Prescriptive View: The Fed Should be Explicit About How Interest Rates Work

It has now been almost exactly one year since the Fed started raising interest rates to combat inflation. When they started raising rates, the unemployment rate was at 3.6%. In February, the unemployment rate was… also at 3.6%. Even construction employment, a notoriously interest rate sensitive sector, remains strong. The 12-month growth rate in the core PCE price index fell from 5.4% to 4.7%. The absence of a raise in unemployment and the slight fall in price inflation has prompted speculation about whether or not monetary policy effectiveness has diminished or if the lags between policy changes and economic outcomes has changed.

And then, over the weekend, Silicon Valley Bank suffered a bank run due to its exposure to interest rate risk. As of now, odds of a 50 bps interest rate hike at the next meeting have fallen substantially, and a halt in hikes appears like a plausible outcome. The Fed is now faced with the challenge of conducting monetary policy amidst elevated risks of further financial turmoil, a firm CPI print, and continued resilience in employment despite slowing wage growth. Long and variable lags, indeed.

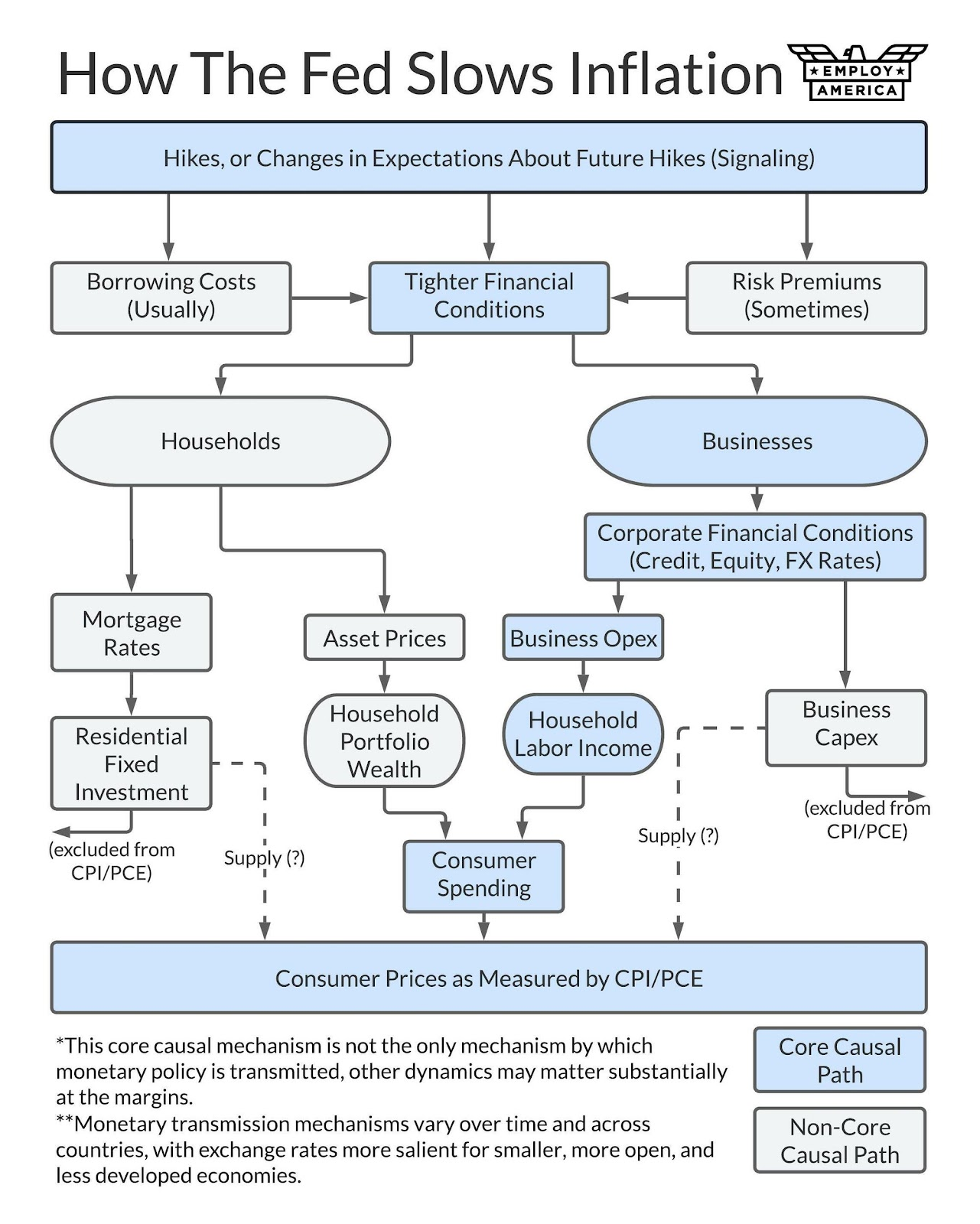

As we’ve written about previously, the Fed’s interest rate tools operate on inflation primarily by influencing financial conditions for firms, which affects hiring and layoff decisions, which in turn affects labor income, consumption, and, finally, inflation. While there might be some more direct channels through which interest rates affect consumer spending (such as interest rates for durable goods purchases), these channels are secondary to the labor income channel, since much of consumer spending is directly financed through concurrent labor income.

As the recent events around the collapse of Silicon Valley Bank show, the path from interest rates to economic conditions can be unexpected and nonlinear. Financial conditions and economic activity don’t respond smoothly and predictably to interest rate changes à la the Euler equation of a representative household looking at real interest rates. When the Fed tightens, things may break suddenly and discontinuously in unforeseen ways.

When economists study the effects of monetary policy on variables such as GDP, inflation, and employment using techniques like vector autoregressions, they are essentially measuring average responses of unemployment, GDP, and inflation to unexpected changes in monetary policy from many different episodes. That may be appropriate for retrospective academic analysis, but for real-time monetary policymaking—especially in an episode as unique as a rapid recovery from a once-in-a-century pandemic—the “variable” part of “long and variable lags” becomes particularly important.

When the Fed’s actions do finally reach the labor market, the burdens of unemployment are not shared equally. Due to the reliance on the interest rate channel, the effects of monetary policy are particularly concentrated in particularly interest-sensitive sectors. Construction workers, for example, are more likely to bear the brunt of unemployment from interest rate hikes. The burden of unemployment falls more heavily on black people and workers with less education. Even if the risk of unemployment was shared equally among all types of workers, the utilitarian costs of drastically reducing the income of a few workers is much higher than slightly reducing the incomes of all workers.

This is a really strange way of fighting inflation. The Fed raises interest rates hoping to tighten financial conditions. If there is financial turmoil, financial conditions will tighten suddenly, and the Fed will be left with the problem of how to clearly communicate its policy trajectory in light of financial stability concerns. When financial conditions finally feed through to the labor market, the costs will likely be concentrated in particular industries and demographic groups. Besides political reasons, one wonders why this is supposedly clearly preferable to, say, raising taxes to lower consumption.

Of course, interest rates are the primary tool the Fed has, and the Fed is the institution in charge of business cycle management for the foreseeable future. Given that reality, the FOMC participants should make clear how they foresee interest rate hikes leading to lower inflation. It also means that the Fed cannot be lax in its duties in regulating and supervising financial institutions.

How will changes in risk-free rates translate into financial conditions that are relevant for business decision-making, especially hiring? In which sectors will employment and production be most affected by these changes, and how are they monitoring these linkages? These are the questions the Fed should be asking itself when conducting monetary policy. To be clear, predictions at this level are difficult. However, this is still preferable to simply saying that “there is going to be some softening of the labor market” as a result of the Fed’s actions.