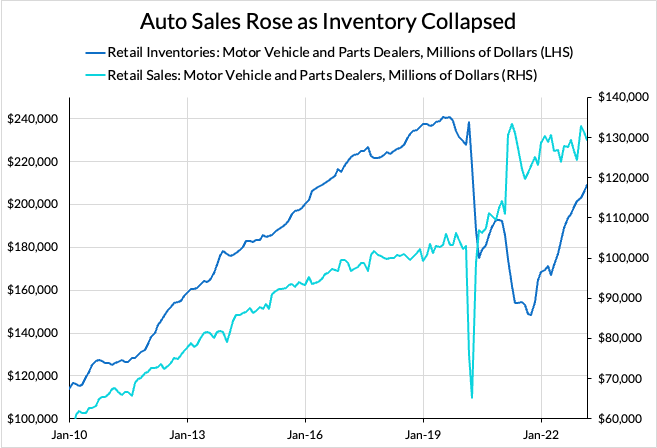

At the root of this issue is pricing power in the hands of dealers simultaneously facing dramatically cut-down inventories due to pandemic disruptions against consistent or even elevated demand for autos. So far, manufacturers have been choosing to ration on quantity rather than price, selling a smaller number of vehicles to dealers at comparable prices to pre-pandemic. These dealers then ration the quantity they received on price to consumers when faced with strong demand for automobiles. As the chart below shows, for much of the pandemic, new autos were often sold as soon as they arrived on lots.

Traditionally, this ratio skyrockets in the early days of recession, as consumers cut back and retailers are left with extra inventory. However, the supply disruptions of the pandemic coupled with the unprecedented level of government support for the American economy have flipped this pattern.

Now, this chart could be evidence of changes in the numerator or the denominator, but we can see that almost all of the movement that matters has been in inventories.

Higher production rates — and especially higher rates of completion of assembled vehicles — should bring up this inventory-sales ratio and hopefully move some more power to resist price increases into the hands of car buyers. We can see this ratio beginning to recover, but it is still a substantial distance from its pre-pandemic habitat.

Impacts from higher production rates will also trickle down to the used market. As it stands, existing dynamics seem to be forcing the marginal price-sensitive buyer deeper and deeper into the used market, further driving up prices there.

With that said, it is hard to see a path to sustained disinflation in new and used autos that doesn’t run through some correction in dealer inventory-to-sales ratios. This leaves policymakers like the Federal Reserve with two choices: waiting it out while production resumes, or crushing demand sufficiently that sales fall enough for inventories to normalize. One of these outcomes is annoying, but the other will bring widespread economic pain.