What a great GDP print. 8.5% nominal growth, and 4.9% inflation-adjusted on the first revision. Although this was largely driven by strength in consumer spending, there are lots of interesting details deeper down in the investment measures.

The first interesting consequence of the strong GDP print is an added piece of evidence for our argument in favor of productivity optimism. Strong growth in output with milder growth in labor hours means outperformance for aggregate productivity measures.

Many have found it hard to reconcile this strong growth performance with the Federal Reserve’s tight monetary policy. In the previous edition of “The Investment Picture”, I pointed to the long-term benefits of the large-scale fiscal and monetary response to the recession. Fiscal spending improved firm and household balance sheets, while low interest rates allowed many to refinance, minimizing debt service costs for the medium term.

Earlier this month, we saw another datapoint in favor of this explanation with the release of the 2022 Survey of Consumer Finances. Without going too far into detail, household finances have improved substantially, both in aggregate and by subgroup, since 2019. This comes after a decade of stagnant survey releases since the Great Recession. A representative factoid: for households that fall within the 40th-60th percentile of incomes – the “middle class” – median net worth fell by 1% between 2016 and 2019 before rising 48% between 2019 and 2022.

Some may say that this means the Federal Reserve needs to keep on with the tight policy. Another way to look at this situation is that the pandemic response provided the US economy with the cushion necessary to weather a number of geopolitical and market shocks without experiencing a significant crisis. As inflation continues to fall, the argument that employment and investment must be curtailed in order to contain inflation weakens as well.

Aggregate investment still looks solid for now, but there are more and more signs that the Fed may be having a negative impact. Investment is what drives long-term growth on the supply side of the economy. Although we may see outperformance in the aggregate productivity measures, the heart of long-term plant-level productivity growth is capital deepening – which comes with investment – and skills deepening – which comes with time. While the Fed has yet to interrupt the latter process by disrupting the labor market, we must not overlook the importance of the former process to long-term productivity growth.

Cycle Indicators

Macro Cycle

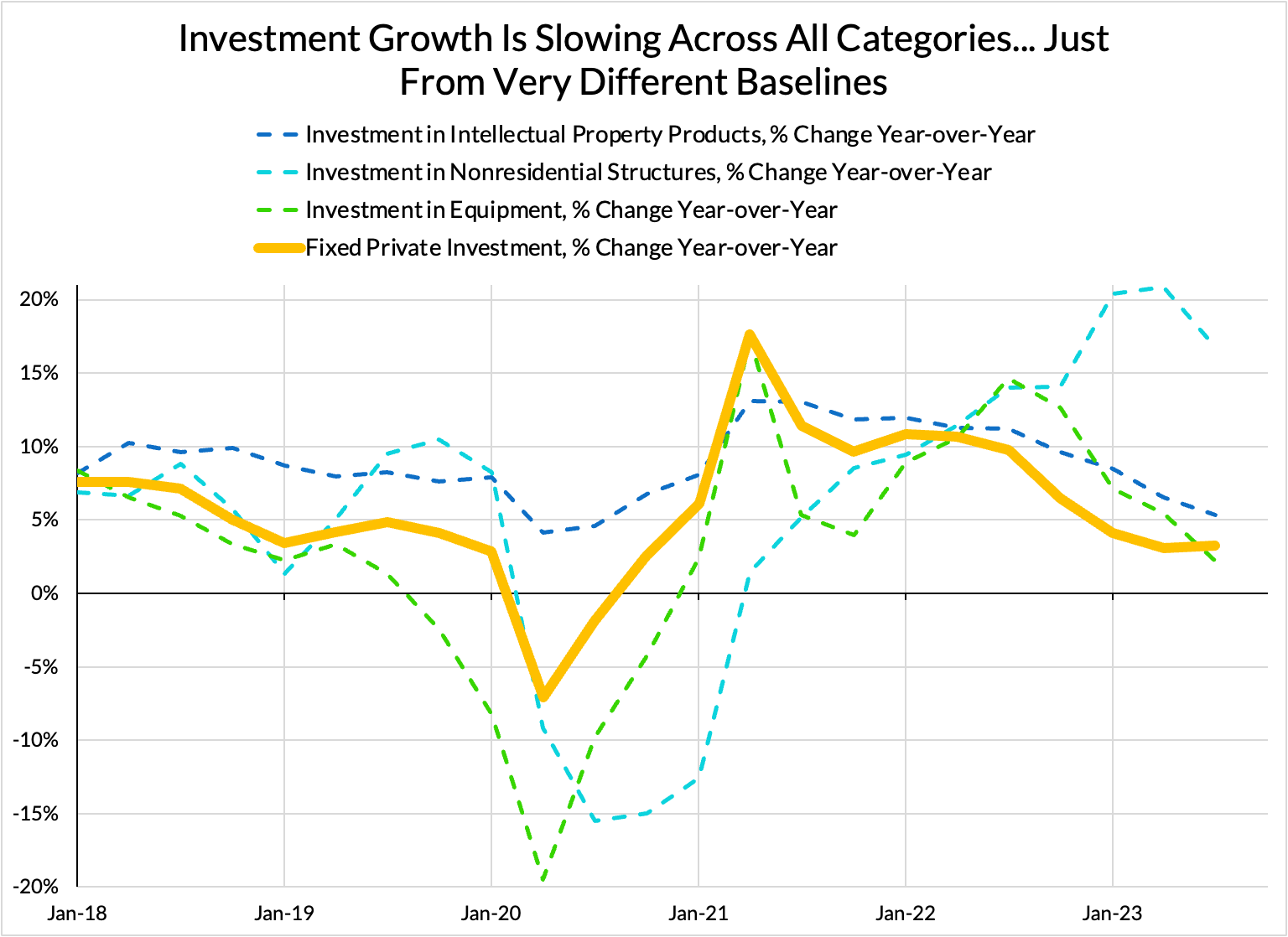

Here we find little evidence for a recession. The strong GDP print, as a whole, was driven by a strong consumer. To that end, consumer spending grew 5.8% year-over year and at a 5.5% quarterly annualized rate. Fixed Private Investment grew at a substantially slower 3.3% year-over-year and 2.8% quarterly annualized rate.

There are some good reasons to expect a slowdown in Q4. However, some significant portion of this strength in the Q3 print comes down to the strong labor market. As long as we see continued firmness there, there is a limit to how weak Q4 GDP can be. For the Fed, the secret may be in learning not to fear the possibility of disinflationary growth.

Investment Cycles

Firm-side nominal investment continues to grow, but we do seem to have passed the post-pandemic peak for the speed of that growth. Overall, fixed investment grew at 3.3% over the past year, and at a 2.8% annualized rate this quarter.

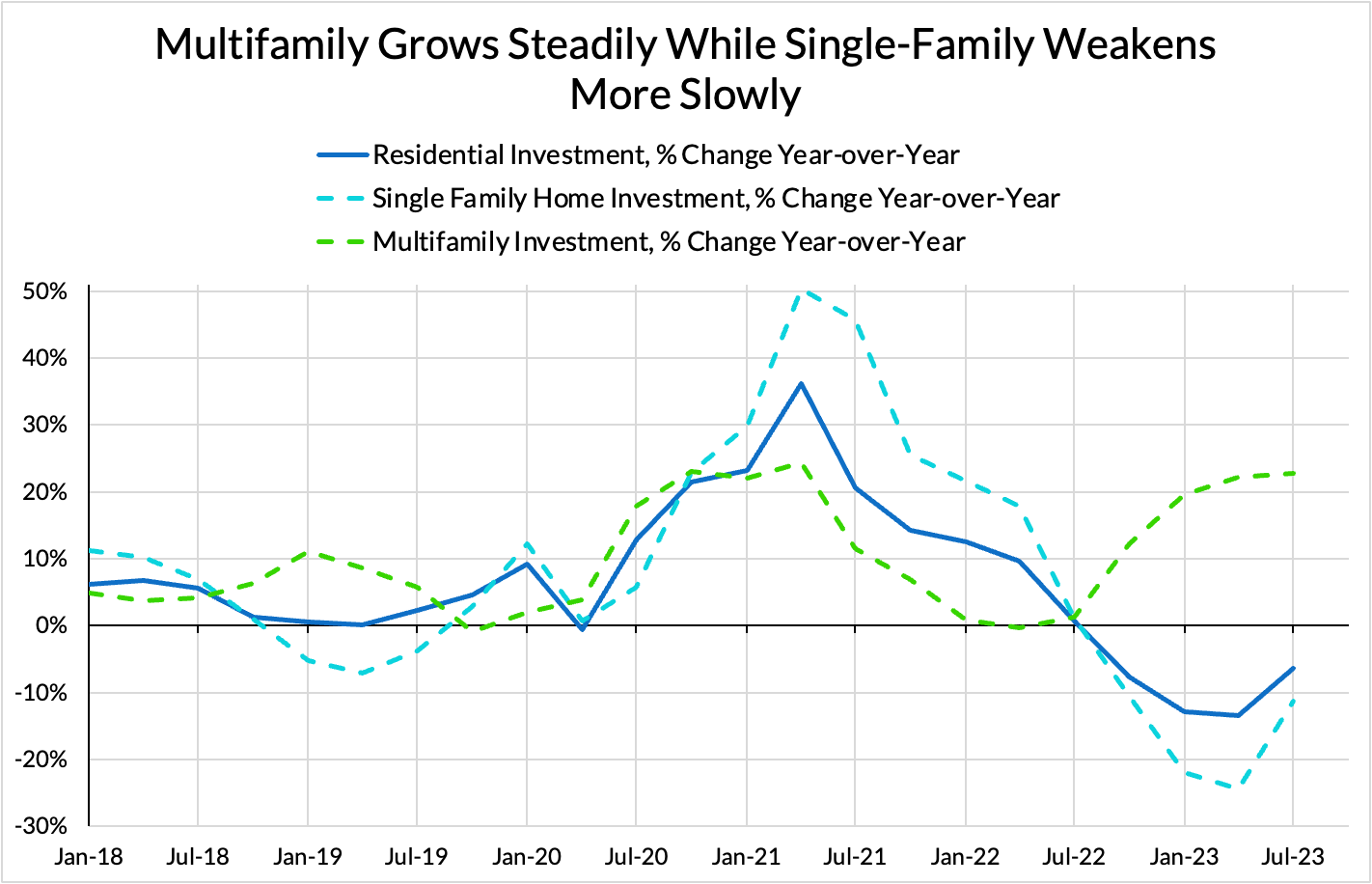

The difference in trajectory between single family and multifamily residential investment is remarkable. Overall, residential investment came in at -6.4% over the past year and a surprising 9.4% annualized rate this quarter. Although multifamily investment continues to grow, it is a much smaller proportion of investment volume. Even worse, multifamily housing starts have taken a nosedive in recent months. However, we are beginning to see a turnaround in single family, which grew notably this past quarter.

Investment Heatmaps

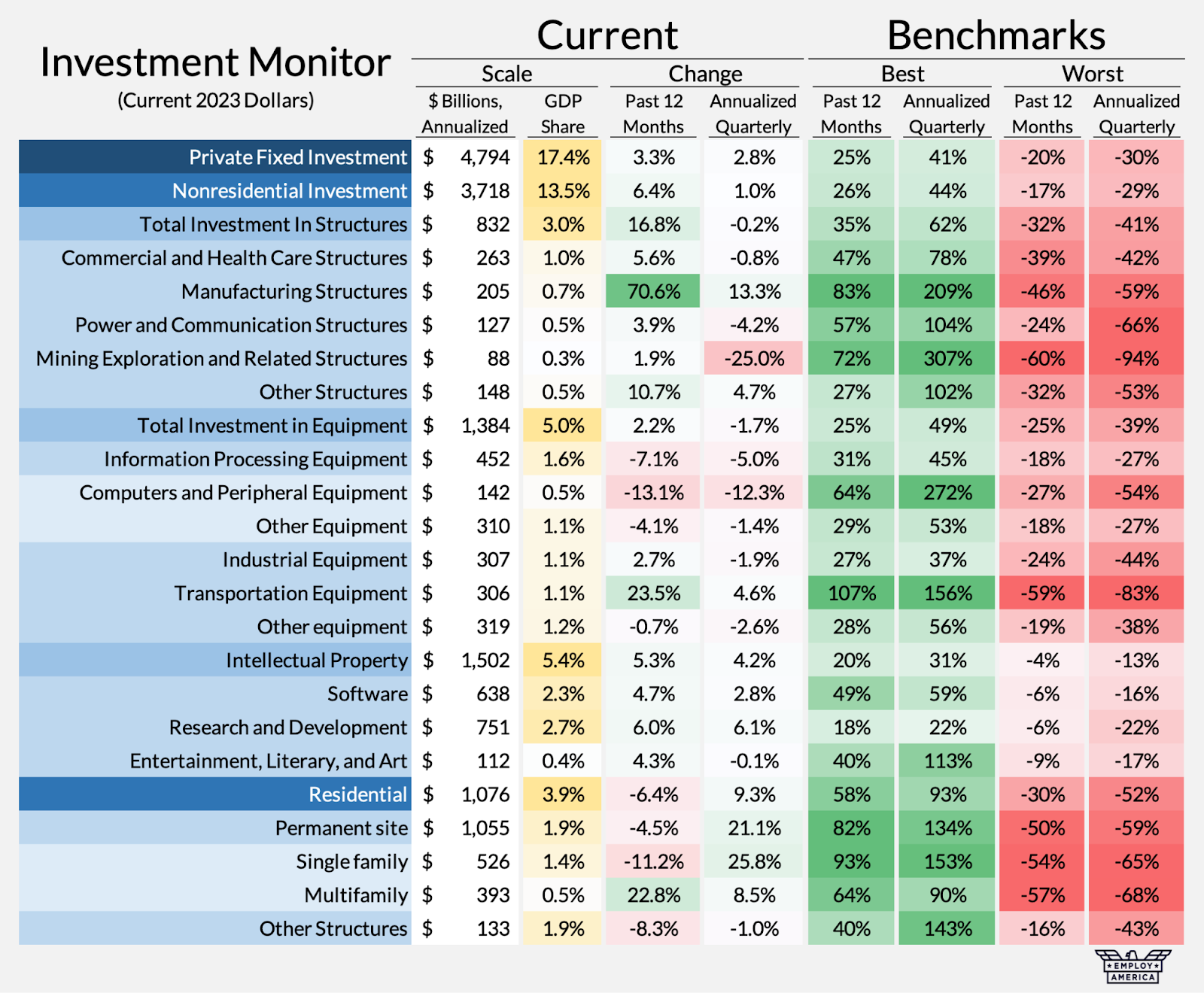

Topline, investment growth is slow but steady. In year-over-year terms, the slowness of that slow growth is due entirely to the slowdown in residential investment: nonresidential investment has grown at a striking 6.4% this past year while residential investment – which accounts for roughly ⅓ the dollar amount of spending as non-residential – has shrunk 6.4% over the same time frame.

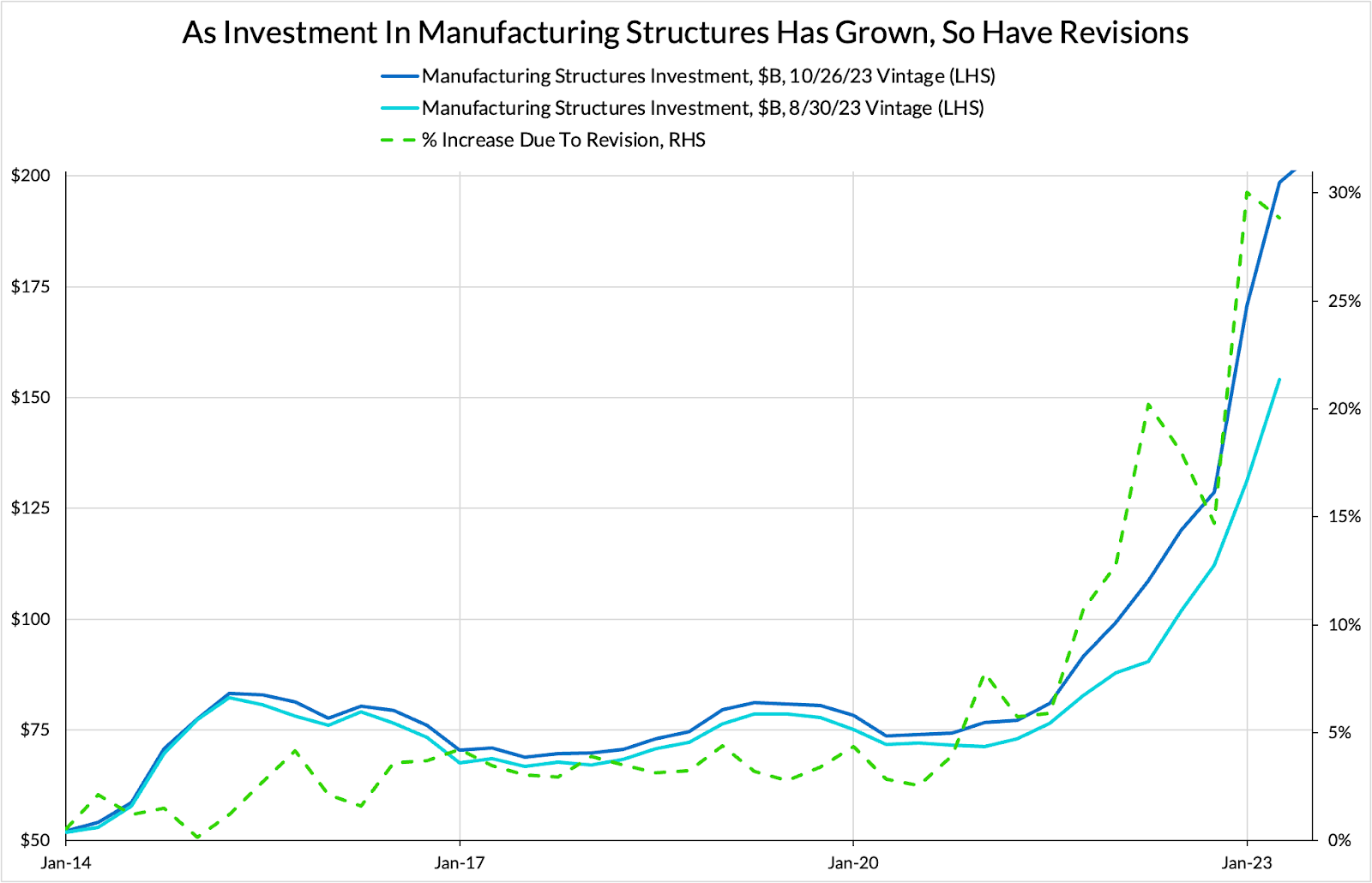

That strong performance in non-residential investment is shared close to equally over structures, equipment and intellectual property. Within structures, we see the strongest growth in the manufacturing subsector. We will dig a little deeper into manufacturing structures below.

After manufacturing structures, multifamily and transportation equipment are tied in a distant second for fastest growing category. The strong performance in transportation equipment is driven in large part by increasing aerospace investment as supply chain snarls continue to resolve and demand for air travel holds steady.

The biggest weakness in year-over-year terms is in single family housing, where the Fed’s tight monetary policy is seeing the most direct impact. From the perspective of housing affordability, lower rates of investment are never a good thing.

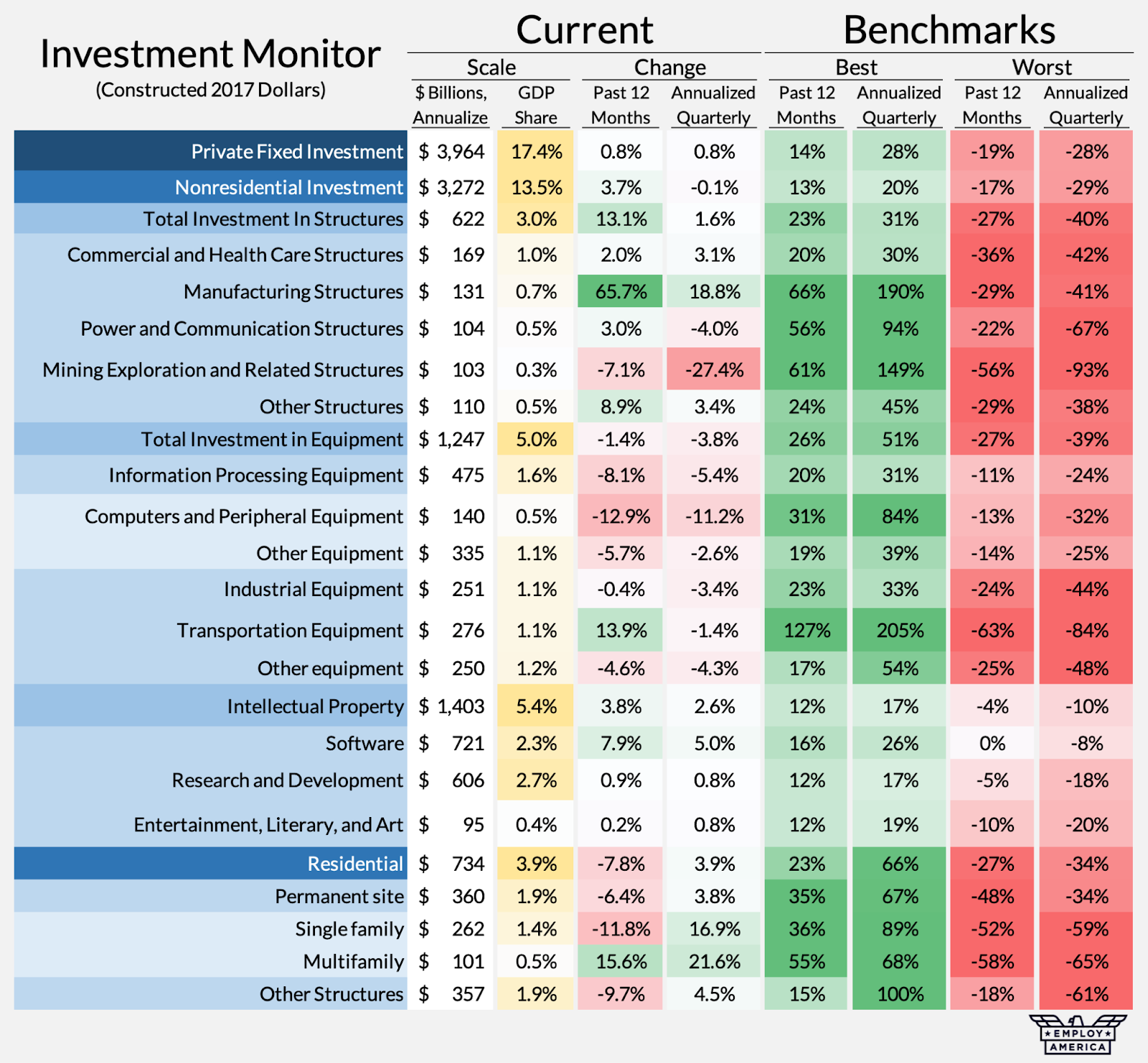

If we adjust to pre-pandemic (2017) dollars, the situation is similar, albeit with weaker growth across the board, as a consequence of post-pandemic and sellers’ inflation.

Nearly everything looks worse when inflation-adjusted, but mining exploration deteriorates the most when we look away from nominal measures. Software – an investment category characterized in large part by the difficulty of constructing an adequate deflator – is the only category of investment to look better in inflation-adjusted terms.

Despite this, investment in manufacturing structures still looks good here. In fact, the annualized quarterly growth numbers for manufacturing should be even better than they are – were it not for a sizable upward revision in the most recent update to Q2 GDP measures.

Monetary Policy and Equipment Investment

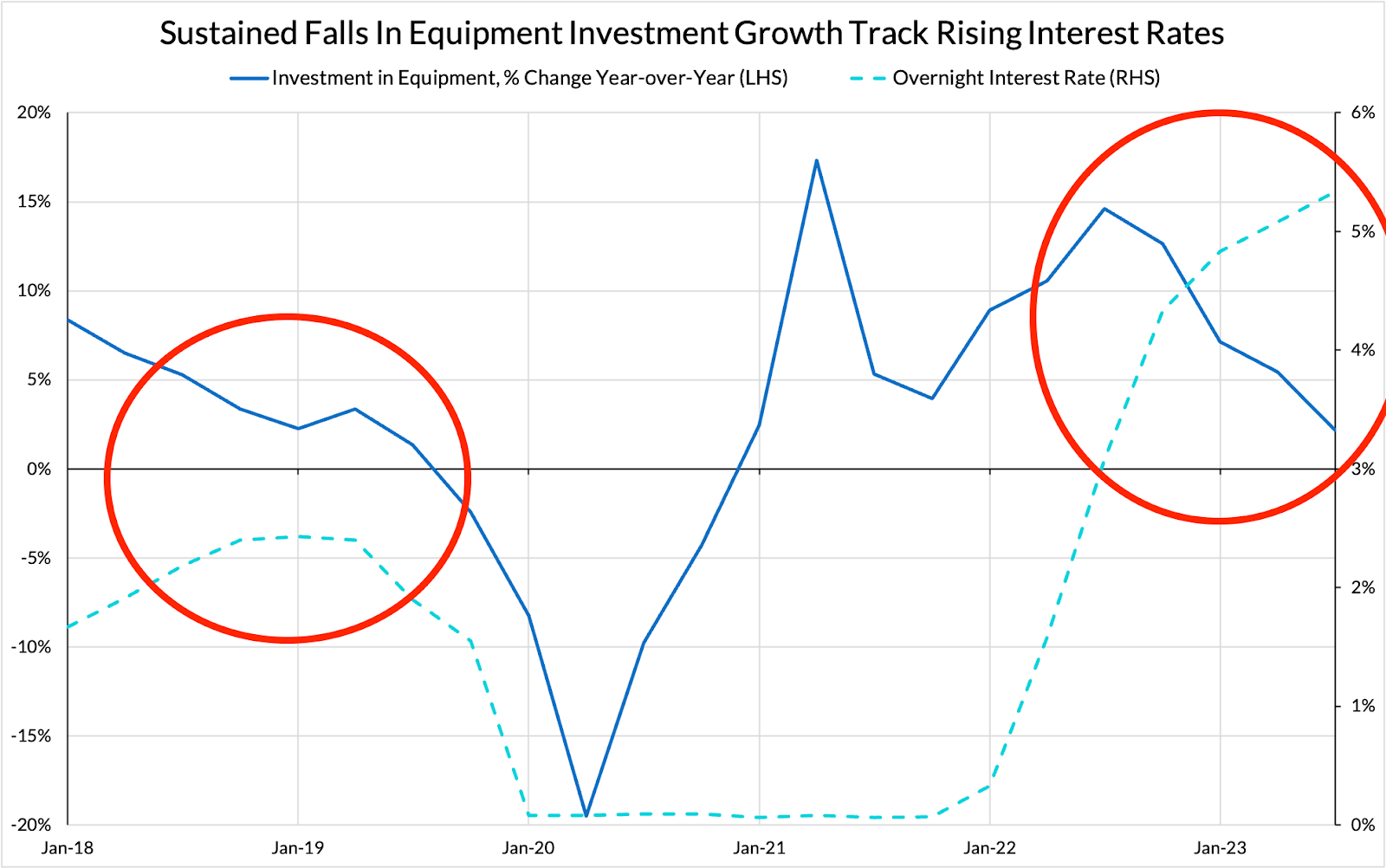

Private fixed investment in equipment would be a natural first place to look for the kind of orderly slowdown in investment that most economic theory predicts as the impact of higher interest rates. Construction projects are long-term, and often budgeted far in advance. Equipment investment is closer to an arms-length market, with less of a penalty of loss due to order cancellation, at least relative to the cancellation of in-progress construction projects. If we expect firms to curtail their capital expenditure budgets in response to a rising cost of capital in aggregate, equipment orders should be the least costly to cancel, and so equipment investment should fall first.

We can see a bit of a rough suggestion of this idea in the nominal data:

At this level of aggregation, causal stories can really only be suggestive at most. So let’s take a look at a narrower group.

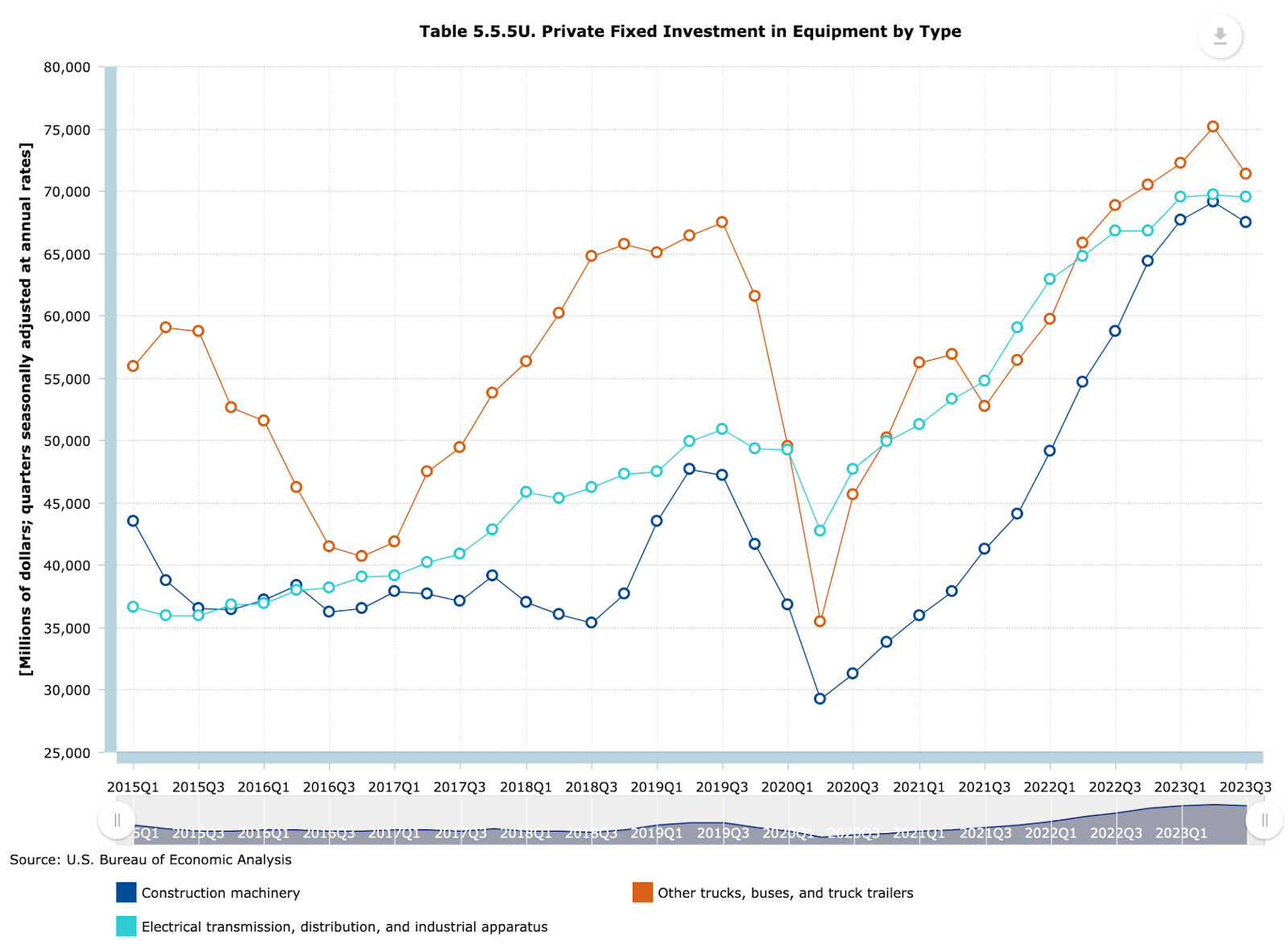

With the Biden Administration’s commitment to infrastructure buildout and the turn towards re-shoring, one interesting place to look for evidence of a supply-side impact of monetary policy through an investment channel is across a range of heavy-industry type equipment.

Again, suggestive and not dispositive, but it sure looks like nominal investment on equipment in these categories is beginning to turn down. Just something that the Fed should keep an eye on while working out just how much longer “higher for longer” really is.