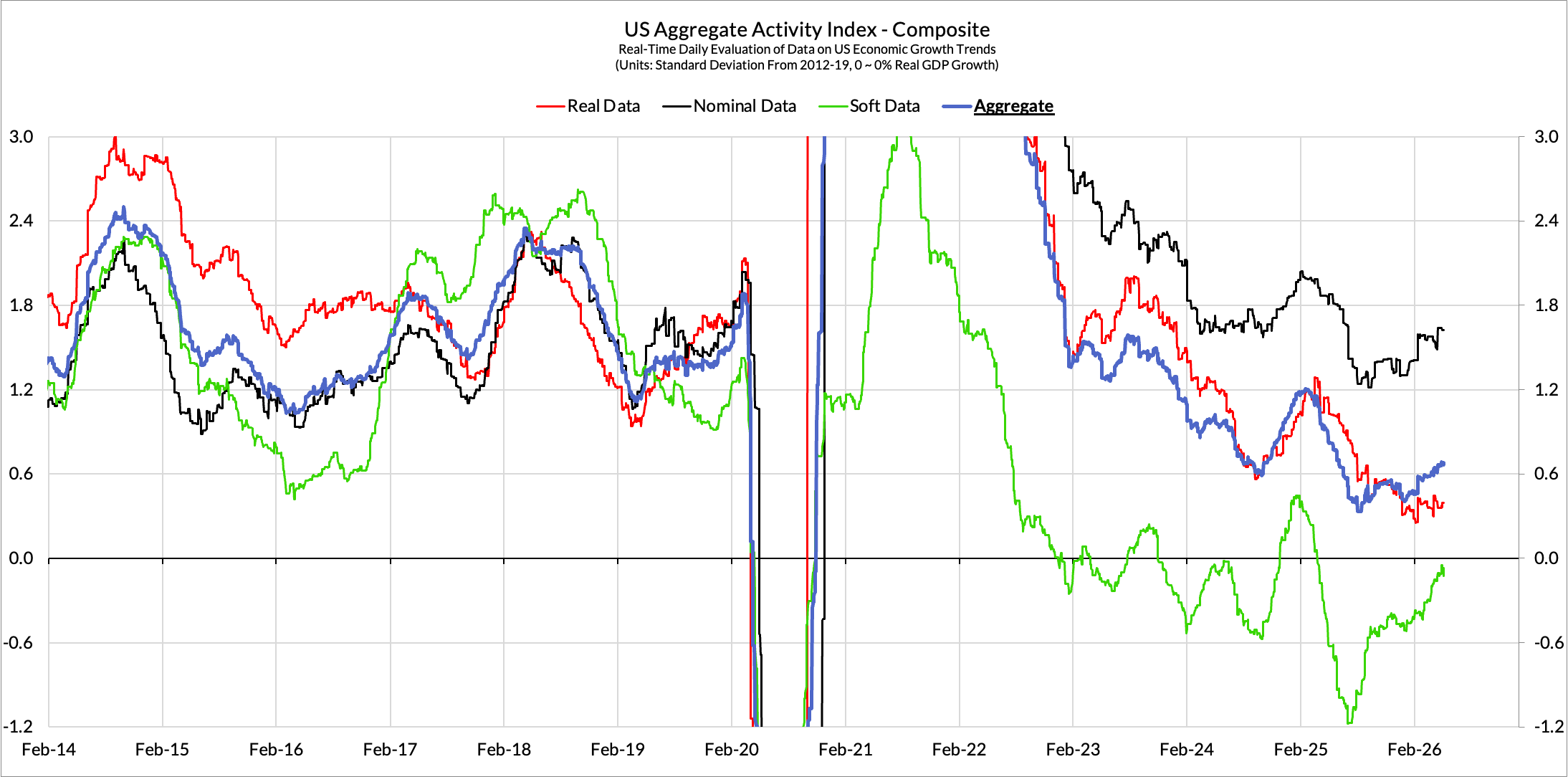

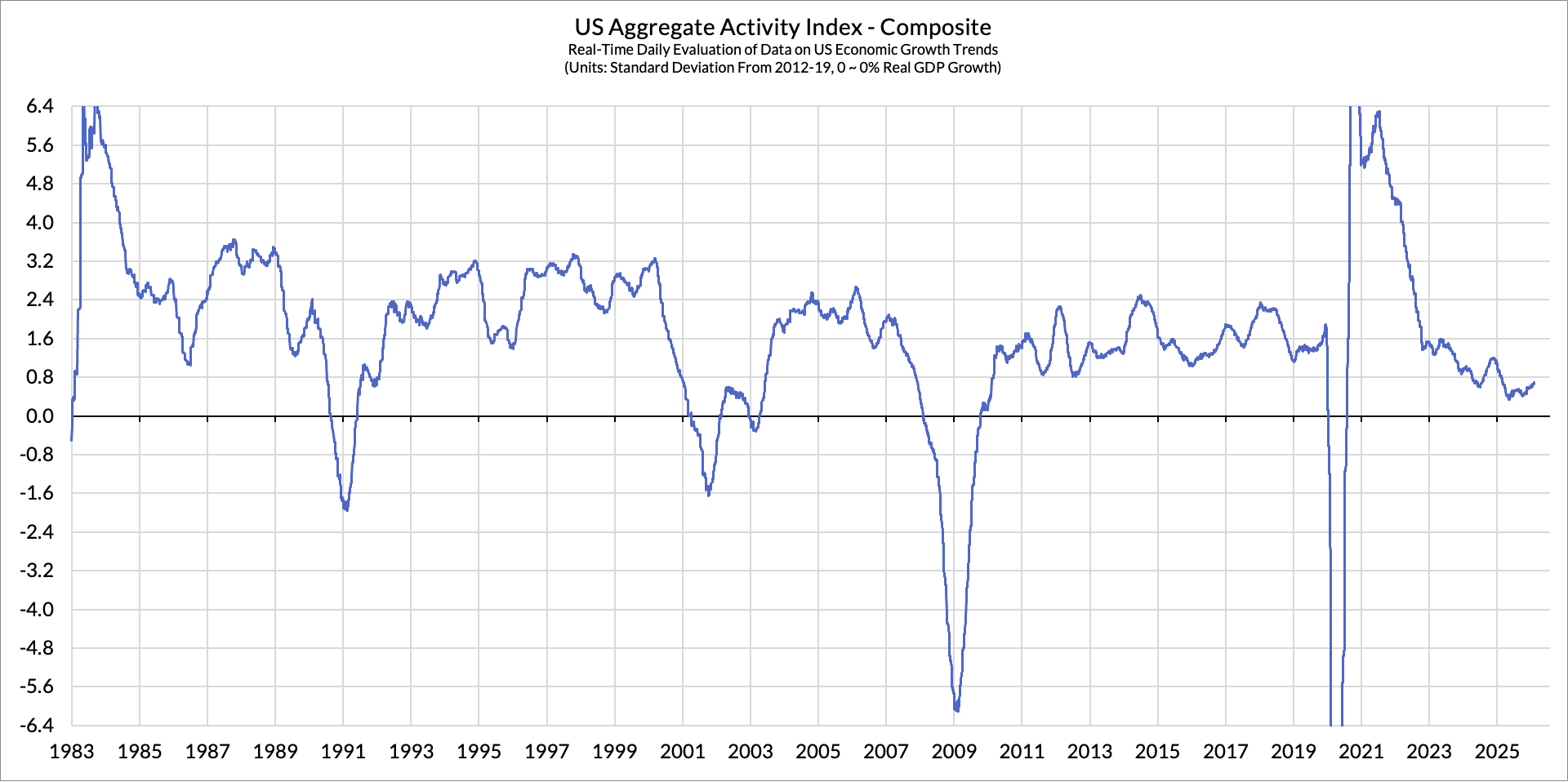

This monitor tracks US growth data in real-time, aligned to the timing of each release. It is a more timely & meaningful gauge of activity growth than GDP or other summary indicators. Please see here for more details.

Summary: The data trends of the past two weeks continues to push the macroeconomic tradeoffs more firmly towards upside inflation risks and away from the downside risks to growth. Q1 GDP surprised us marginally due to some stronger than expected government spending tied to the relief from the shutdown. While Q2 GDP is likely to show more of a mark from the Hormuz shock, we still see decent trends in US economic activity. In the face of persistent upside inflation surprises, the stable trends in activity are a reason for the Fed to continue shifting hawkishly.

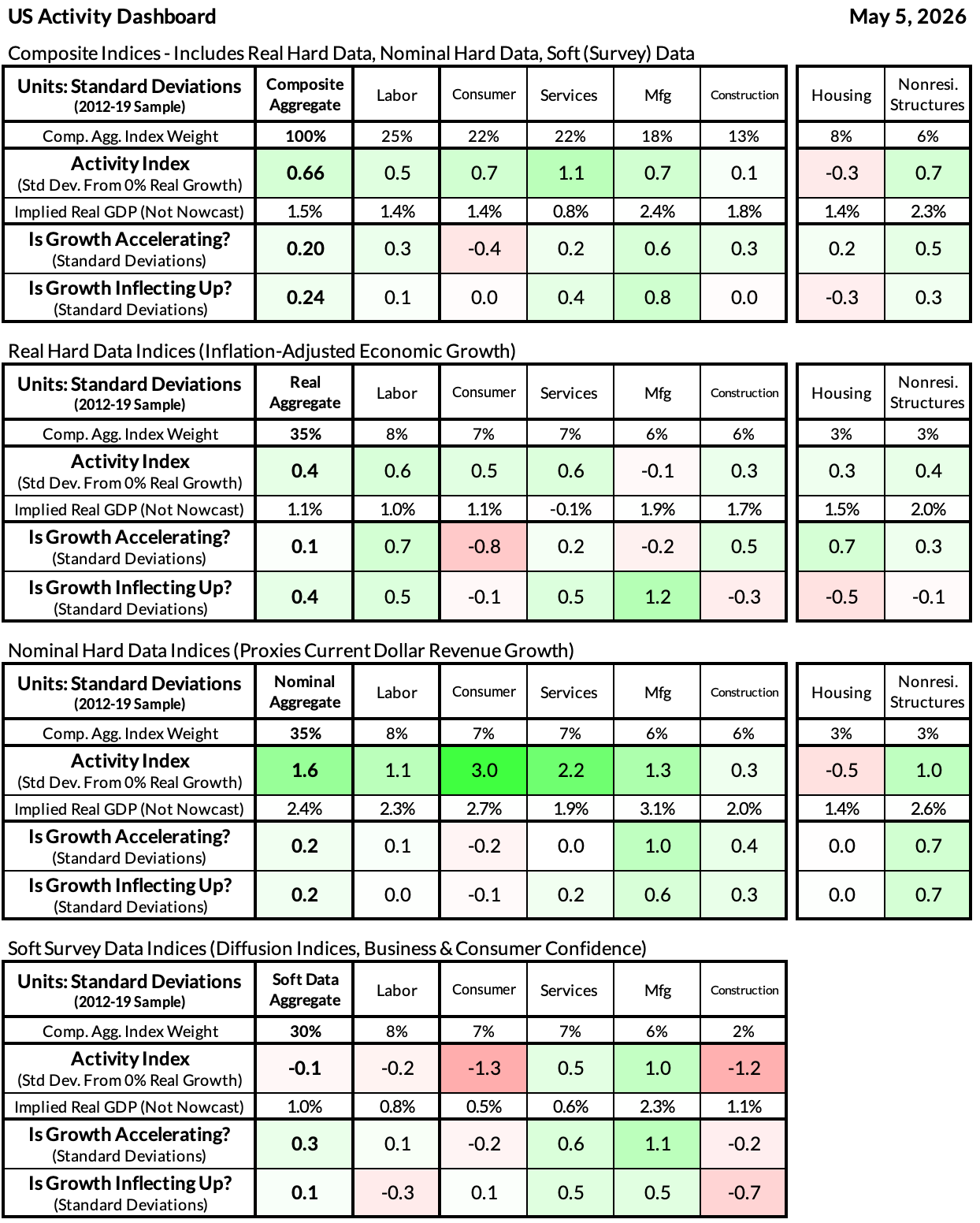

Data Developments

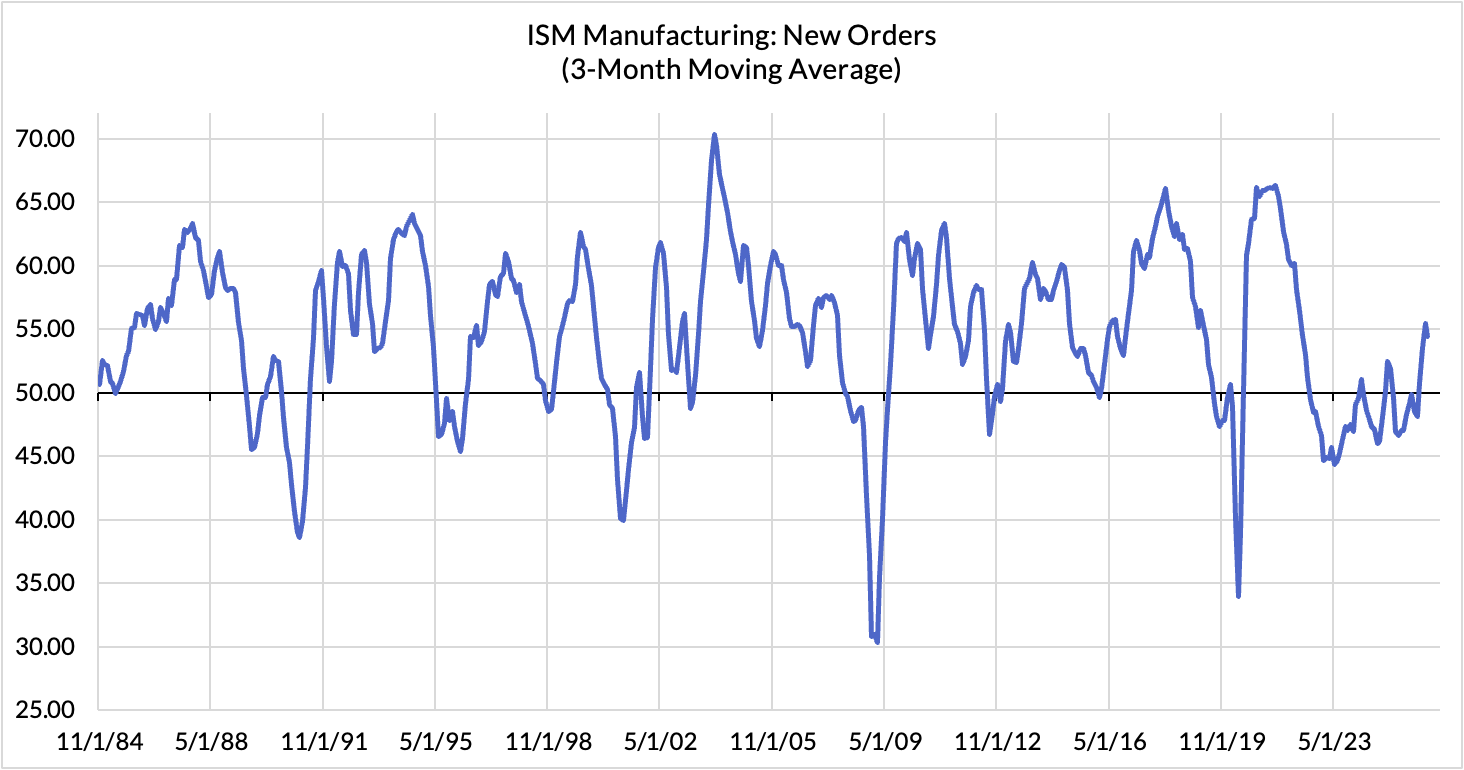

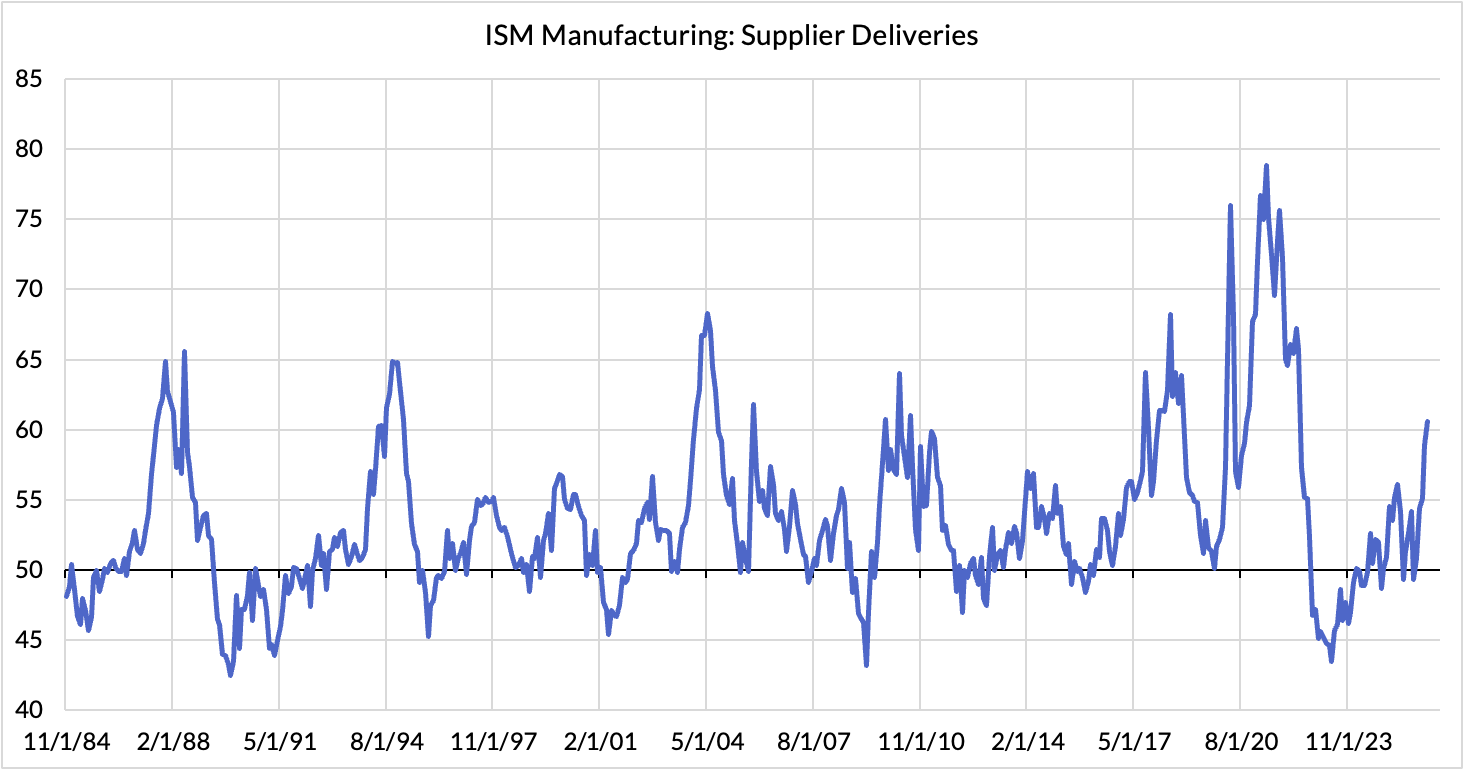

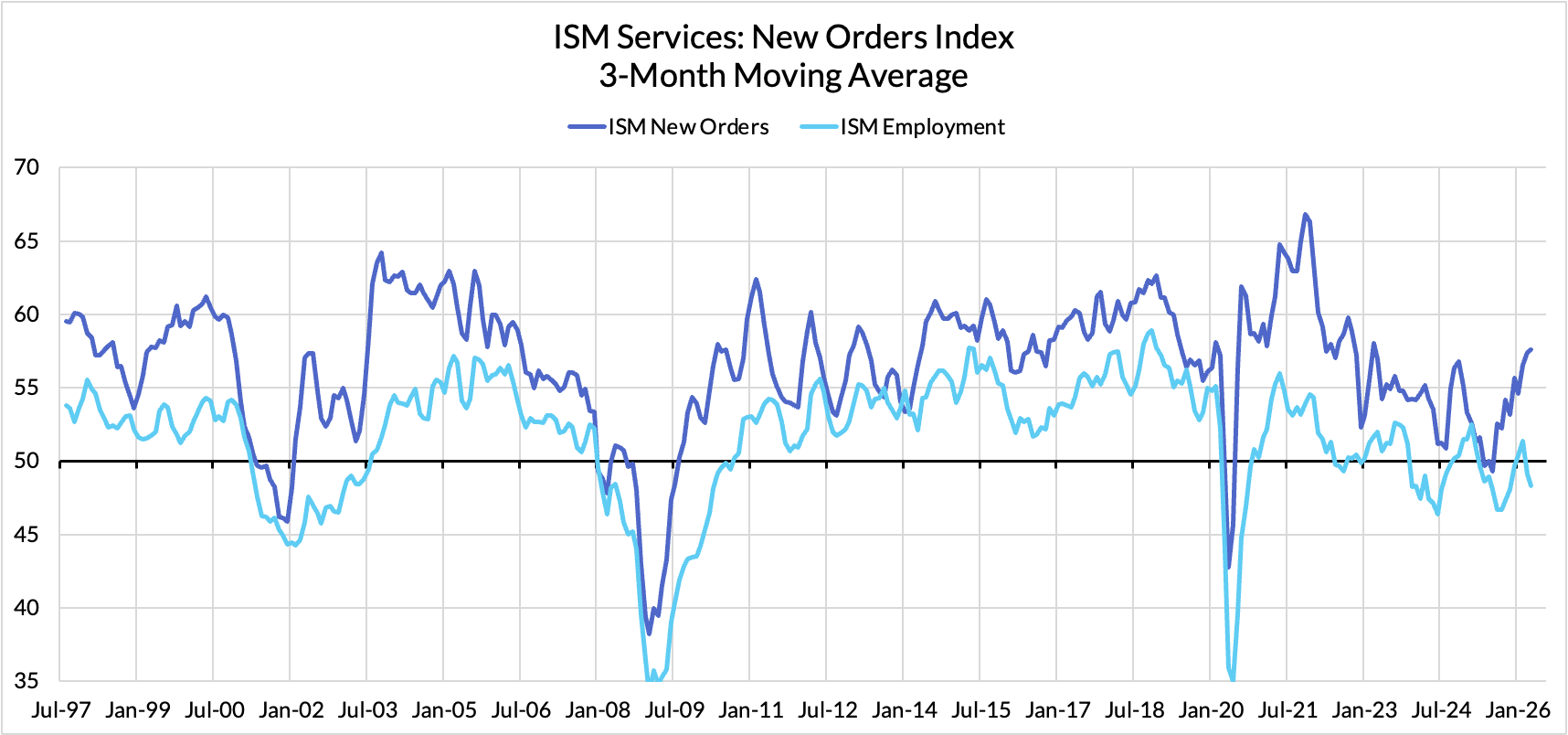

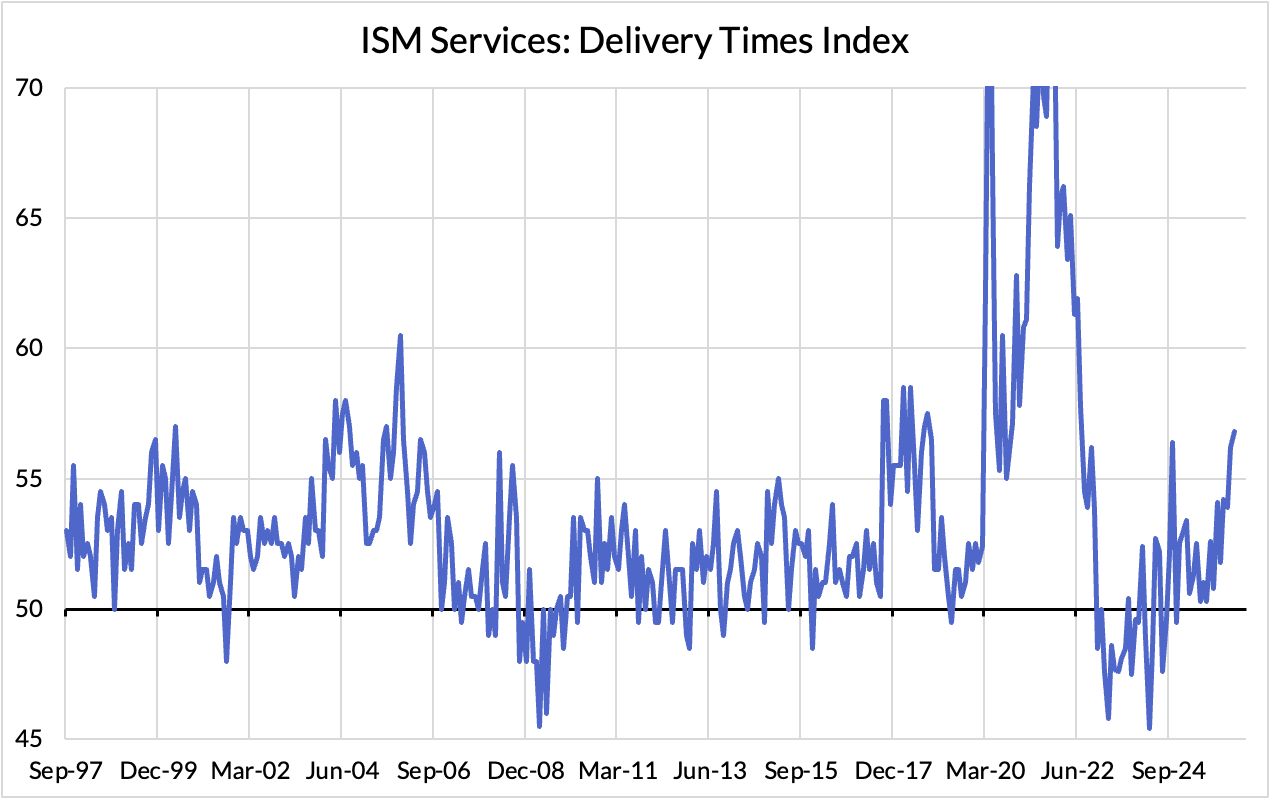

(1) The Soft Data Is Consistent With Continued Growth Improvement and Inflationary Pains

The ISM surveys deliver a straightforward takeaway: growth trends are accelerating, and with them, supply constraints are binding more tightly. New orders are growing in the manufacturing and services subsectors, while delivery times readings are also hitting new highs, indicative of a transportation service bottlenecks. Supply chain tightness is liable to exacerbate inflationary pressures that were already of concern in the past few months prior to the Hormuz closure. A growth trajectory far from the left tail and and inflation trajectory more consistent with the right side of the distribution adds up to a hawkish trajectory for Fed policy

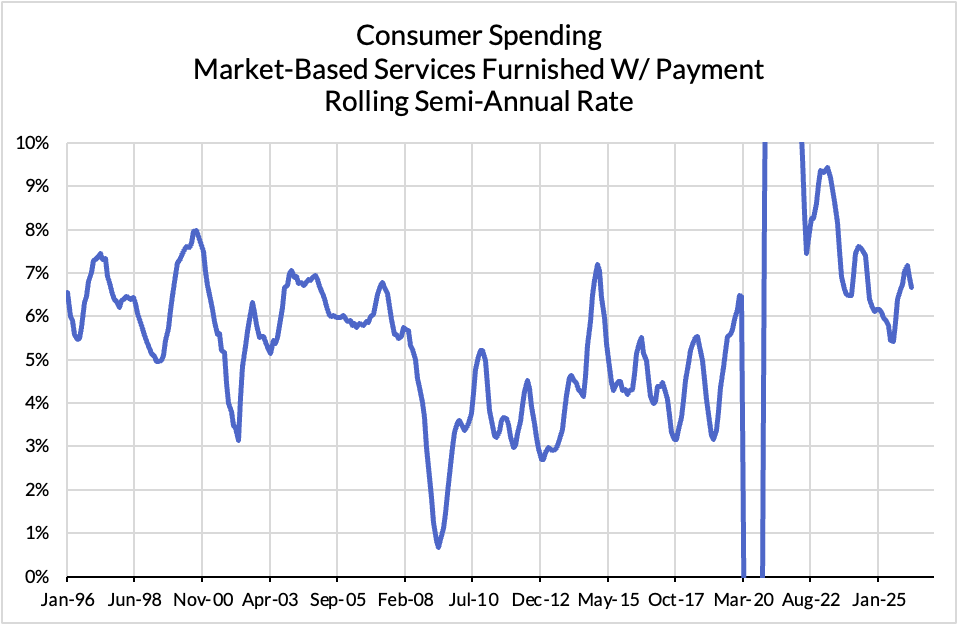

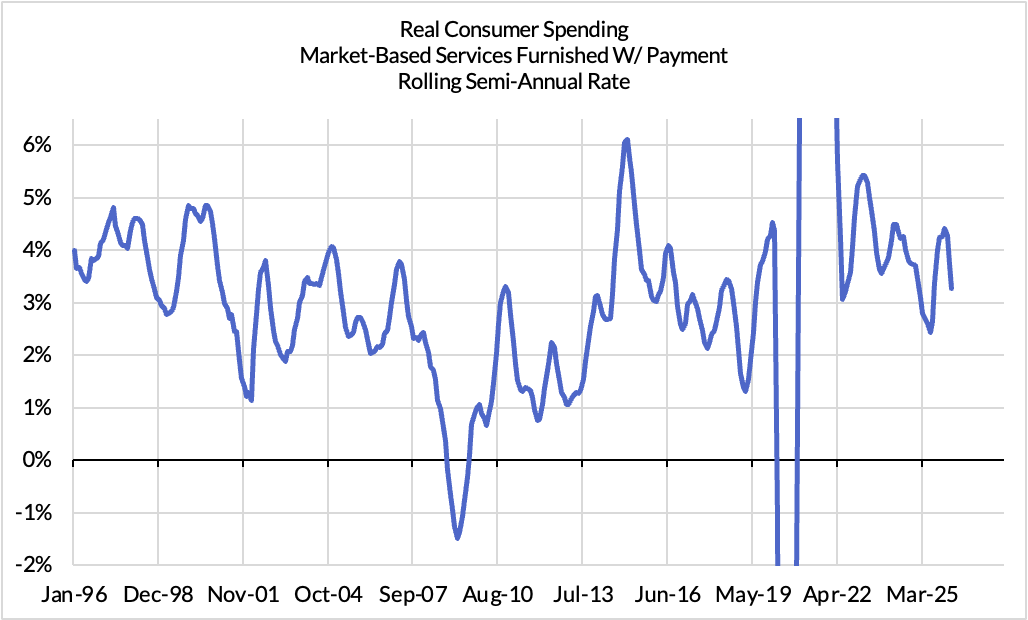

(2) Consumers Have Spent Aggressively On Services. We May Be Due For A Bigger Correction Soon

The March PCE data showed some marginal deceleration in nominal and real services spending trends for consumers. Real food services consumption has been very soft in the past several months and quarters, but healthcare spending has continued to outperform its pre-pandemic pace in both real and nominal terms. Some of this might be attributable to demographics, but especially with more inflationary dynamics emerging, we expect to see some slowing in the coming three quarters.

Our Baseline Views of US Activity

We underestimated a few things in Q1 GDP:While none of our component level nowcasts were that far off, each cut in the direction of upside surprises. The government shutdown snapback was larger than anticipated, while consumer spending on services also came in on the stronger side of what we were anticipating. Meanwhile, private final demand also came in much stronger due to surging imports for information processing equipment. We had anticipated robust fixed investment demand tied to the AI boom but apparently not enough. Business fixed investment is taking up an increasing share of nominal GDP, and is now clearly in excess of what prevailed in the 2010s.

Even with these forecasting misses, productivity growth in Q1 is still set to be a measly ~0.5% in Q1, far from the outbreak that Kevin Warsh has premised some of his dovish arguments.

We are expecting real GDP growth to be 1.2% for 2026Q2. March weakness tied to higher commodity prices was significant, but the effects on quarterly real GDP data are primed to be backloaded into Q2 relative to Q1. There will also be noticeable effects on structures and equipment investment if material costs persistently spike and raise corresponding deflators.

The Hormuz shock will still be more likely to exacerbate inflation than to tip the US business cycle into a full-blown recession: If two negative quarters of real GDP growth were enough to call a US recession, 2022 had that same phenomenon (before later revisions). But business cycles are fundamentally risk cycles and while there are real risks and uncertainties tied to the Hormuz shock, it isn't yet evident how this shock will permanently impair risk-taking (hyperscalers calling time on their investment surge might be one such channel, but we are not seeing evidence to that effect yet).

The US economy can handle higher oil and refined product prices better than most other countries given the persistently strong dollar and the availability of cheap natural gas. There is still a breaking point on how much of a commodity price surge the US can stomach, but we are far from that breaking point right now. The dollar is liable to strengthen in an environment of US growth outperformance.We are reminded of how the tech boom kept going through the late 1990s even as the Asian Financial Crisis drove a global recession and a US manufacturing recession. We see some parallels to the current moment, where the Hormuz shock could be incredibly nasty for many advanced and emerging economies, global energy prices make new all-time highs, and yet the US economy and its tech boom skate through, breeding imbalances and papering over weaknesses in other cyclical sectors.