Disinflationary Dynamics: Beyond Unemployment

At the Senate Banking Committee’s Humphrey Hawkins hearing on Tuesday, Senator Warren questioned Chair Powell about the implications of the Fed’s projections for unemployment, which call for an unemployment rate of 4.6% by year’s end, around an additional two million people without jobs.

Powell was resistant to say plainly that this is what the Fed is aiming at:

WARREN: I’m looking at your projections, do you call laying off 2 million people this year not a sharp increase in unemployment? Explain that to the 2 million families who who are going to be out of work

POWELL: We’re, again, we’re not targeting any of that, but I would say that even 4.5% unemployment is better than most of the time for the last 75 years.

To Warren’s point, these projections are the FOMC participants’ views of economic variables under “appropriate monetary policy.” Make no mistake: the committee believes that an increase in the unemployment rate is a necessary step in order to reduce inflation.

Other Fed officials have been more explicit about their view that unemployment needs to rise in order to reduce inflation. SF Fed President Daly went so far as to argue that low unemployment was an issue in and of itself, even independent of the wage growth argument that Powell has been leaning on:

[Some say we can just reduce vacancies]. I just don't think so. My own projection for the unemployment rate is that we have to go into the mid-4s or slightly higher on unemployment to get the sort of relief of the unemployment in the labor market we need to bring things back in balance…. the wage growth itself is not the problem. The problem is the labor market is out of balance.

Mary Daly, December 16th, 2022

Is it true that to get disinflation, unemployment must increase? Not so fast. There are several paths through which the Fed’s tools can lead to disinflation even without aiming directly at an increase in unemployment. The important thing is to realize that the labor market acts on inflation primarily through its effect on labor income, which is tightly linked to demand. More specifically, the speed of labor utilization increases, rather than the level, is the important determinant of labor market-driven inflation.

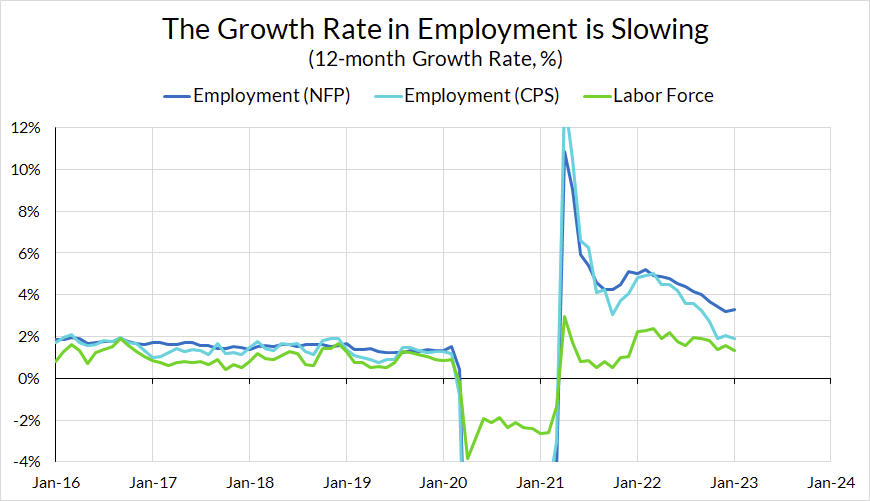

The first component of labor income is employment. To the extent that employment growth slows, so too does labor income growth. During the runup in inflation in 2021, we called out the rapid speed of employment gains as one cause of elevated inflation at the time. Since then, the growth rate in employment has been falling.

The exact speed of the deceleration is unclear, due to the discrepancy between the household and establishment surveys, but the general trend is clear: employment growth is slowing. If the growth rate of employment continues to fall, but stays around the growth rate of the labor force, the unemployment rate will remain steady but the growth rate of labor income will fall.

The second component of labor income growth is wage growth. As with employment, a slower growth rate in wages also slows labor income growth. We’ve seen substantial wage disinflation as well, even as the unemployment rate remained low in late 2022. This is consistent with the labor market cooling in general, as the rate of quits and hiring has returned to near pre-2020 levels.

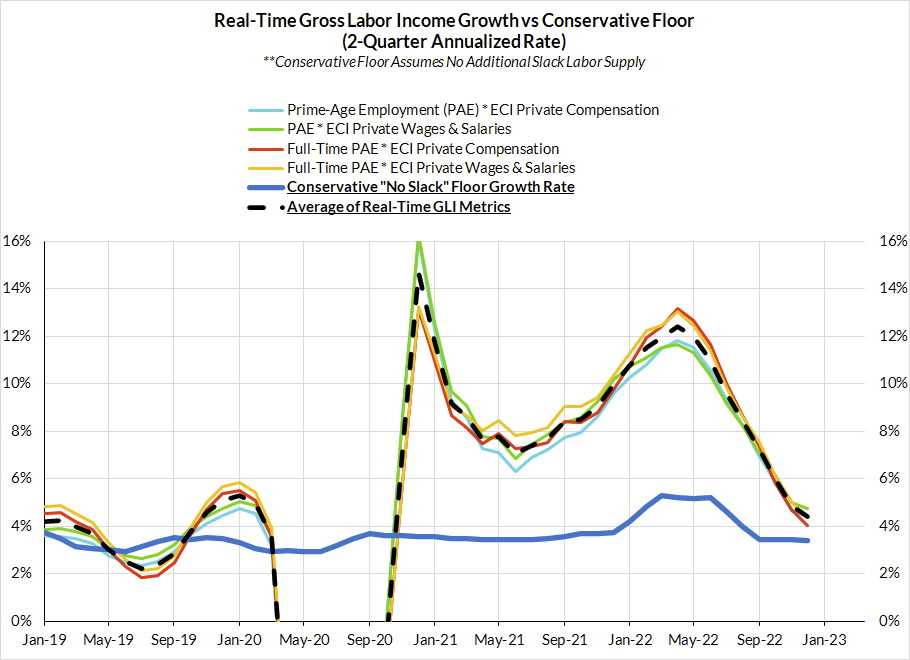

Taken together with the employment data, the combination of slowing employment and wage growth means that gross labor income is decelerating quickly and is essentially back to pre-2020 levels.

We’ve written before that the Fed’s effects on gross labor income are the primary channel through which the Fed affects inflation. The most cyclical components of inflation, such as rent and groceries, are not typically financed through borrowing, but through concurrent labor income.

There are other channels through which interest rates could affect consumption, such as affecting consumer borrowing rates and wealth effects. However, estimates of the elasticity of spending to interest rates are generally low, households do not behave purely according to the Euler Equation, and our understanding of the wealth effect channel is not well-understood. That being said, it does appear that higher interest rates are reducing demand in certain areas. Interest rate increases may stem demand for certain financed goods, such as new automobiles.

While a fall in consumption that stems directly from interest rate hikes could obviously have knock-on effects through raising unemployment, the point is that it is not the unemployment itself that tames inflation. The unemployment is an unfortunate side effect, but not one the Fed needs to directly aim at.

In addition to the above, there are other disinflationary dynamics that should come into play that are beyond the scope of Fed policy. As Alex Williams has pointed out, there are still substantial supply chain issues that will take time to work through the economy, and disinflation from resolving those issues will be a bumpy and lengthy process. Some believe that profit margins, which have increased during this inflationary episode, could ease, allowing the labor share of income to rebound as is historically consistent with post-recessionary dynamics.

The question for the Fed is: will they let these disinflationary dynamics play out? Or will they push ahead and risk unnecessarily eroding the strong labor market recovery they helped to achieve? Given the stakes, we hope they side with prudence and patience and aim for slower growth, not unemployment.