If you enjoy our content and would like to support our work, we make additional content available for our donors. If you’re interested in gaining access to our Premium Donor distribution, please feel free to reach out to us here for more information.

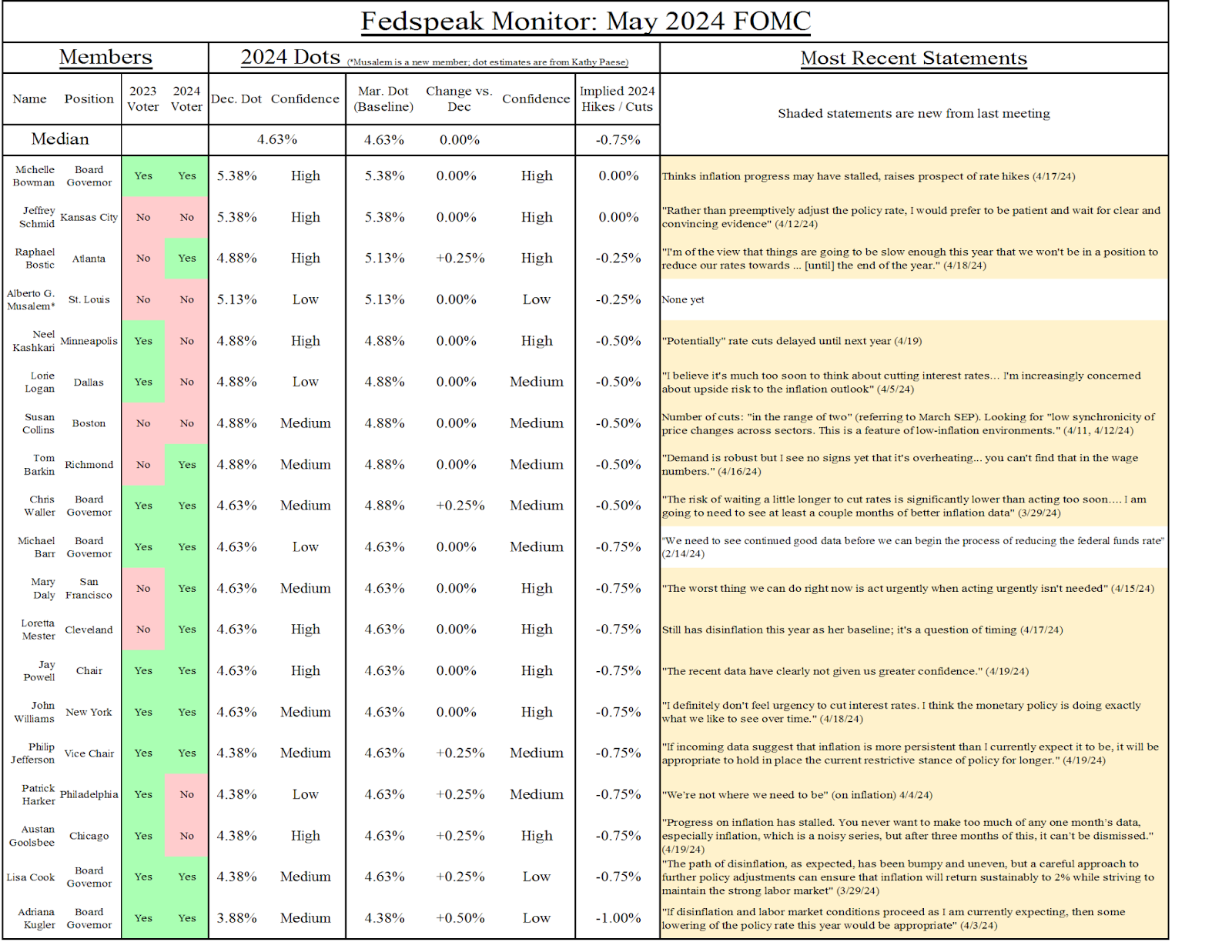

Latest Fedspeak and Dots

What to look for:

Since the last meeting, inflation has come in hot and the labor market has remained strong. The Fed will continue to hold off on rate cuts, and without an SEP this meeting what remains to be seen is how hawkish the statement and press conference will be.

Every member that's spoken since the March meeting has expressed both a further desire to be patient on starting rate cuts (in response to the inflation data) and confidence that holding rates steady for longer will, on the margin, come with less downside risk to the labor market. However, only a handful of members are talking seriously about the prospect of rate increases or cuts this year.

It's important to keep in mind that the continued pushback of the first cut is a reflection of the inflation data, rather than a change in the Fed's reaction function. Even as members stress the need for patience on cuts, they also have communicated that they are sensitive to the prospect of labor market deterioration. On the labor market side, their willingness to maintain rates at this level for longer reflects their belief that the labor market is more resilient than they previously believed, not a desire to see a greater deterioration in the labor market.

The Developments That Matter:

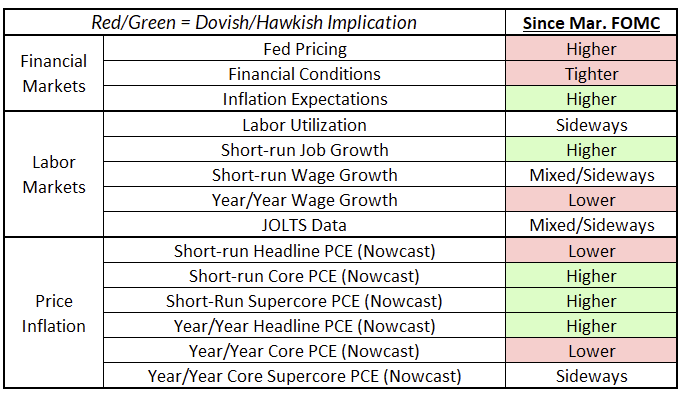

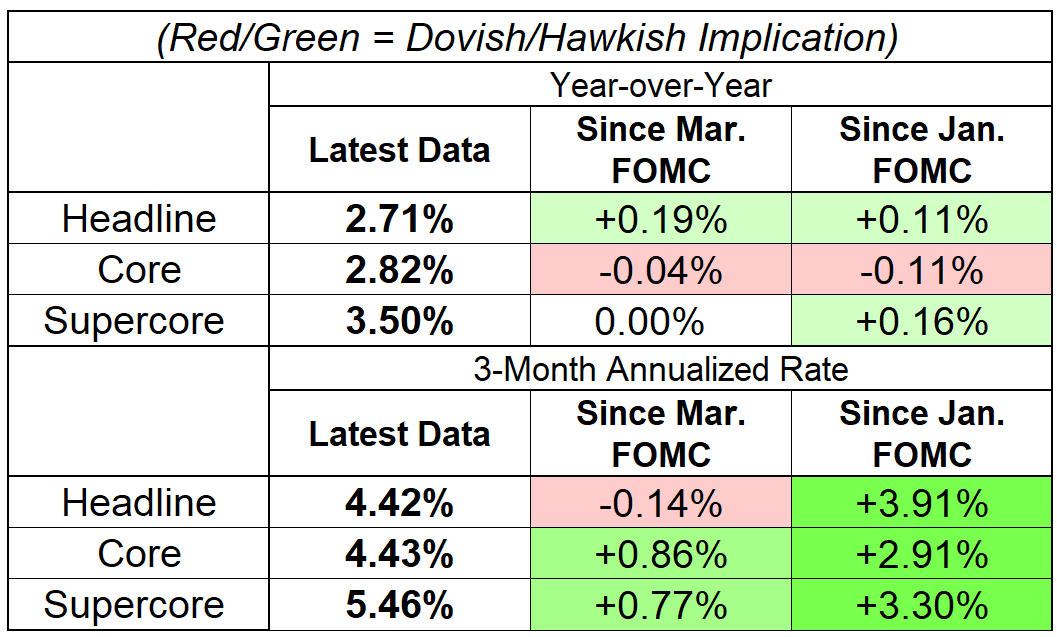

- Inflation: After a rough January and February, March was only slightly easier. Core PCE growth averaged 3.73% annualized in Q1 2024, and came in at 2.82% year-on-year in March. Core services ex-housing inflation moved sideways on a year-on-year basis, and continued to accelerate on a three-month basis. The most optimistic take you can find among the committee is Austan Goolsbee saying that progress has “stalled.” With three months of inflation prints higher than they’d like, they’re going to likely need at least three more months of good data before they feel comfortable cutting. Speaking on April 2nd (before we had information about March inflation), Mester (who is a 2024 voter and leans slightly more hawkish than the median FOMC member) said she would want to see two more months of good inflation data before cutting.

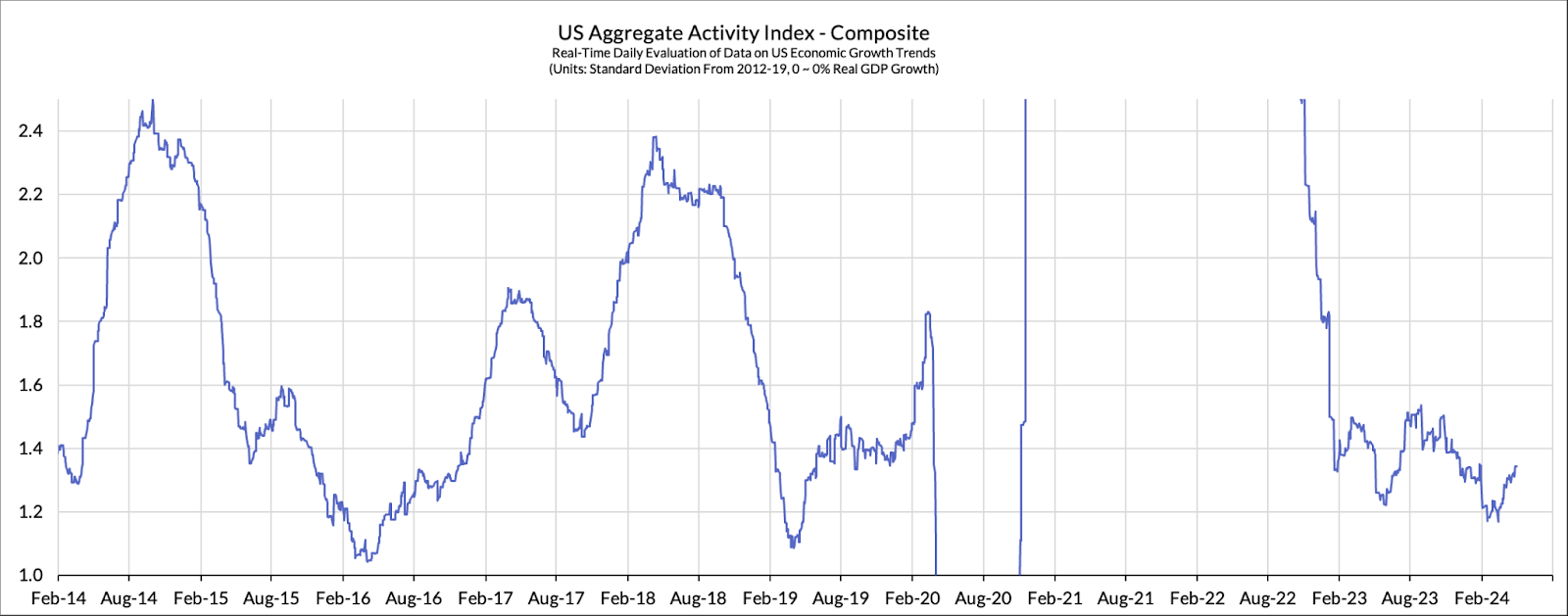

- The Labor Market Looks Resilient: There are no obvious signs of weakness in the labor market. The worst-looking series is the fall in full-time employment, but even that is not matched by an increase in the number of workers that are part-time for economic reasons. Nominal wage growth is running at or just above 4%, above what FOMC members think is compatible with 2% inflation (and members have been explicitly looking for slower wage growth from here.

- Fedspeak: Following this month’s inflation data, every member, from Michelle Bowman to Austan Goolsbee, has moved more hawkish. Our current baseline is for a September cut, with risk towards moving later. Some key statements from the more dovish members over the past few weeks:

Daly: "There's absolutely, in my mind, no urgency to adjust the policy rate"

Williams: “I definitely don't feel urgency to cut interest rates”

Goolsbee: “Progress on inflation has stalled”

That being said, members have generally stressed that their views represent a marginal change in the timing of cuts this year. A few members have talked about the prospect of no cuts (or even hikes) this year: Kashkari, Bowman, and Bostic. Bostic has signaled a willingness to do more cuts this year if there’s “pain” in the labor market.

There is a growing divergence among the committee about where r-star is. On one hand you have some members who think that the neutral rate has likely only risen slightly (this includes Daly, Williams and Goolsbee). These members appear to be more attentive to model-based estimates of r-star or explanations that rely on longer-term trends like demographics or productivity. On the other hand, members like Kashkari and Bostic lean more on the fact that growth and the labor market are strong as suggestive that policy is not that tight. Kashkari (3/6/24): “maybe this constellation is neutral…. So why do anything?”

What we’re thinking

Before the last FOMC meeting, we said that “what’s important is that they begin cutting as soon as they have that ‘bit more’ confidence.” That remains the case, and most of the committee appears to be ready to do that. Most importantly, the committee continues to say that they will cut in the case that the labor market shows signs of deterioration.

We also said that we see Fed restrictiveness in investment. That remains the case, and is one answer to members who are asking: “why cut?” As I’ve argued before, Fed effects on the supply-side could have ramifications on inflation in the longer-run. The prime example of this is in housing; multifamily starts fell to their lowest post-2020 level in March, and are now below levels seen in the mid-to-late 2010s. While the Fed might be constraining rental inflation currently, we might be seeing the start of another round of housing shortages that may come back to hit rental inflation in the future.

The impact on investment is also an answer to members who are entertaining the idea that rates are currently neutral. Consumption might be strong (buoyed by the strong labor market and the latent effects of supportive fiscal policy) but if Fed restrictiveness is primarily felt in investment—what does that mean for the Fed’s goal of reducing core PCE inflation?

How Has The Data Evolved Since Last FOMC?