May 2026 Core-Cast Post PCE: Quirky Measures Drove our Miss; Supercore (Core Services Ex-Housing) is Running Hot

Our month-over-month May Core PCE nowcast of 0.40% came in 8 basis points above the realized 0.32% reading. Our error stemmed from Supercore (core services ex-housing) – the realized readings for nowcasts for core goods and housing came right in line with our final nowcasts for May.

Within Supercore, our miss stemmed almost entirely from two categories: final consumption expenditures of nonprofit institutions (0.42% nowcast vs -0.86% realized) and tax preparation services (11.76% nowcast vs 4.14% realized).

Before the discussion, we’d like to address our recent misses, which have recently been outside of our typical error band. The BEA has recently shifted its methodology for choices for tax services by taking a smaller share of the CPI input for tax services and capturing the rest as a judgmental trend for PCE. Final consumption expenditures of nonprofit institutions is an opaque category. The BEA deflates it by input cost measures – this measure is currently disinflating with a lag to wages. We are currently refining our models and fine tuning our forecasting and nowcasting techniques to improve accuracy in these and other difficult categories and hope to be back on track soon.

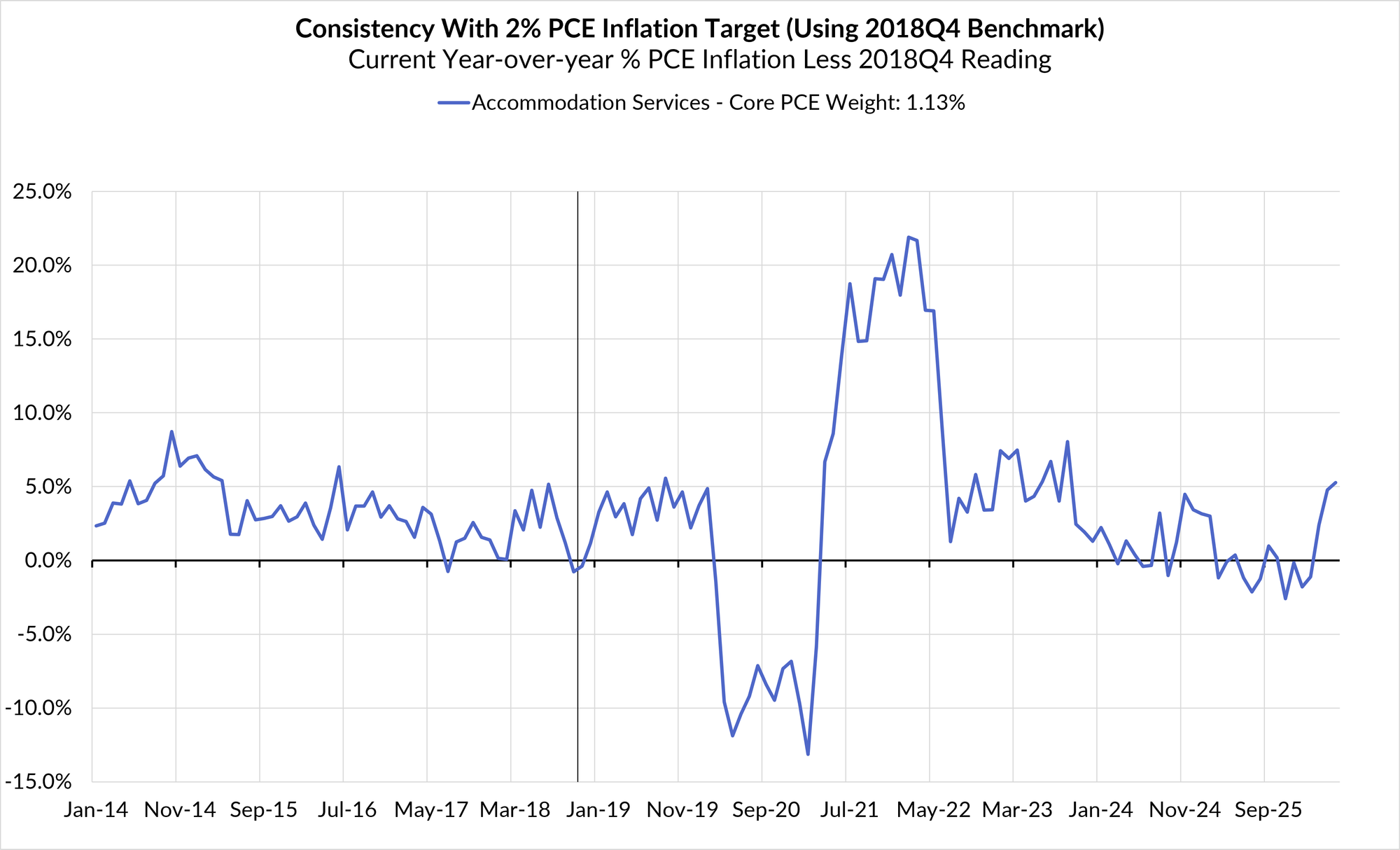

Supercore (core services ex-housing) is a real problem for the Fed. Portfolio management, Healthcare services, airfares, food services, and lodging are all running hot. Portfolio management will likely continue to run hot due to equity market performance. We would like to emphasize that even if one strips out portfolio management and other imputed prices (Market-Based Supercore) is still running hot and the risk for these categories is still tilted to the upside. Even though crude oil prices have rapidly come down to the $70-80 range from the MOU with Iran and potential reopening of the Strait of Hormuz, crack spreads for gasoline, jet fuel, and diesel have yet to show similar reprieve. It could take several more months for prices for these refined products to normalize – especially diesel and jet fuel. More importantly, the transmission of these refined products into airfares and food services may not happen until later this year. We could also potentially see more upside risk over the next two months from world cup driven tourism demand in transportation services, lodging, and food services.

Core Goods offered some relief in May. After running between roughly 5% and 6.5% on a three-month annualized basis from February through April, Core Goods fell by 9 basis points in May, pulling the three-month annualized rate down to about 1.7%. This was primarily led by prescription drugs (−0.90%) and broad softness across apparel and home furnishings. Jewelry, major appliances and footwear still saw some upside. We would caution against declaring victory on tariff inflation as of now. Tariff effects have yet to show up in new vehicles and we could start to see some more passthrough in 2H2026 when section 301 and 232 tariffs are announced and finalized.

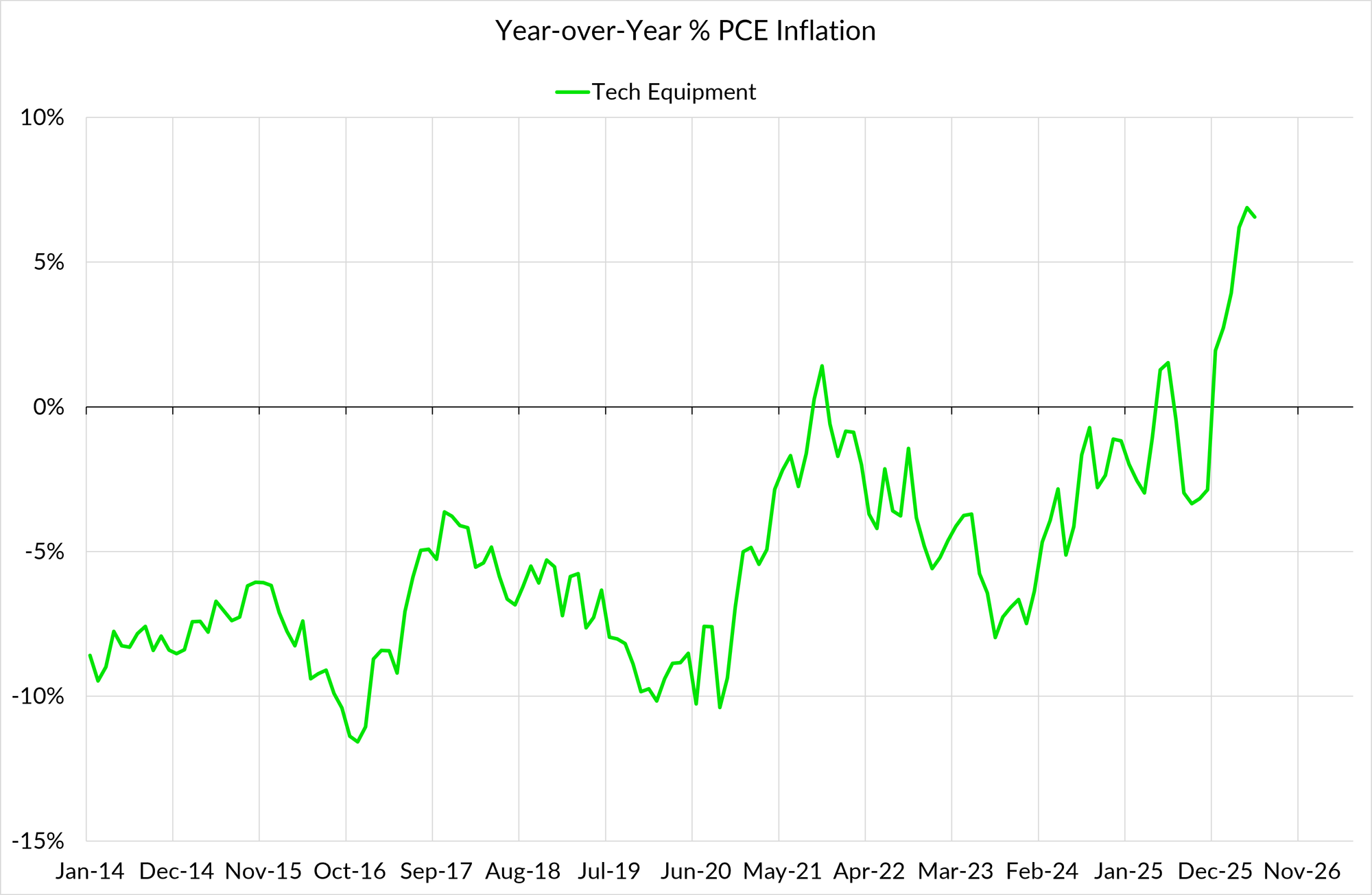

Tech equipment – which normally shows deflation – has been running hot for several months due to AI-related bottlenecks (memory shortages in particular) but also showed some relief in May (-0.24%). The three-month annualized rate for these categories is still running at a staggering 20.1%. We see more upside risk to this category, as there is no sign of the memory bottleneck breaking anytime soon. Just today, Apple announced a series of price hikes on various products due to the memory and storage shortages. While hedonic adjustments may cancel the inflationary impact, more persistent shortages of memory could start to impact production for motor vehicles, TVs, smart appliances, and streaming and gaming devices.

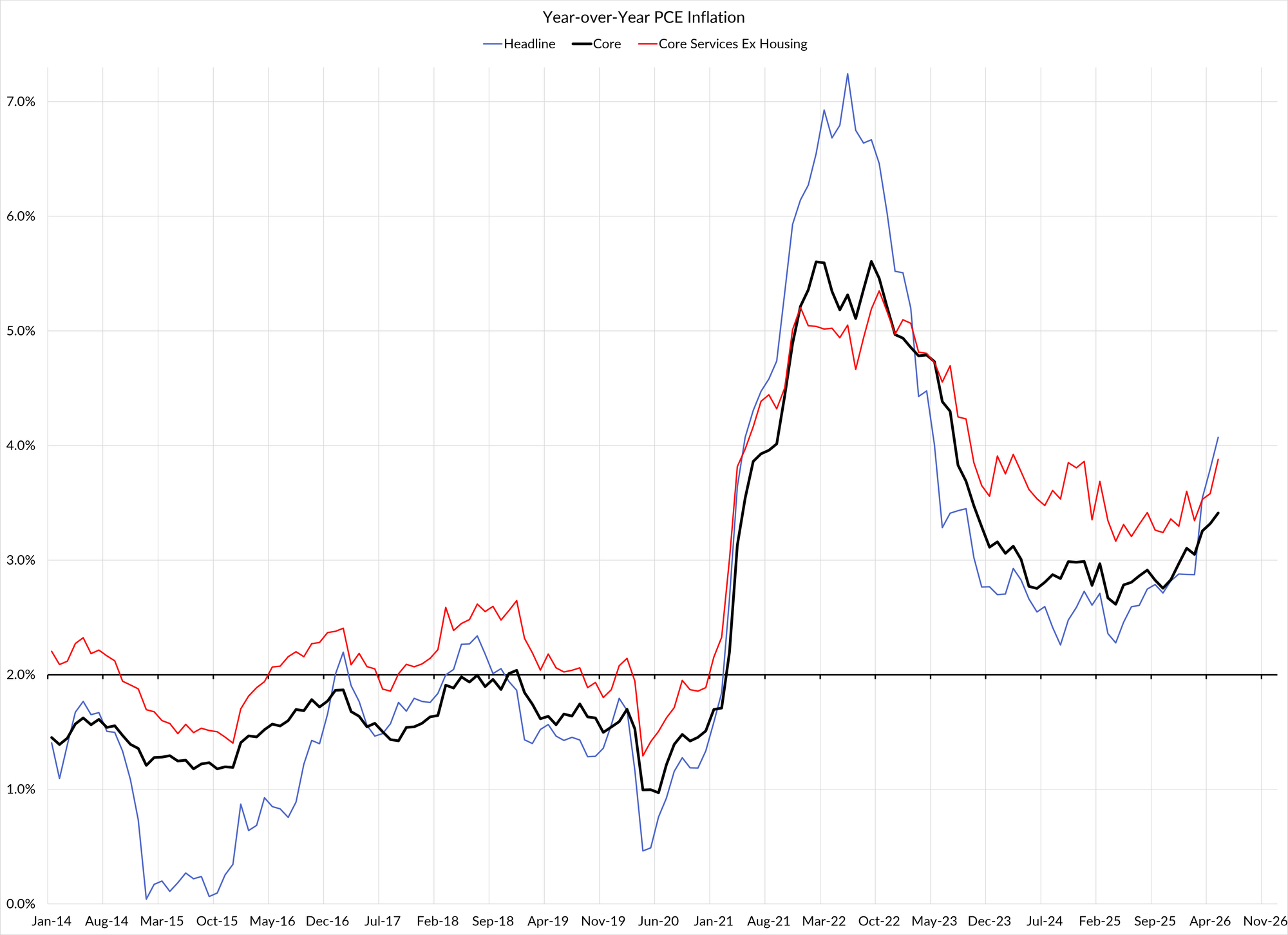

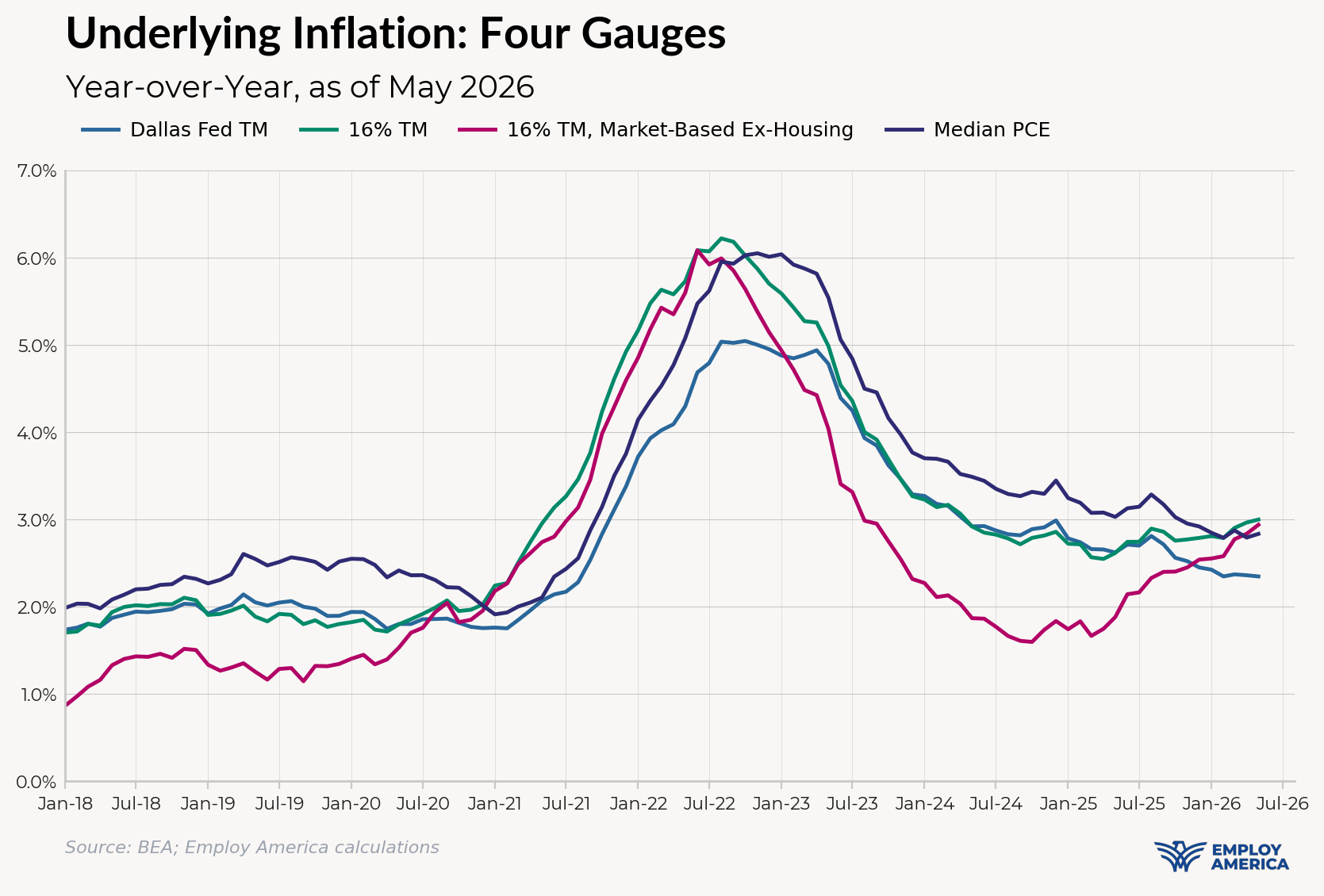

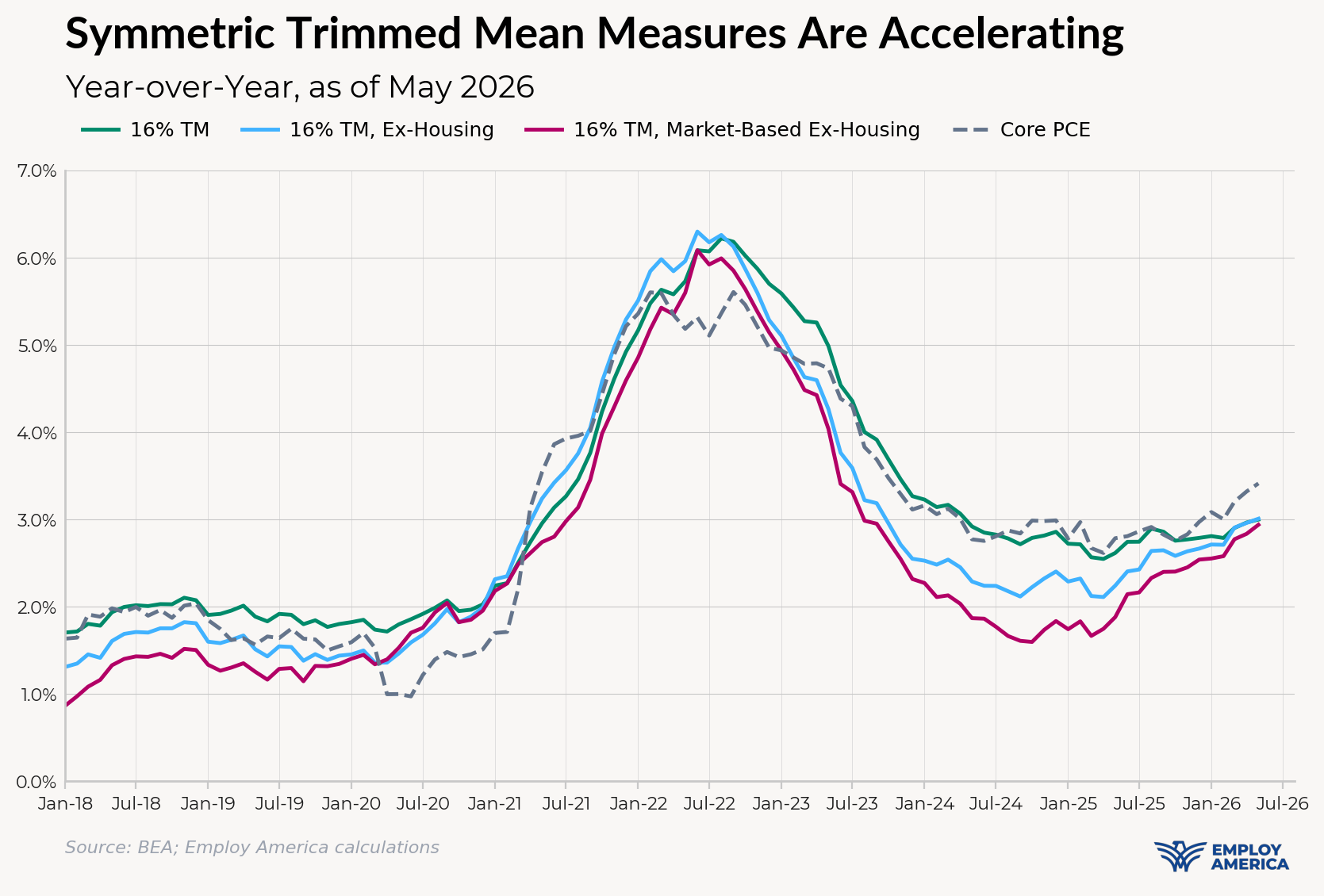

Chair Warsh's two presumably favored gauges continue to understate underlying inflation. Median PCE ticked up to 2.83% year-over-year, while the Dallas Fed Trimmed Mean held flat at 2.35%.

Our robust measure of inflation, 16% trimmed mean, market-based ex-housing continues to accelerate.

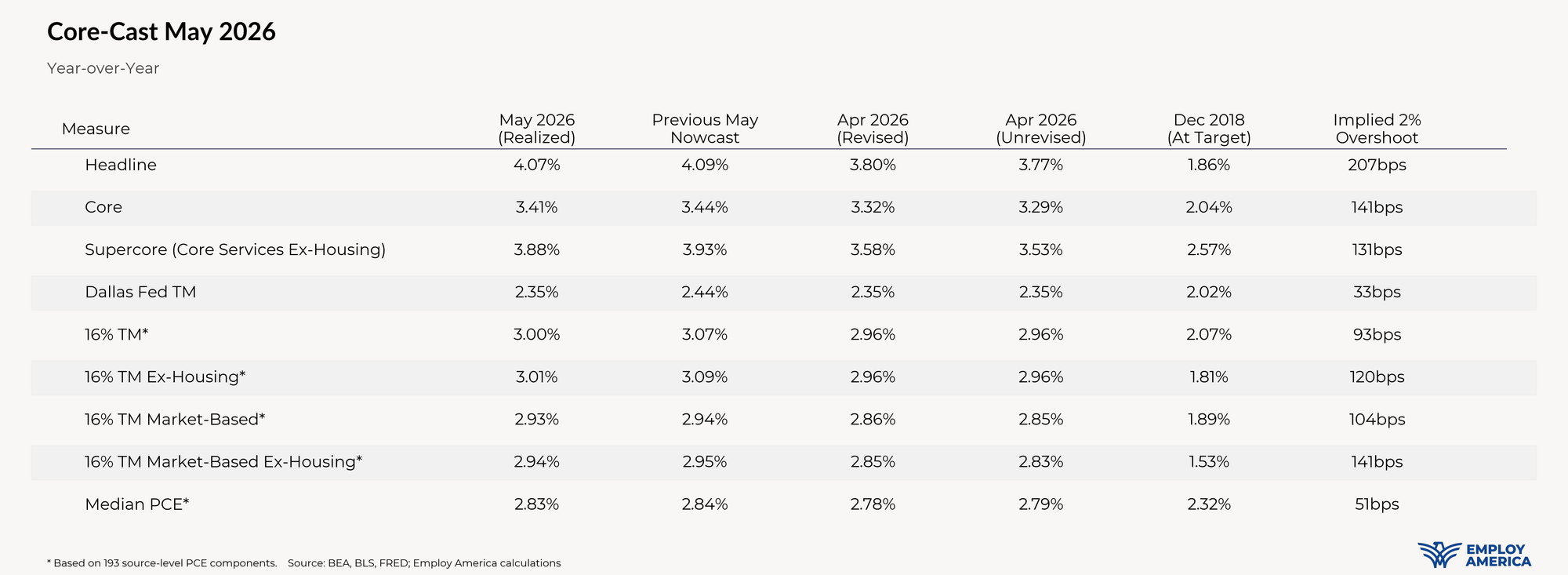

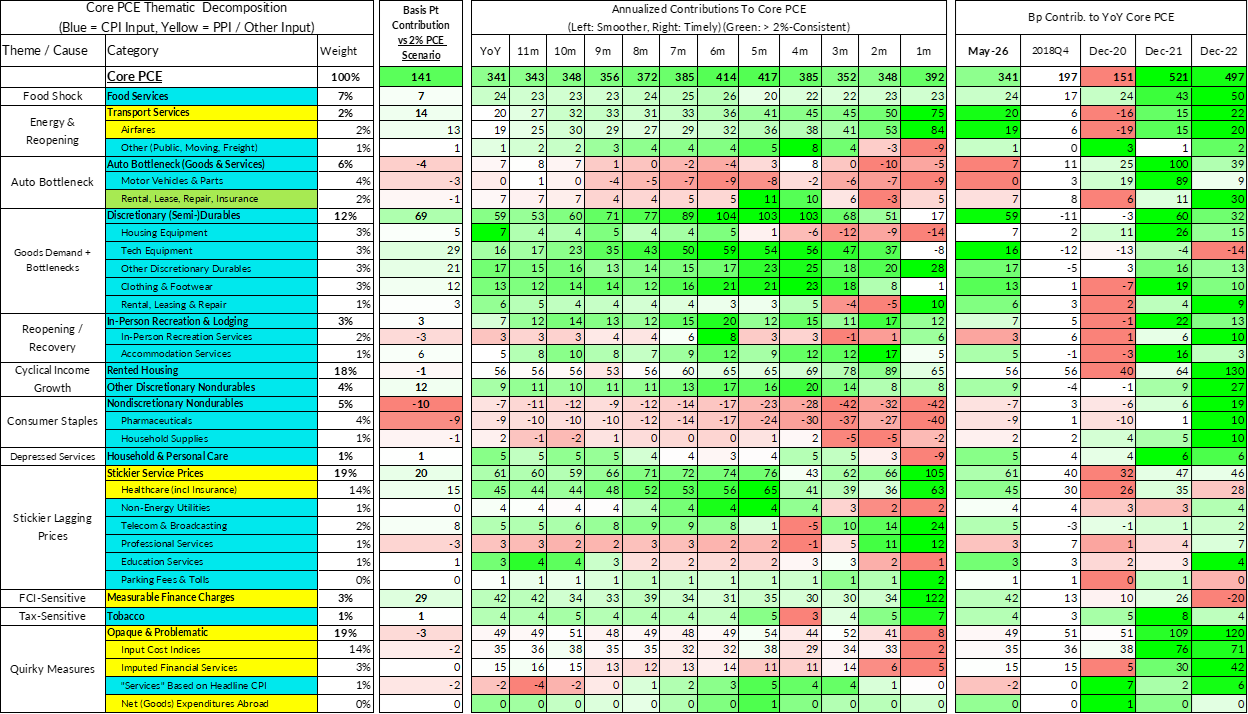

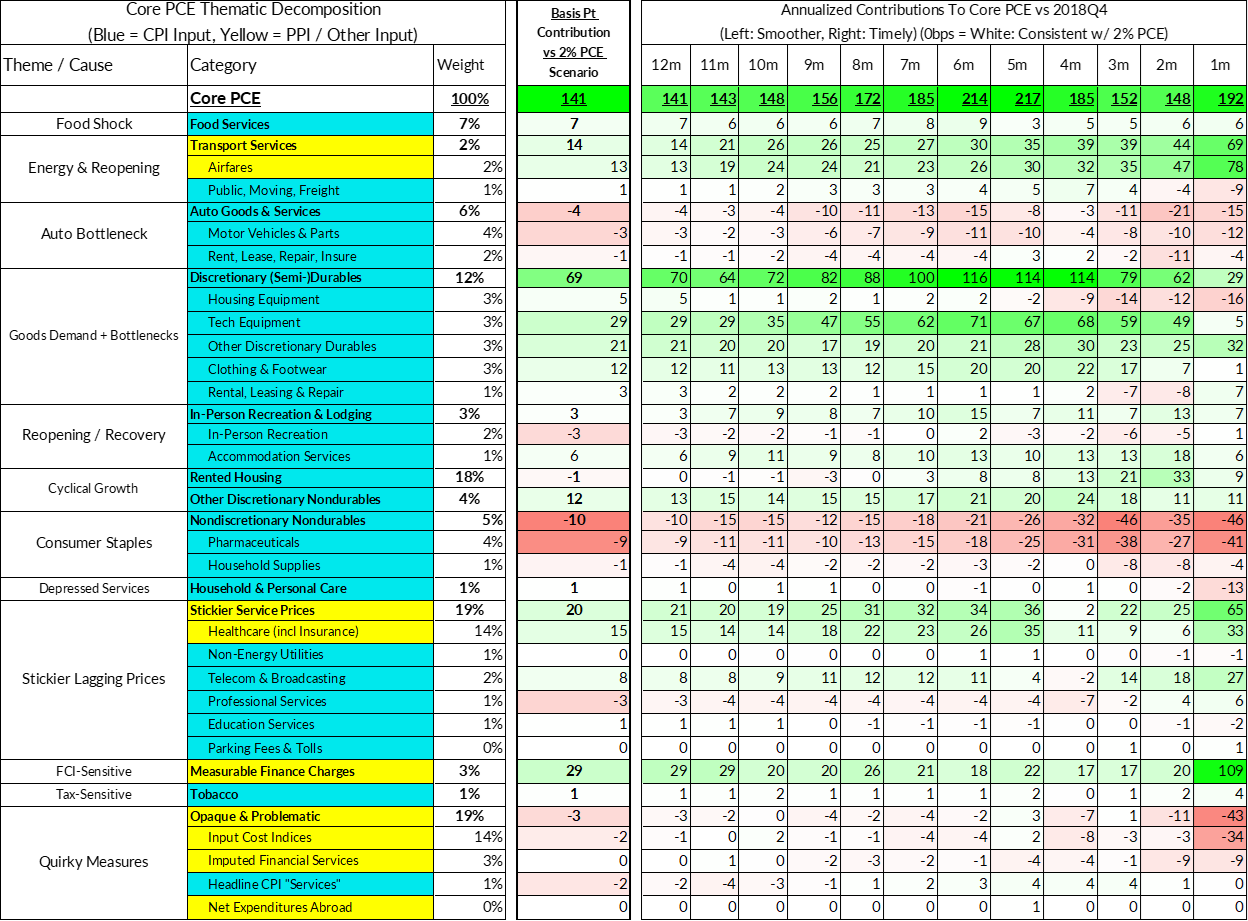

Core PCE (PCE less food products and energy) is running at a 3.41% year-over-year pace as of May, 141 basis points above the Fed's 2% inflation target for PCE.

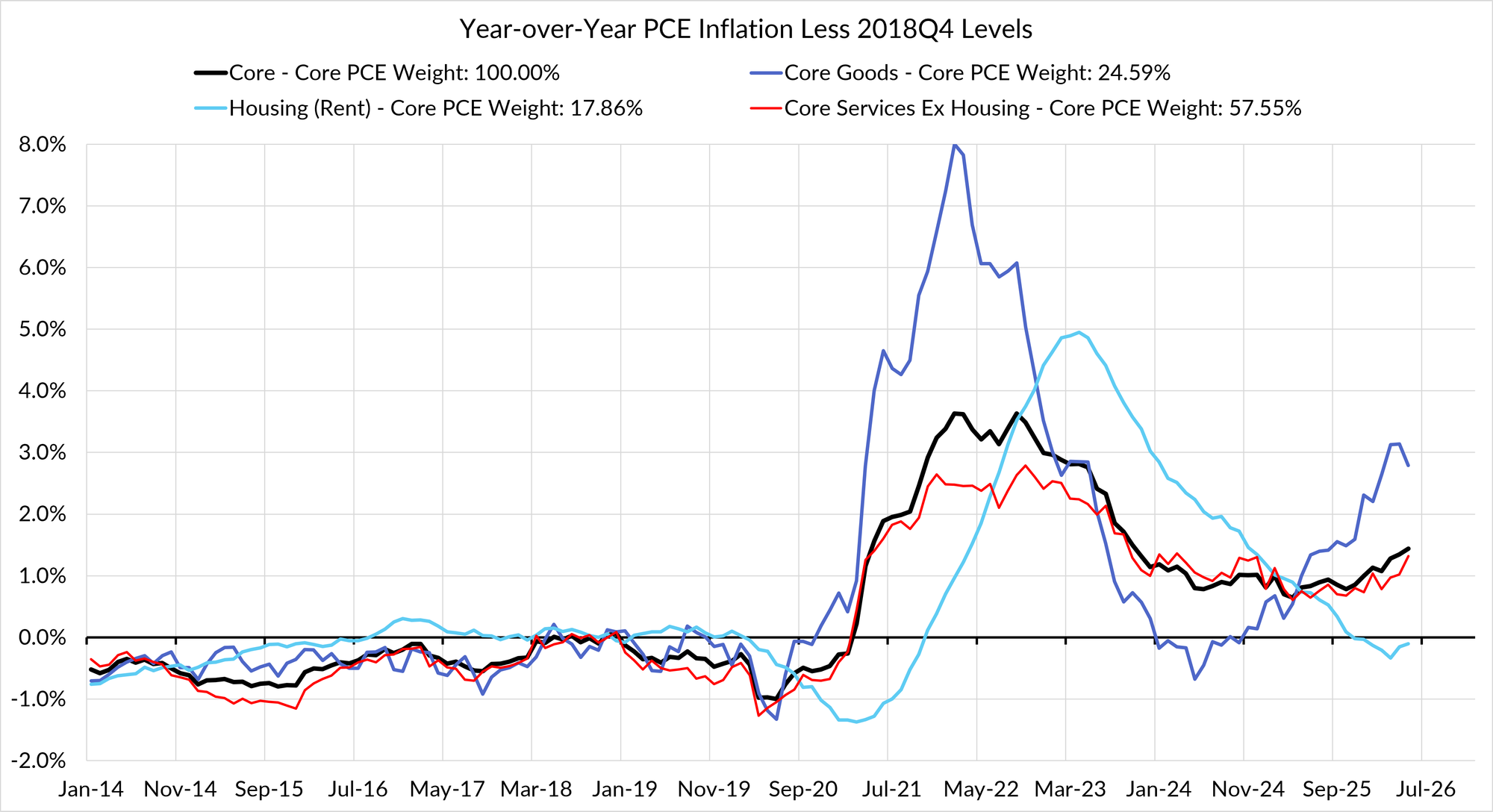

The contributors to the overshoot:

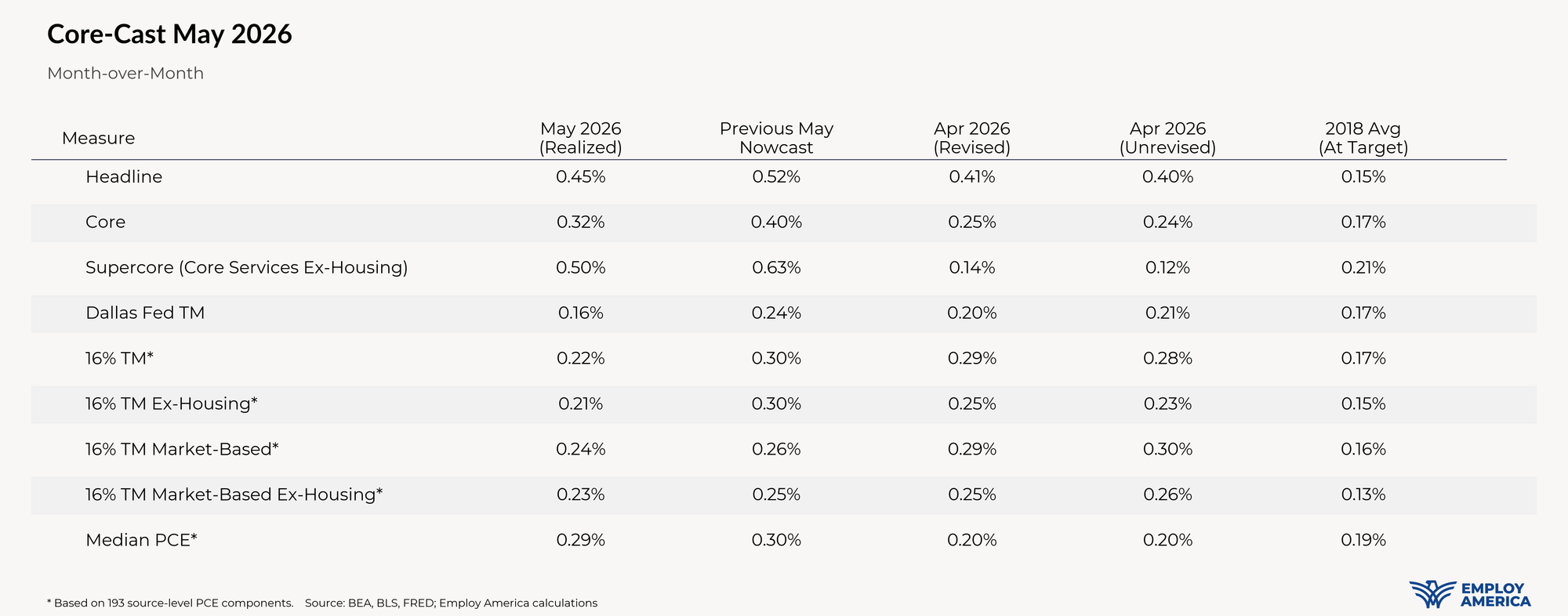

The second heatmap below gives you a sense of the overshoot on shorter annualized run-rates. May monthly annualized Core PCE is running at a 3.92% annualized pace, a 192 basis point overshoot vs 2% target inflation.

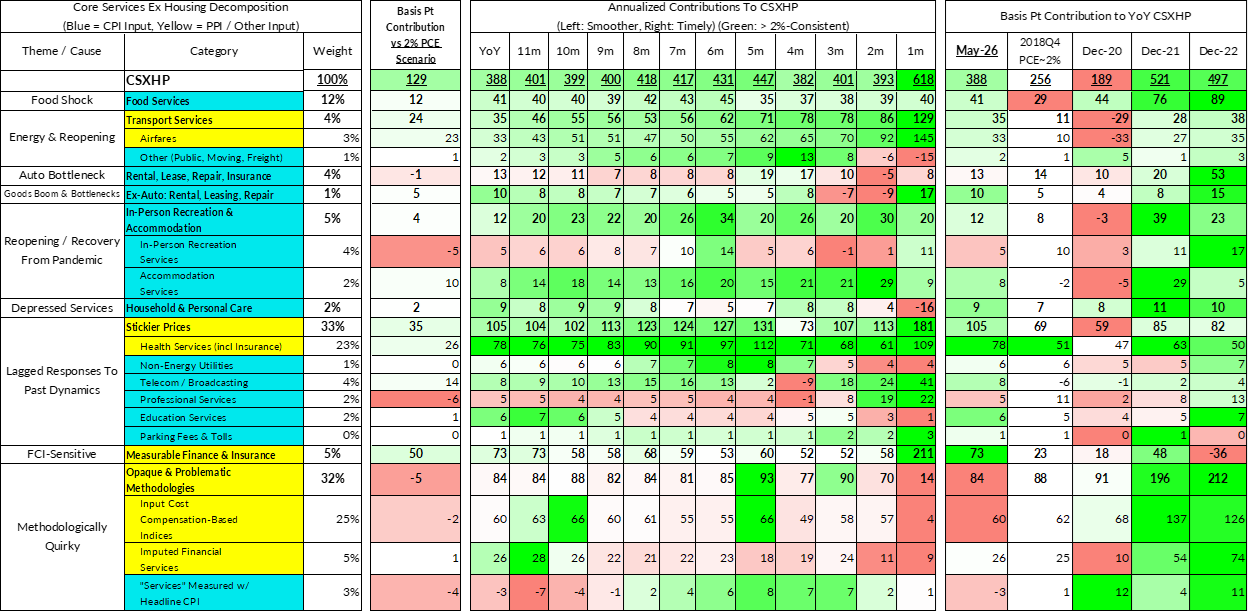

The April growth rate in "Core Services Ex Housing" ('Supercore') PCE is running at a 3.88% year-over-year pace, a 129 basis point overshoot versus the ~2.59% run rate that coincided with ~2% Headline and Core PCE inflation.

The May m/m Supercore is running at a 6.17% monthly annualized rate, a 359 basis point annualized undershoot of what would be consistent with 2% Headline and Core PCE.