The Fed in 2023: Buying into Deceleration

In this piece, we’ll take a look at how the Fed’s thinking on the labor market has changed as the data validated or disproved various hypotheses in 2023.

In this piece, we’ll take a look at how the Fed’s thinking on the labor market has changed as the data validated or disproved various hypotheses in 2023.

This is the first of a two-part series. As we near the end of 2023 and what appears to be the end of a Fed rate hiking cycle, it’s useful to take stock of how the Fed has changed over the past year and what that means for 2024. In this piece, we’ll take a look at how the Fed’s thinking on the labor market has changed as the data validated or disproved various hypotheses in 2023. In the next, we’ll discuss what this means for 2024 and what the Fed needs to do to achieve a soft landing.

At the height of the post-COVID inflationary episode, a particular narrative about the origins of, and solutions to, the problem of rapid price increases began to take hold. The monetary and fiscal stimulus used to propel the economy out of the pandemic recession had overheated the economy, causing inflation. At least that is how the story went. Rather than a sign of policy success and economic health, the historic low unemployment rate of 3.5% was said to be a sign that inflation would remain high or even continue rising.

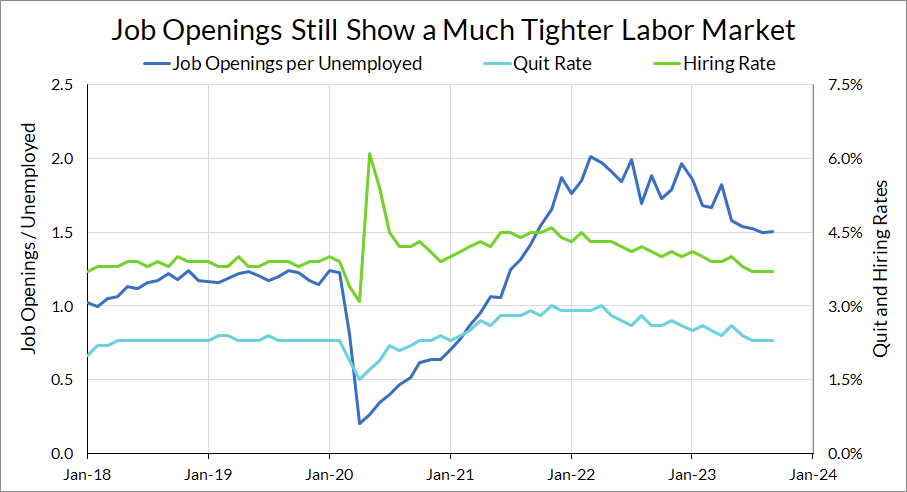

The evidence behind this story was limited even at the time. One key piece of evidence put forward in support of this hypothesis was the rapid increase in job openings and the outward shift of the Beveridge curve. At the peak, there were more than two reported job openings for every unemployed person, according to the JOLTS data. Cooling the economy enough to return to low inflation under these circumstances would, according to this story, require the Fed to raise rates high enough to cause a dramatic increase in unemployment. The exact extent to which unemployment was necessary differed depending on which prognosticator or hypothetical scenario (for a more precise summary of these projections, reread my previous research report, “Misled By the Phillips Curve”). On the whole, the clear takeaway from these arguments was that preserving the hard-fought labor market recovery was likely to prevent inflation from returning to target. The Fed would need to get tough and slam the brakes on the labor market. I’ll refer to these arguments as the “Braking” point of view (I also like that it sounds like “breaking”, as in “break the labor market”).

At Employ America, we have consistently put forward an alternative story. We argued that disinflation was possible without an increase in unemployment. By early 2023, there were already signs that price and wage growth were slowing, even as unemployment remained low. The employment recovery was rapid, but the return to full employment itself meant that aggregate labor income growth was set to slow, which would itself be disinflationary. These labor market dynamics, combined with the resolution of disrupted supply chains, would produce a dynamic which we called an “endogenous slowdown” at the time. Under this scenario, inflation would moderate even as employment remained strong.

This dynamic is akin to how a car decelerates when the driver takes their foot off the gas pedal, even if they don't touch the brakes. For that reason, I’ll refer to these arguments as the “Deceleration” point of view.

The past twelve months of data have proven decisive in favor of Deceleration. Despite a still-elevated job openings rate and still-low unemployment rate, inflation and wage growth have fallen significantly. The Fed—which never fully embraced either viewpoint— is thankfully taking notice, before it’s too late. But how did we get here, and what does it mean for the future?

At the start of 2023, the Fed had adopted a position somewhere in between these Braking and Deceleration. On one hand, and to their credit, they never fully embraced a hard Phillips curve view of inflation and the labor market. When Representative Ocasio-Cortez asked Powell about Summers’ theory that mass unemployment would be necessary to tame inflation, Powell declined to endorse those views:

“I think there’s so much uncertainty and in particular, the answer is going to depend to a significant extent on what happens on the supply side. If we do get these supply side problems worked out, which I think is certainly going to happen in time, then we wouldn’t see anything like that. But it’s a highly uncertain time; our intention is to bring down inflation while keeping the labor market strong.

Powell to Ocasio-Cortez, June 23rd, 2022

On the other hand, the Fed did see an increase in unemployment as an appropriate response (or inevitable price to pay) for disinflation. This intention was communicated most clearly in the December 2022 Summary of Economic Projections, in which the median FOMC member’s projection for unemployment by the end of 2023 under “appropriate monetary policy” was 4.6%. As we pointed out at the time, and as Senator Warren strenuously argued to Chair Powell, that trajectory was historically consistent with a Fed-induced recession. Powell also repeatedly cited the elevated level of job openings to unemployed as proof of an overheated labor market. For several meetings in a row, he centered the importance of the tight labor market in contributing to measured inflation in the core non-housing services aggregate, which comprises more than half the core PCE basket.

But throughout the hiking cycle, a question lurked: How would the Fed react if unemployment started rising while inflation stayed high? Would they pivot, away from rate hikes to preserve the historic labor market recovery? Or would they see such an increase in unemployment as a key part of the plan—and if that was what they were thinking, how far would they actually be willing to go?

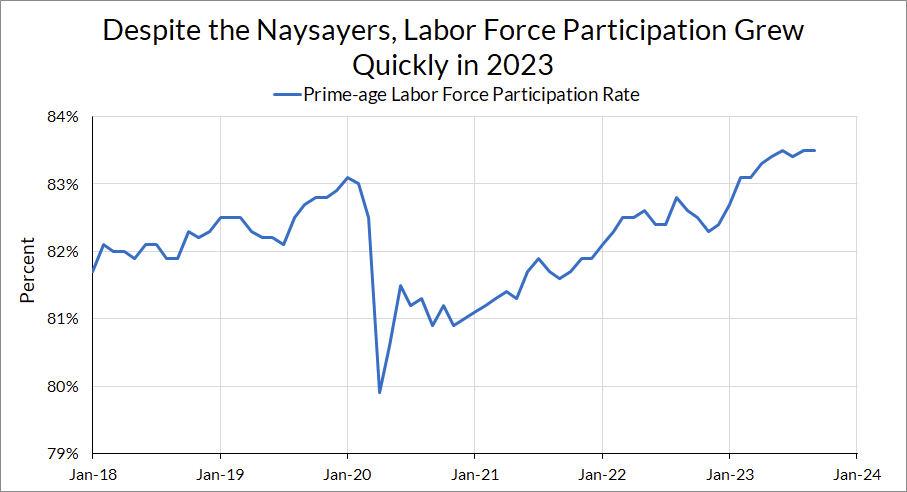

Thankfully we never had to find out the answer to that question: the unemployment never arrived, even as growth in prices and wages slowed substantially. The data in 2023 soundly rejected the predictions of models that relied on job openings data and Phillips curve frameworks to argue that disinflation would require substantial increases in unemployment. The unemployment rate has only risen to 3.9%, driven in large part by improvements in labor force participation. Even though the unemployment rate is higher than where it was a year ago, the prime-age employment rate, at 80.6%, is also much higher than where it was a year ago and tied with the peak pre-pandemic reading in January 2020. Real growth is poised to come in stronger than expected earlier this year and demonstrate meaningful acceleration.

Meanwhile, inflation has fallen across a wide range of measures. To take just one, the 12-month change in the core PCE index peaked in February at 5.6% and has now fallen to 3.9%. In short, 2023 was a test of the Phillips curve. It failed, the Fed has recognized it, and Powell knows it:

I don’t think most of the inflation we’re seeing at all is from the Phillips curve, though. It was really the collision of very strong demand, really strong demand, with constrained supply.

Jerome Powell, October 19th, 2023

The Fed’s tone on the labor market has evolved to reflect this reality. Discussions of the balance of risks have moved away from a single-minded focus on inflation and towards the “balance” of risks between unemployment and inflation. FOMC members are talking about the need to “proceed carefully.” As with the recession forecast at the beginning of the year, this change in tone is clearest in the SEP. The most recent report saw members revise their median unemployment rate projections down to 4.1% by the end of 2024. The Fed, in short, is no longer aiming for a recession.

It’s not just the high-level relationship between inflation and unemployment where the Fed’s perspective is evolving – the details of how they understand the labor market are changing as well. Take, for example, the use of job openings as a measure of tightness in the labor market. In March, we wrote that the job openings and quits data were telling diverging stories about how quickly the labor market was cooling, and that the Fed would need to choose which one of these stories they believed in. At first, Powell emphasized the importance of the ratio of job openings to unemployed workers and the rate of wage growth in gauging the tightness of the labor market. But more recently, at the Economic Club of New York, Powell talked up other labor market indicators in addition to job openings, and emphasized that they have returned to pre-pandemic levels:

In the labor market, strong job creation has met a welcome increase in the supply of workers, due to both higher participation and a rebound of immigration to pre-pandemic levels. Many indicators suggest that, while conditions remain tight, the labor market is gradually cooling. Job openings have moved well down from their highs and are now only modestly above pre-pandemic levels. Quits are back to pre-pandemic levels, and the same is true of the wage premium earned by those who change jobs. Surveys of workers and employers show a return to pre-pandemic levels of tightness. And indicators of wage growth show a gradual decline toward levels that would be consistent with 2 percent inflation over time.

Jerome Powell, October 19th, 2023

While this isn’t by any means a wholesale abandonment of the past emphasis on job openings data, it is encouraging to hear him talk more openly about a broader set of labor market measures. Now that those other measures have returned to pre-pandemic levels, it’s clear how much of an outlier the job openings data is. While quit rates and hiring rates have returned to pre-pandemic levels, the vacancy-to-unemployment ratio has not.

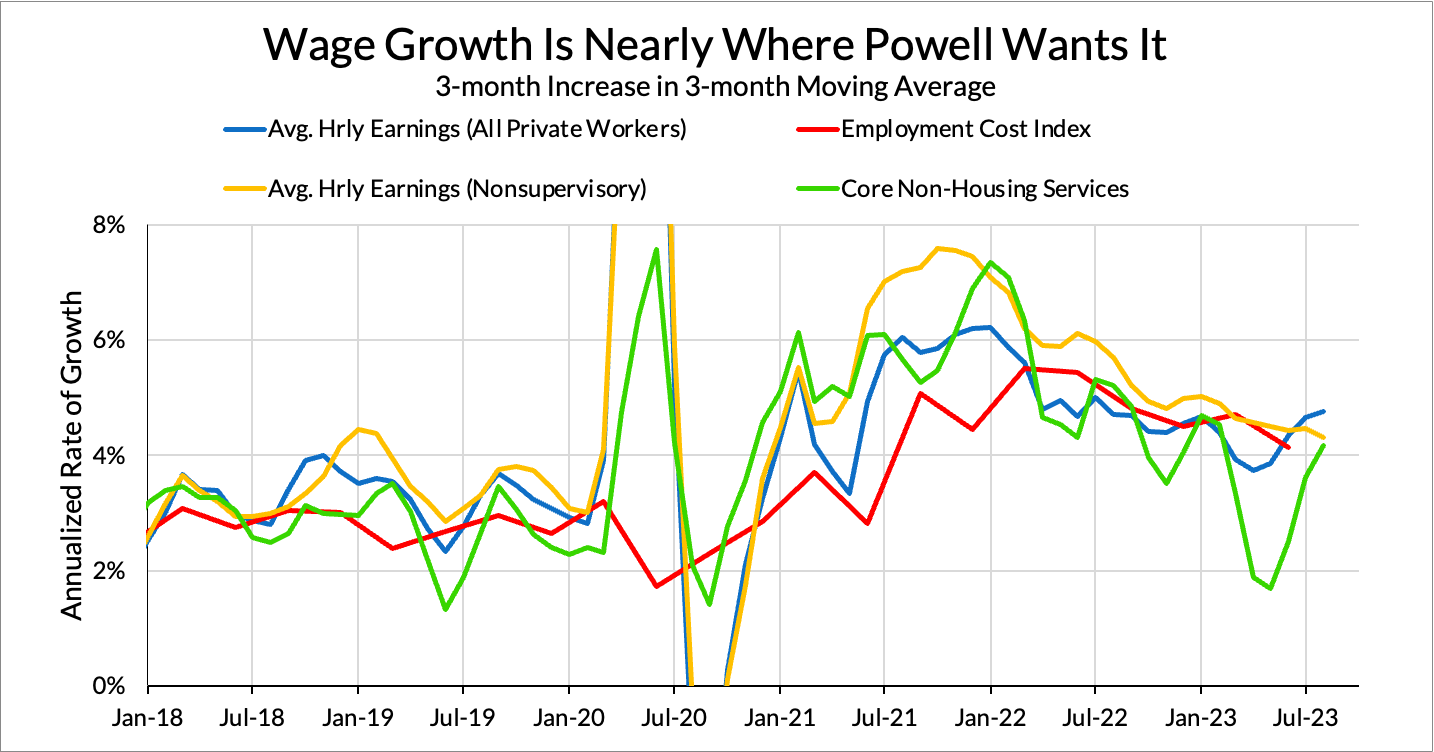

While wage growth varies on different measures, on all measures we see meaningful deceleration and if we look at the last 2 quarters, average hourly earnings is back to a pre-pandemic growth rate. As I wrote in our October 2023 labor market recap, is close to where Powell wants it. Based on his previous statements, we are near the level of wage growth the Fed considers consistent with 2% inflation.

Proponents of the job openings measure used to argue that it was superior because it was better at predicting wage growth and inflation. However, if anything, job openings appear to lag other labor market indicators during this episode. By the end of 2022, quits and hires were presaging a slowdown in the labor market, while the vacancy-to-unemployment rate was still roughly 40% above its prepandemic peak and only marginally lower than post-pandemic peak levels.

The problem doesn’t go away if one tries to fit more sophisticated Phillips curve models using job openings to the data. As I wrote earlier this year, models attempting to forecast inflation and wage growth conditional on paths of the vacancy-to-unemployment rate (such as Domash and Summers (2022) and Ball, Leigh and Mishra (2022)) missed the mark quite badly.

Powell has also recognized his previous error in underestimating the recovery in labor supply, another phenomenon we also highlighted back in March.

I personally thought, well, I guess we won’t get any [more labor supply], and then we’ve gotten a substantial amount this year. The female labor force participation [rate] in prime-age workers is at an all-time high, which has to be related in some way to work from home. But labor force participation increased, immigration increased, and now you see that in the overall cooling of the labor market.

Jerome Powell, October 19th, 2023

Labor force participation improvement did, at first glance, look like it might be dead near the end of 2022. But in just a matter of months, the measure built a head of steam, with prime-age labor force participation increasing a whopping 1.2 percentage points from November 2022 to June 2023. As we and others argued, causality runs both ways between labor force participation and labor market tightness: a good labor market draws people in from the sidelines.

Finally, the improvements on the inflation front over the past year have vindicated proponents of a supply-driven story of inflation during this episode. The improvement in supply chains in 2023 has been real, and you can see it in the granular inflation data. As I wrote in my piece on Phillips curve predictions:

In the end, those who focused on the supply-side explanations of inflation would prove to have a better understanding of the dynamics behind our inflation problems (even if some predictions on that front underestimated the time it would take for those issues to resolve). The “supply side” of the economy can be subject to dynamic and durable shocks, and it spans much more than what the unemployment rate or wage growth can capture. Physical capacity challenges and commodity shortages were important features of the current inflationary episode. Going forward, understanding the supply side will continue to be key to understanding inflation.

Misled by the Phillips Curve: How Inflation Predictions Went Wrong (Preston Mui, Employ America)

By contrast, Phillips curve-centric models gave insufficient attention to the supply side of the economy, since the framework encourages researchers to try to explain inflation or wage growth using measures of labor market slack. However, even a relatively sophisticated Phillips curve model in Ball, Leigh and Mishra (2022) that attempted to model inflation shocks (including supply shocks) and their effect on overall inflation failed to capture the overall disinflationary effect of supply chain improvements, predicting almost zero effect of negative inflation shocks on headline inflation.

Powell sees it too. Again at the Economic Club of New York, he described this inflationary episode as “really the collision of really strong demand with constrained supply—cars being a great example.”

In short, in 2023 the Fed was presented with two frameworks: Braking and Deceleration.

According to those who argued for Braking, inflation came from the tight labor market, as evidenced by the historic elevation in the number of measured “job openings.” Supply chains were a secondary concern; what really mattered was inducing slack in the labor market. Getting this slack would necessitate moving along the Beveridge curve and increasing unemployment, perhaps to levels consistent with a deep recession.

By contrast, Decelerationists argued that inflation was largely driven by constrained supply stemming from pandemic disruptions to supply chains and one-off recovery in the prices of services kept suppressed by the pandemic. It would take time for the economy to fully adjust to these shocks, but with time, their impulses would fade and inflation would normalize. The high level of the employment was not the primary cause of this inflation, and the labor market was cooling in any case, as could be seen if one looked to robust indicators like quits and hiring. Disinflation could be achieved without recession.

The data has favored Deceleration, and the Fed is following suit. While Powell described the soft landing path as “narrow” earlier this year, it has since “widened” over the duration. Bostic and Goolsbee are now optimistic that we are on the “golden path” to a soft landing.

Which brings us to 2024. Now that the Fed is no longer aiming for a recession and is now explicitly (through its projections) aiming for a soft landing, what do they need to do to achieve that? That will be the topic of the next piece in this series, but the questions are going to look very similar to the questions they faced in 2023. How tight is the labor market, and how much can things slow without triggering a recession? Are there still supply side improvements remaining that will continue disinflation, and how does monetary policy affect the trajectory of the supply side? Getting those questions right will prove key to making the soft landing a reality.