“For the first time, we [central bankers] have had to really study [supply chains] carefully”

- Chair Powell

As we have argued, a substantial portion of post-pandemic inflation can be traced to supply chain disruption. What was a loosely woven mesh pre-pandemic snapped and disconnected in different places, for different reasons, and for different lengths of time, in ways that make it difficult to get clear pictures of the situation in the data. Although repairing that mesh—resetting expectations and reconnecting suppliers and purchasers with one another—is key to containing inflation in the medium term, it may not be enough to guarantee disinflation in the near term. Policymakers and commentators should be careful to remember that even when supply chain problems resolve themselves, they can easily leave large “air pockets” of missing production that can exert substantial force on market prices. This air pocket eventually passes through, but before it has, supply chain resolution may prove substantially less of a disinflationary force than commentators and policymakers at the Fed are expecting.

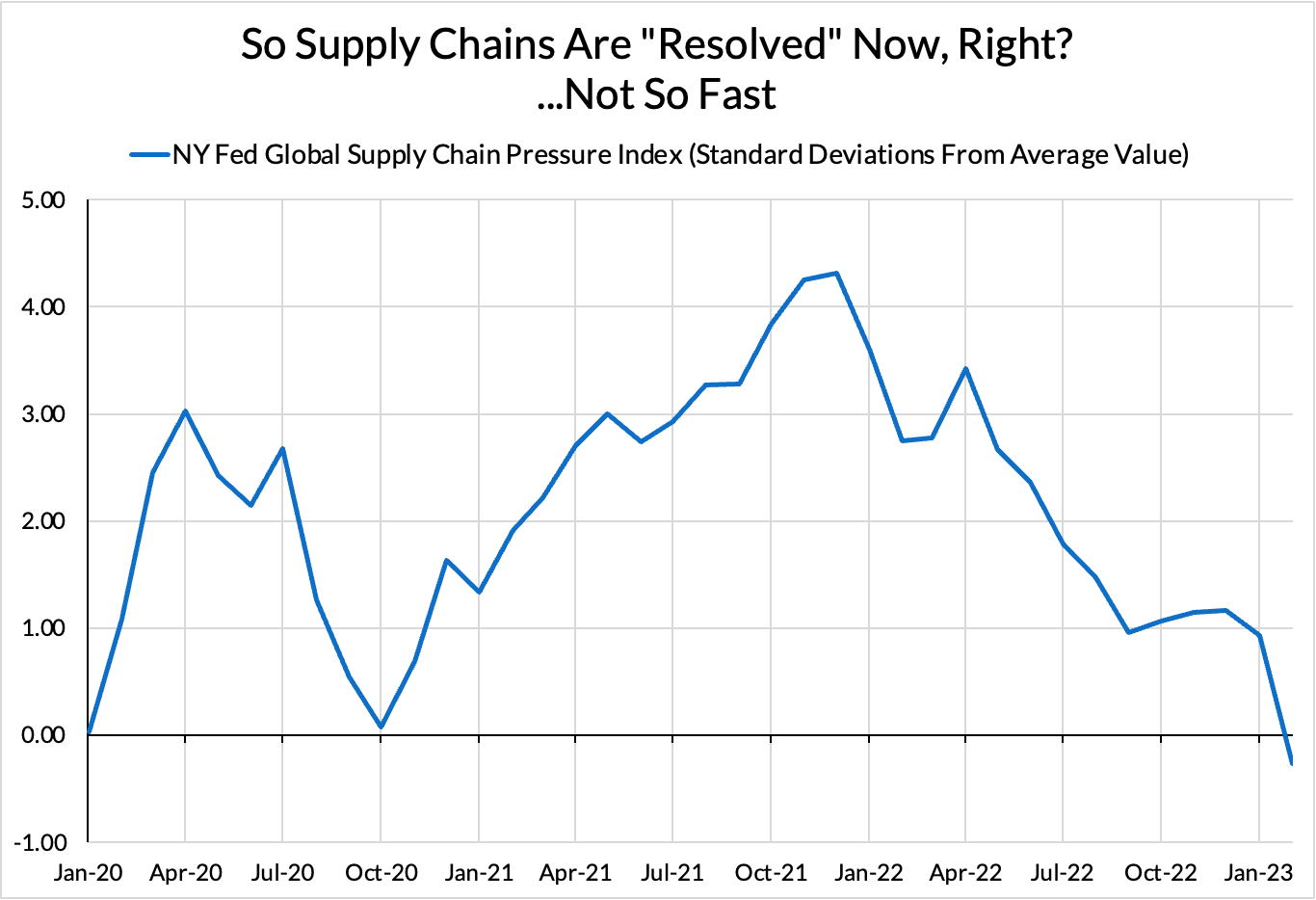

To wit, the NY Fed’s “Global Supply Chain Pressure Index” appears to show supply chains “returning to normal” after a period of sharp disruption in 2020 and rolling difficulties in 2021 and 2022:

However, if we dig into the guts of this index, we find that that may not be the right interpretation. A substantial portion of the index is built on PMI data from the Institute for Supply Management. This is a great data source, but the data the NY Fed is using measures the rate and direction of change of supply chain issues, not their outright level.

What the chart above shows is that things are likely, in aggregate, no longer getting worse. If we think about this in terms of “air pockets” in the supply chain, it simply means that the 2021-2022 air pocket is now closed. Even though it’s no longer getting bigger, the air pocket still has to pass through the rest of the system. This is the lesson of renewed pricing strength in used car markets: despite new auto production returning to the same neighborhood as pre-pandemic production, pricing in this market happens on the margin and right now marginal supply is dominated by this air pocket.

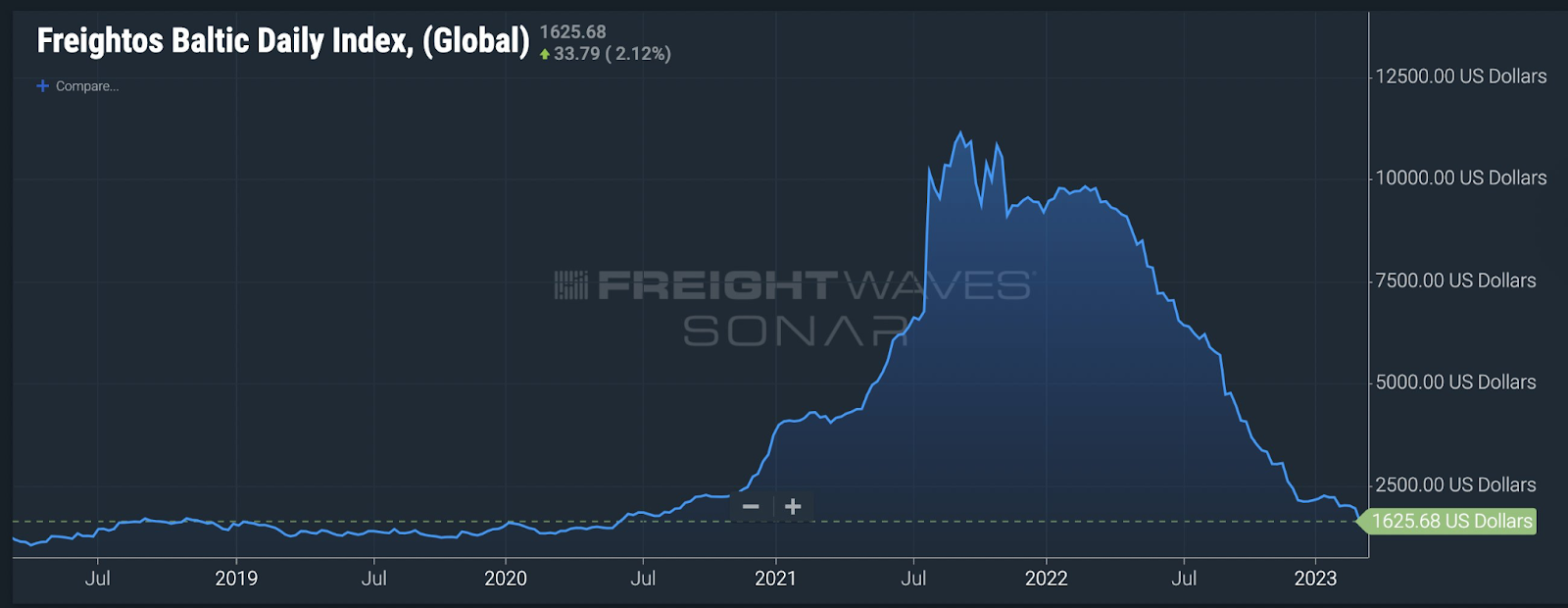

Logistics issues that have plagued supply chains over the pandemic paint a similar picture of a “normalization” that hasn’t quite normalized.

Spot shipping rates have round-tripped relative to pre-pandemic, but over that round trip, aspects of logistics market structure have shifted in ways such that the falling prices will likely have less disinflationary effect than rising prices had inflationary effects. Facing rising spot prices, many supply chain participants shifted into longer-term contracts, locking in higher-than-spot prices in order to hedge against prices rising further. Once prices are “no longer getting worse,” firms may remain locked in those contracts, such that falling spot shipping rates may offer less disinflationary power than expected.

The problem for the broader economy is that “not getting worse” is still worse than expected from the Fed’s perspective. Going into 2023, many expected a handoff from goods disinflation to housing disinflation to services disinflation, but that is happening slower than expected due to granular bottlenecks like the problem in used and new autos. If the Fed is thinking that the supply chain problems are sufficiently “fixed” as to be no longer inflationary, they are probably wrong.

As happens often in a complexly measured dynamic system like an economy, the issue here is a basic stock-flow consistency problem. “Supply chain disruption” isn’t something that can be easily quantified, but we can trace how shortages and expected shortages can lead to sudden, sharp price spikes by looking at how they affect pricing on the margin. These issues don’t generate one-off price increases, but rather, create a situation where upstream and downstream supply chain participants have to haggle and fight over who is going to pay for the air pocket of missing production. Different sectors will see different outcomes given different balances of power and elasticities, which will play out differently in the measured inflation data.

If the Fed gets it in mind that the supply chains being “fixed” means that past supply chain issues won’t show up in future inflation, they will likely be surprised. Those “air pockets” may need to pass through the system for us to get to actual disinflation, but it’s far from clear that tighter Fed policy is going to make them move any faster.