Welcome to our State Space series. Here you will find how we’re thinking about the pathways and scenarios that could take us to critical economic states. We will never settle for "it's too unlikely." We try to reason backwards from the most important (tail-risk) scenarios, their most likely pathway to fruition, and the indicators that allow us to monitor the likelihood of each pathway. Updates will share how these pathways are (or are not) playing out, and if new risk scenarios are potentially emerging. If you are interested in more timely and extensive access to this content, feel free to reach out to us here.

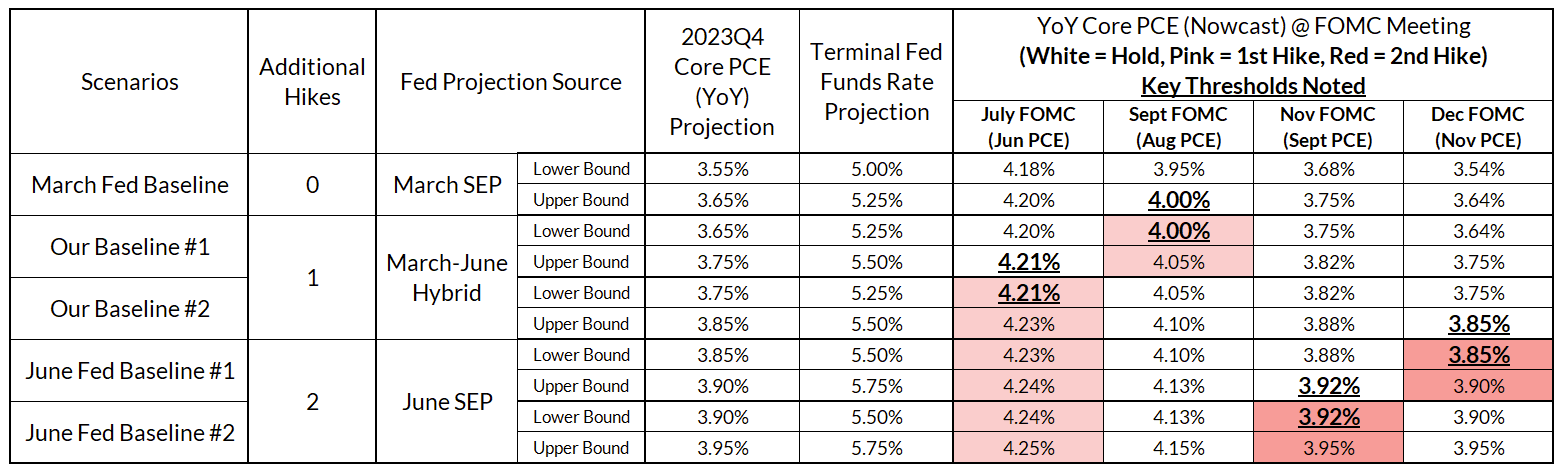

In this post, we lay out the roadmap for understanding how Core PCE outcomes could shape Fed meeting decisions through the rest of the year. We also provide a comprehensive update of our baseline views.

The major shifts from the baseline outlook in the previous edition of our State Space series:

- Recession probabilities have abated further as a result of more accommodative financial conditions and more sustained momentum in fixed investment. Nominal growth readings are decelerating, while real growth readings are potentially accelerating.

- We now see one additional hike (terminal 5.375%) as the firm base-case. We were previously on-the-fence prior to the June FOMC meeting about whether 5.125% or 5.375% would be the terminal Fed Funds Rate (and leaned towards the former).

- A July hike is now a strong base case, with risks skewed towards a second additional hike in 2023 (vs not hiking at all). That said, we can paint realistic scenarios in which 0, 1 and 2 additional hikes are very plausible. In this post, we lay out the roadmap to each of these scenarios in terms of Core PCE outcomes and provide a comprehensive update of our baseline views.

The full version of this State Space is made available exclusively for our Premium Donors. To view the full version, sign up here for a 30-day free trial or contact us for more information.