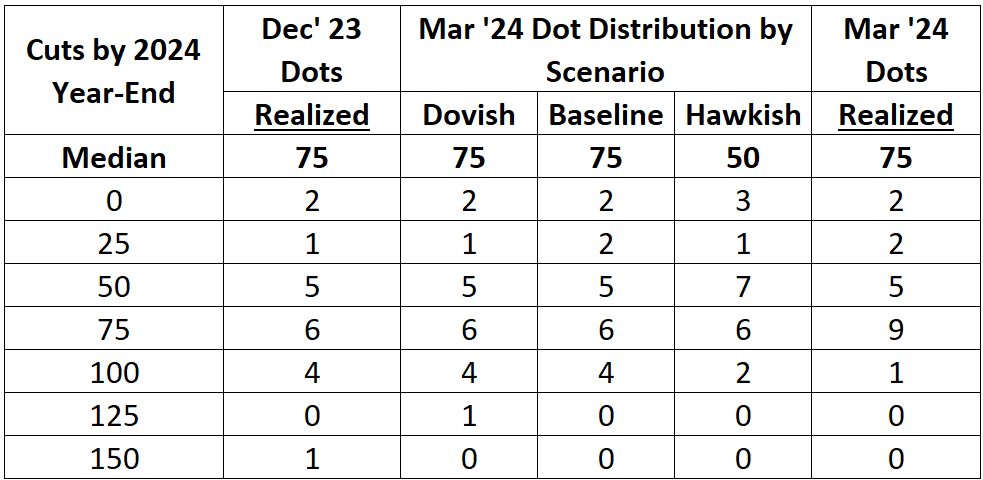

As expected, the FOMC voted to hold interest rates steady at their March 2024 meeting. The median number of cuts projected by the end of 2024 remains at three, consistent with our baseline view. However, as we previewed, the median dot for 2024 is on a knife-edge, with the three-cut median projection of the nineteen FOMC members maintained by nine members at three cuts and one at four.

Relative to our scenarios, the dots of the hawks and moderates came out in line with our baseline. The doves have fallen in line with the moderates, with only one member projecting four cuts this year.

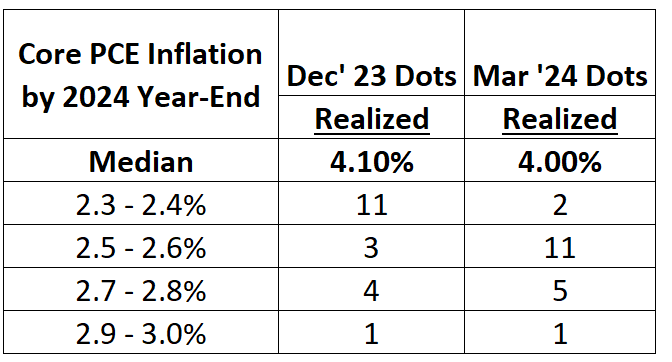

The movement in the dots appears to be directly tied to their inflation projections. While there was not a lot of movement in the members on the higher end of the inflation projections, most members with the lowest December projections for 2024 core PCE inflation revised their projections upwards, while the members with higher projections mostly remained steady. The hawks looked at the hot January and February inflation prints and interpreted it as confirmation of their view of the economy, while the doves got spooked.

In short, the movement in the dots is a direct reflection of the data since the previous meeting, which have seen higher inflation in January and February alongside strong growth and a solid labor market. The Core PCE price index grew at an annualized rate of 5.1% in January and is expected to come in at 3.4% annualized in February, after growing at a rate of 1.9% in the latter half of 2023. Despite these bumps, longer-run inflation measures continue to fall: we expect 12-month core PCE inflation to measure 2.86% in February, down from 2.94% in December.

Meanwhile, economic activity looks solid. The labor market appears healthy, but continues to slow from its rapid growth earlier in the recovery, and real GDP is expected to continue growing at a healthy pace. That constellation of data means we are going to have to wait longer for that greater confidence before the Fed begins normalizing rate cuts.

However, there was a lot to like from the press conference this week. The risk was almost completely to the hawkish side at this meeting; the January and February inflation prints could easily have been used to justify spiking the possibility of a May cut or calling for higher unemployment as necessary to bring inflation down. Powell avoided all of that, stressing that the Fed will be on-guard against signs of deterioration in the labor market and placing the appropriate amount of weight on the recent inflation prints, focusing on the longer disinflationary trend. Here are the highlights from Powell’s press conference.

Fed Normalization is Still the Game Plan

I use the word normalize deliberately. In our piece on Fed policy in 2024, we used that term to describe the process of bringing interest rates back down as inflation comes down, even in the absence of a deterioration in the labor market. Expectations for the beginning of rate cuts may have been pushed back and the dots moved up at this meeting. But, based on Powell’s answers at this week’s press conference (as well as recent Fedspeak by himself and others on the committee), normalization is still the main view of the core of the committee. Take this explicit statement welcoming strong job growth:

Jeanna Smialek: Strong hiring in and of itself would not be a reason to hold off rate cuts?

Jerome Powell: No, not all by itself, no. You saw last year, very strong hiring and inflation coming down quickly…. In and of itself, strong job growth is not a reason for us to be concerned about inflation.

March 20th, 2024 FOMC Press Conference

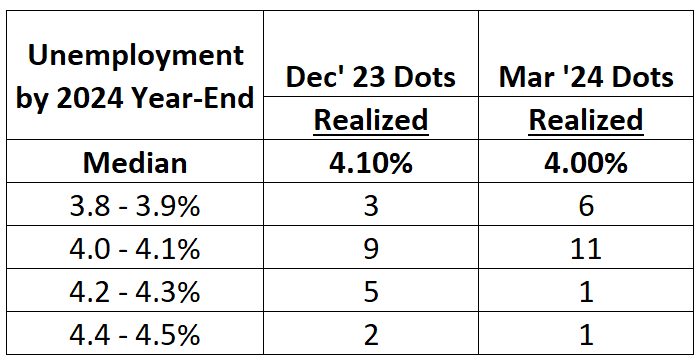

If the Committee’s projections for unemployment are anything to go by, they largely agree. While the median unemployment dot only fell slightly, this masks a substantial reduction in the Committee’s projections; now, only two members see unemployment rising beyond 4.2% by the end of this year.

Now, nearly every FOMC member sees unemployment rising by no more than 0.2 percentage points from its current level of 3.9%. This is a stark contrast to the recessionary projections of the Fed in early 2023, let alone the more dire predictions of other commentators.

Minding the Bumps While Keeping an Eye on the Road

It would have been very easy for Powell to overreact to the two months of unfavorable inflation data. However, Powell placed these data points in their appropriate context by focusing on the longer-run trajectory of inflation:

[January and February 2024 inflation] certainly hasn’t improved our confidence, it hasn’t raised anyone’s confidence. But I would say that the story is really essentially the same. And that is one of inflation coming down gradually towards 2% on a sometimes bumpy path… I think that’s what you still see. We’ve got 9 months of two and a half percent inflation now and we’ve had 2 months of kind of bumpy inflation… we were saying that it’s going to be a bumpy ride and we’ve consistently said that.

Jerome Powell, March 20th, 2024 FOMC Press Conference

Powell justified this view by pointing out that the Fed similarly didn’t cut in the wake of the lower inflation readings in the latter half of 2023. It is encouraging that Powell is being even-sided in not overreacting to short-run inflation numbers and instead taking the long view.

Maintaining optionality this time:

After the January FOMC meeting Powell actively spiked the possibility of a March meeting, even before the January inflation data and jobs data. This is somewhat of a moot point after those data releases, but we thought it was an unforced error. This time around, Powell was directly given the opportunity to spike the possibility of a May cut, and declined:

Ann Saphir: Is there enough data between now and, say, May, to be able to get the kind of confidence you still need?

Jerome Powell: I really don’t have anything for you on any specific meeting going forward…. Things can happen during an intermeeting period, unexpected things. I don’t want to dismiss anything…. If there were a significant weakening in the data, particularly in the labor market.

March 20th, 2024 FOMC Press Conference

As of now, we think the probability of a May cut is small—it would probably require both good March inflation data and notable weakness in the labor market. But, Powell’s comments show that he is on-guard against threats to the employment side, and ready to move if necessary.

Where They Should Go from Here

For now, the Fed is still waiting for further confirmation of disinflation. For now, that is understandable given the recent inflationary prints. In our playbook for Fed policy in 2024, we wrote: “ Lag if you must, but follow inflation down.” The Fed should be ready to begin rate normalization as soon as they get the remaining “bit of evidence” necessary to convince them that inflation has come down. Failing to do so would risk slowing the labor market further than necessary and continue the Fed's weakening of the supply-side of the economy.

Powell’s press conference (as well as recent Fedspeak) seem to indicate that the Committee is broadly on board with this view. However, some members of the Committee have hinted that they might be willing to wait even longer.

My conjecture is that, in the absence of a major economic shock, delaying rate cuts by a few months should not have a substantial impact on the real economy in the near term.

Chris Waller, February 22nd, 2024

“Maybe this constellation is neutral… so why do anything?”

Neel Kashkari, March 6th, 2024

One main argument for waiting further has been the notion that perhaps the natural real interest rate (r*) is higher than it previously was, and thus Fed policy is less restrictive. One way of seeing this is in the Fed’s projections of its longer-run interest rate, which ticked up from 2.5% to 2.6% at this meeting. While the modal member sees the long-run interest rate between 2.38% and 2.62% (implying a neutral real interest rate of around 0.5%), other members see the long-run federal funds rate as higher, with one member’s projection implying an r* of around 1.75%.

It may well be the case that the neutral real interest rate has gone up, but it’s far from clear at this point. As Powell said at this press conference, “there’s tremendous uncertainty about that.” John Williams, who is the Committee member with the deepest background in this topic, thinks it’s still low. In any case, a potential rise in r* changes the final destination of normalization but not the need to normalize in the near-term as inflation falls.

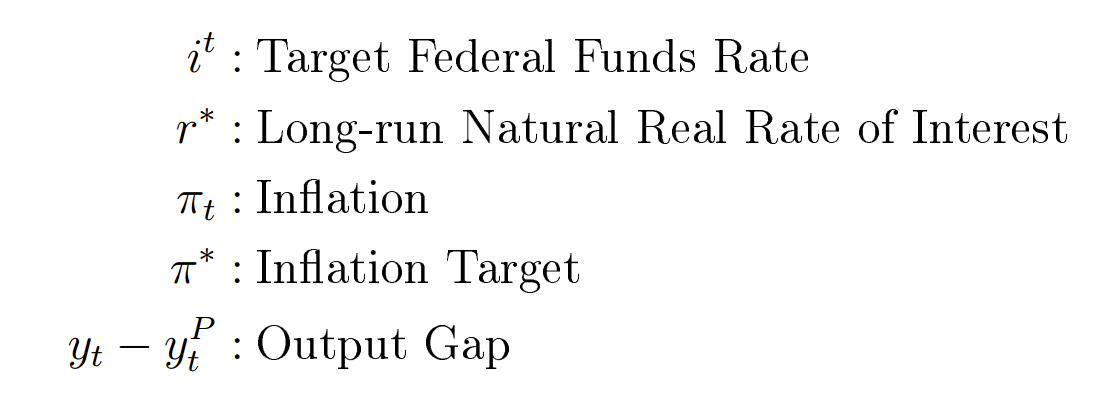

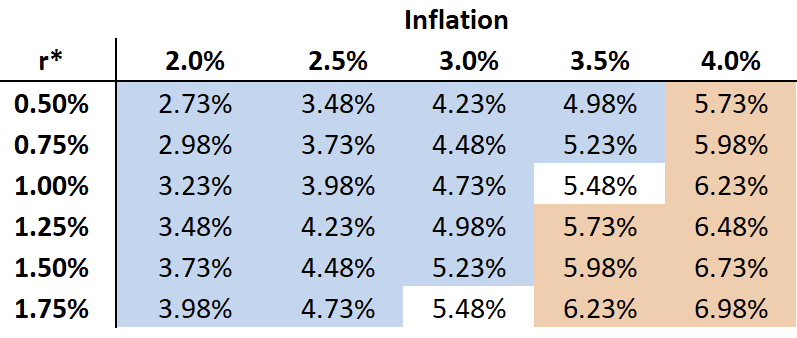

A useful benchmark to consider is the "Balanced Approach" monetary policy rule that former Fed Chair Janet Yellen and other key Fed staff and officials have promoted. This variation on the Taylor rule follows:

where:

The table below shows the implied policy rate prescriptions from the Balanced Approach rule under different levels of the neutral real interest rate and inflation (assuming unemployment remains at 3.9%):

There is always uncertainty around both where underlying inflation and r* are. To start with the first, core PCE inflation is running at 3.05% annualized on a 6-month basis and 2.86% on a 12-month basis. The Federal Reserve Bank of New York’s Multivariate Core Trend of PCE Inflation is at 3.04%. In that range of inflation estimates, the current rate is above the rule’s prescription for almost all of the range of r* estimates. Even at the upper limit of the Committee’s estimates of r* at 1.75%, policy will be restrictive if core inflation comes down to 2.6%, as they project it will by the end of this year.

As we wrote in our playbook, rate normalization should be faster at the beginning, when restriction is apparent, and slower at the end. One reason for going slower at the end could be that uncertainty about where r* is. It’s an inverse of the reasoning the Fed used to hike quickly in early 2022, when it was clear that Fed policy was accommodative, and slower as it reached peak rates. If you think the natural rate is higher, that shouldn’t be an argument against moving now. It’s an argument about ending up at a higher destination.

To be clear, the Fed does not rigidly follow this (or any) interest rate rule. We expect them to lag inflation its way down, but looking at the rule’s prescription is a useful way of thinking about how to handle the uncertainty around the level of the natural rate of interest as inflation falls.

A significantly higher level of r* is not the consensus view of the committee. However, we are starting to see the idea that this is a reason to remain higher for longer creep in at the margins. Powell has indicated that he is willing to go even if there is not unanimous consensus among the committee when it comes time to cut:

“...we do try to achieve consensus, and ideally unanimity. People do dissent. It happens. Life goes on.”

Jerome Powell, March 20th, 2024 FOMC Press Conference

When it comes time to cut, there will probably be some FOMC members who will want to hold off. How much Powell can build consensus and how much dissent he is willing to tolerate may play a role in the timing of the first cut.