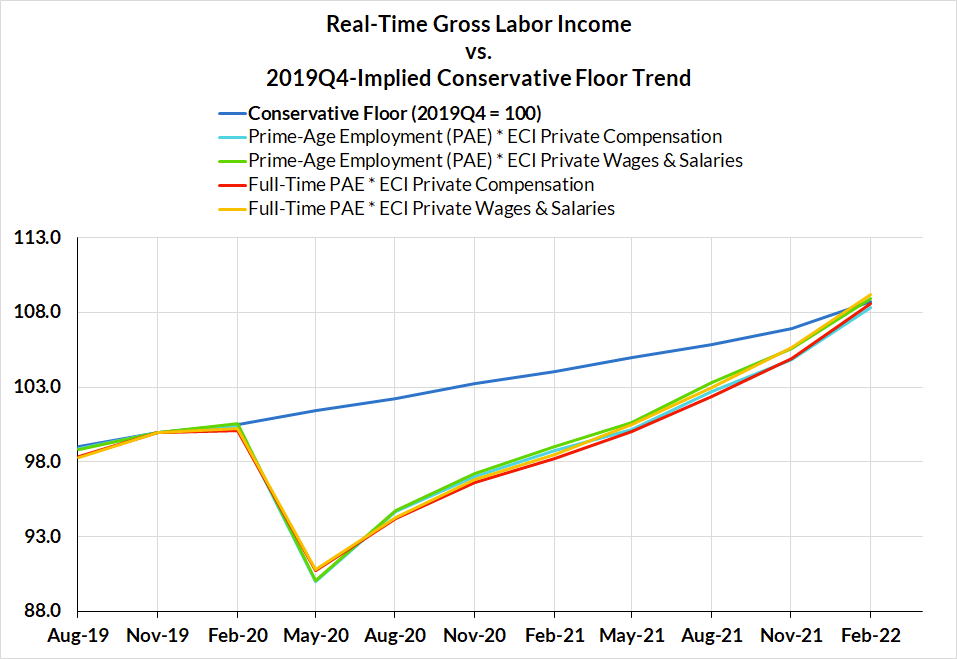

If you have been following our real-timemacro commentary, you’ll know that the economy has been making rapid progress towards the key benchmarks we consider necessary conditions for tightening policy. Although data can only be released on a lag to reality, we now have confirmation of what we expected was the case. As of the first quarter of 2022, we have effectively recovered the jobs and wages lost to the pandemic-induced recession.

Today’s labor market is closely comparable to the pre-pandemic labor market, especially after accounting for aging, the dynamic nature of prime age labor force participation, and the scale of wage outperformance. With prime age employment and wages making robust gains in March, our nowcasts for March “Real-Time Gross Labor Income” are firmly above the floor imposed pre-pandemic.

With this achievement now obvious, we enter a new phase of this expansion: preservation. Preservation of the expansion means two things in the current context:

1. Slowing down inflation and, by extension, labor income growth. While it was desirable for labor income growth to run strong to expeditiously “catching up” the ground lost during the recession, sustaining this pace year after year would prove inconsistent with the Fed’s longer run inflation goals.

2. Avoiding an excessively abrupt income growth slowdown that causes employment rate declines. No matter what path the Fed chose, a slowdown was coming this year: with reopening and fiscal impulses rolling off, employment can’t help but slow. Slower gains in prime-age employment are hardly a tragedy, but if we begin to see signs of outright reversal, more vicious feedback loops are likely to emerge.

The wild card within our framework is wages. Despite its popularity with the macro commentary consensus, we do not subscribe to the view that there is a rigid Phillips curve-like relationship between the level of labor utilization and the growth rate of wages. While there is room for reasonable disagreement here and plenty of uncertainty to grapple with, we think it is more likely that labor market churn and wage gains will both moderate as the reopening and fiscal impulses to economic activity dissipate. The mid-2000s and the mid-1980s are two clear counterexamples to the Phillips Curve view of wage growth: wage growth slowed even as employment rates rose and unemployment rates fell.

When tightening, the Fed should continue to take each decision meeting by meeting. It is critical that they remain watchful of how their policies are achieving traction and how external factors are influencing financial conditions and the outlook for labor income growth and and for inflation. But given that the first checkpoint (recovering to labor income levels consistent with the pre-pandemic trend) was achieved in 2022Q1, we now face a set of conditions where, with both labor income growth and inflation running especially strong, interest rate hikes at this juncture are more clearly justified.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.