June 2026 FOMC Preview (Public)

We don’t expect a hiking bias to be explicit in the June statement or the press conference, but we expect it to start to show in the Fed dots.

We don’t expect a hiking bias to be explicit in the June statement or the press conference, but we expect it to start to show in the Fed dots.

Note: Subscribers to MacroSuite receive our FOMC preview during the blackout period before each FOMC meeting. A public version of the preview is released closer to the meeting. If you're interested in becoming a MacroSuite subscriber, please reach out to macrosuite@employamerica.org

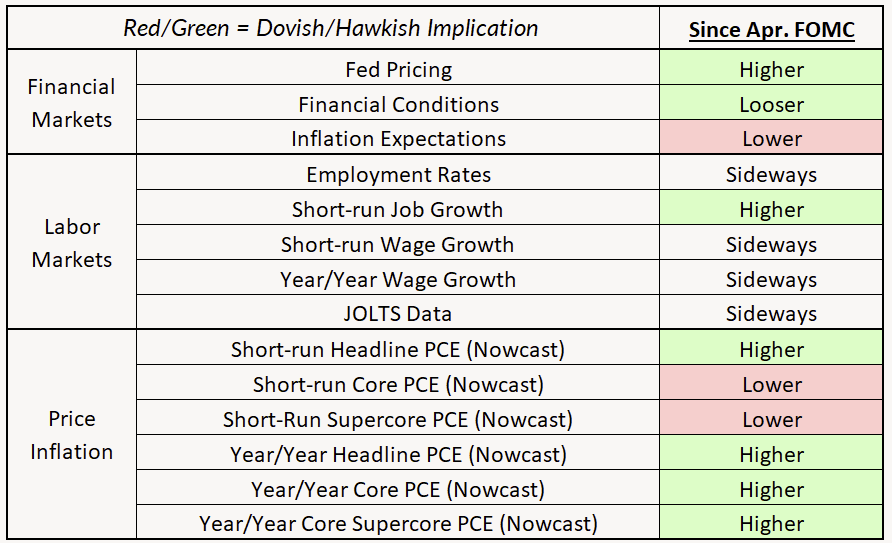

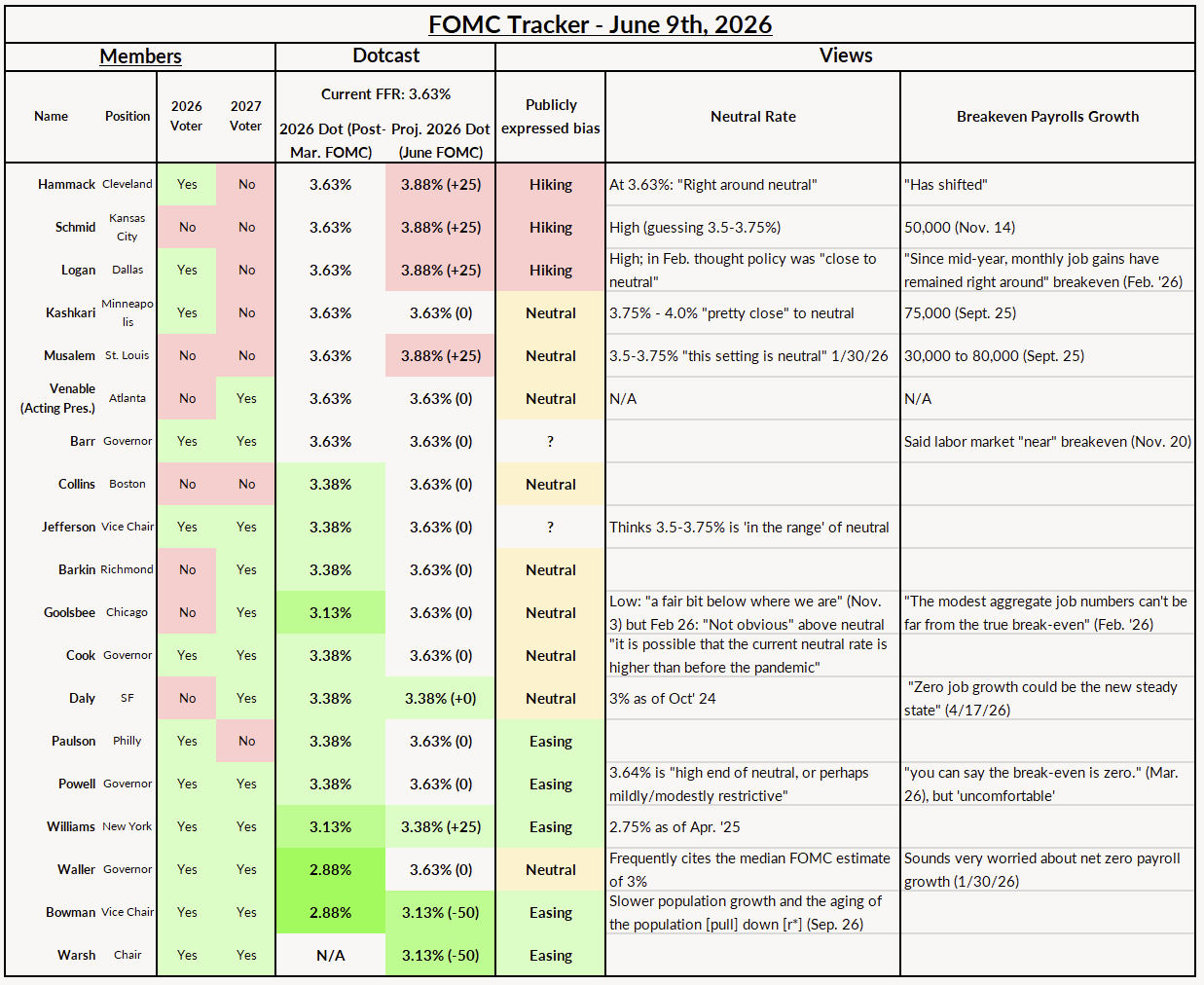

The data developments, Fedspeak, and market action since the previous meeting could not be worse for a new Fed Chair that wants rate cuts. Since the last meeting, the inflation outlook has worsened, and the labor market data has looked pretty solid. The Committee has taken notice; members with a cutting bias are now neutral, and neutral members have adopted a hiking bias. We are seeing the hawkish pivot we predicted play out.

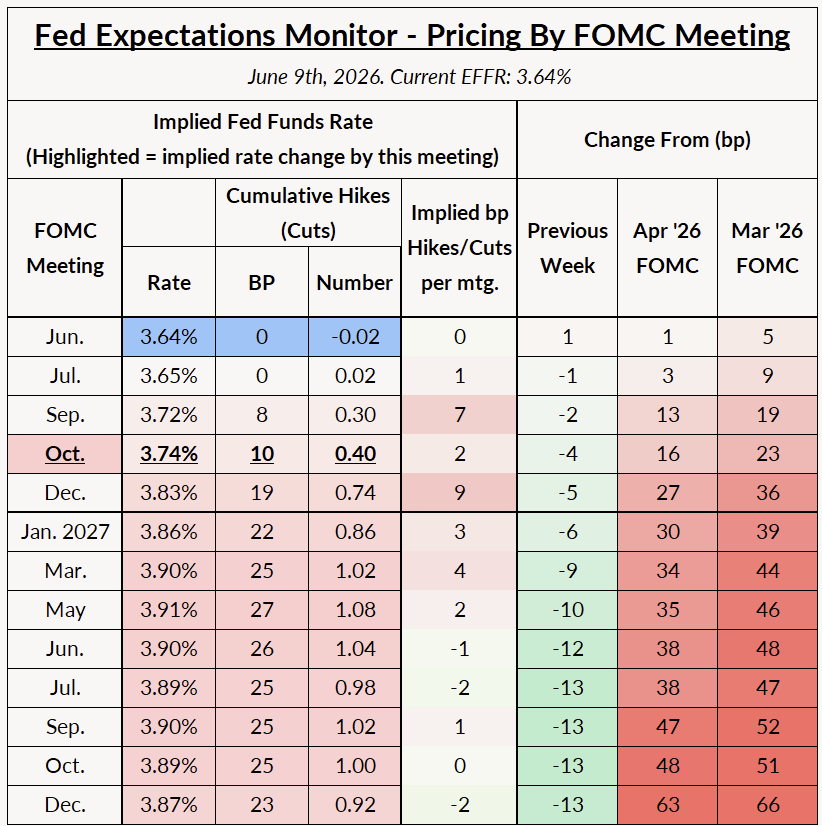

One big question we are looking for is: how soon will the hawkish pivot pencil itself in? We don’t expect a hiking bias to be explicit in the June statement or the press conference, but we expect it to start to show in the Fed dots. We expect a more overt hiking bias to reveal itself in the Fedspeak over the next few months, and our base case is for a hike as soon as October with two hikes overall.

Warsh has come into the position of Fed Chair arguing that trimmed mean measures of inflation and the prospect of deflationary productivity growth mean that the Fed should be cutting rates even as the risks tilt away from the labor market and towards inflation. Those arguments have been widely panned by other Committee members. Regional Bank Presidents at branches that create trimmed mean measures have noted the flaws with asymmetric trimmed mean measures, and the members that show the most interest in productivity growth are leaning towards productivity growth leading to higher neutral rates.

If Kevin Warsh tries to push for imminent rate cuts, he will be far outside the central tendency of the Committee, finding few other allies on the Committee. There is a lot of uncertainty in how he will play this, but the view from the rest of the Committee is clear: cuts are off the table for now, and hikes may be coming.

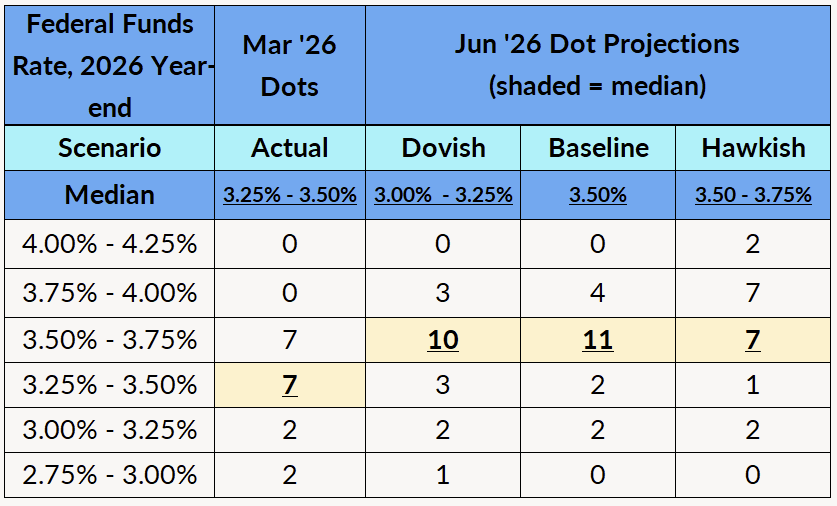

Our baseline scenario sees most of the Committee at no hikes or cuts for the year, with four hawks putting in a hike (probably Hammack, Musalem, Logan, Schmid). We have Williams, Daly, Bowman and Warsh still penciling in at least one hike for the year.

We do not see much scope for dovish movements from that scenario, but see much scope for potential hawkish deviations from our baseline. We still do not know how Fed officials have digested that jobs report, and it’s possible that the hawks will feel emboldened enough that a couple of them pencil in two hikes and significantly more members move to a hawkish bias. Here, the median dot is still for no cuts or hikes, but only just barely.

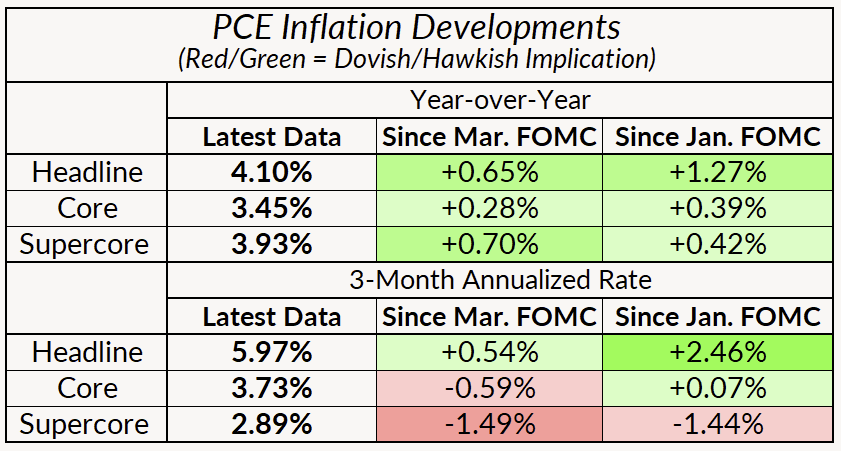

Inflation continues to be a headache for the Fed, with core PCE coming in at 3.3%. The causes are not uniform, with tariffs, AI investment, and the closure of the Strait of Hormuz all playing a role. While Warsh’s favored Dallas trimmed median measure is declining, our more robust symmetric trimmed mean measures are rising and closer to 3%. May CPI and PPI may show somewhat lower short-term inflation, but it likely won’t be enough for the Committee, which put forward a median projection of just 2.7% PCE and core PCE inflation in 2026.

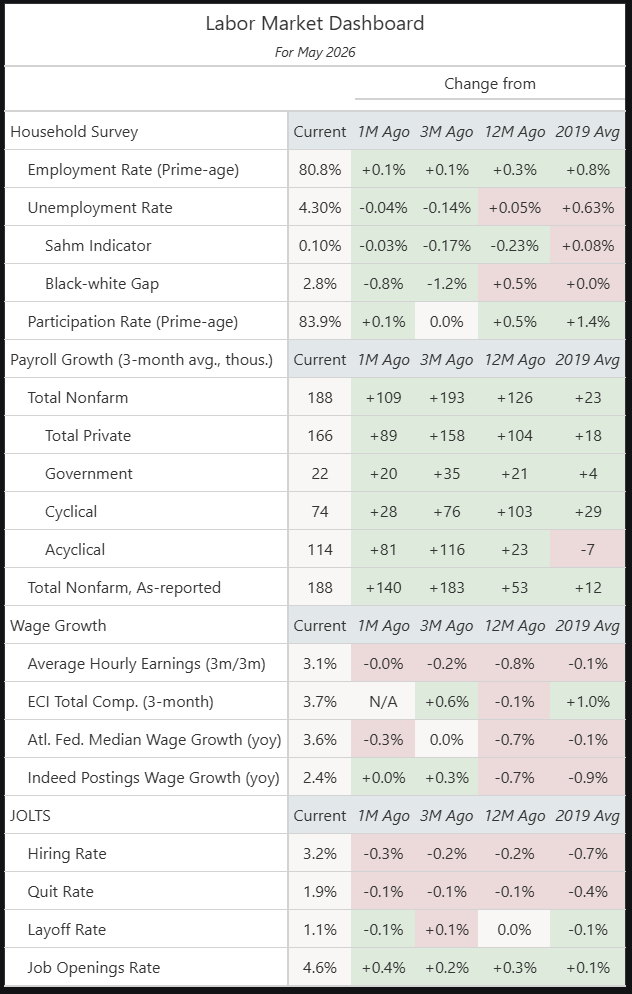

Meanwhile, the labor market looks somewhere between stable and even potentially accelerating. The unemployment rate in May was about where it was prior to the April meeting, and nonfarm payrolls had another good month. Payroll growth has now averaged 188,000 a month for the last three months, far above the zero breakeven rate that many FOMC members believed was plausible. While earlier jobs reports this year were clouded by weather, strikes, and weird seasonality issues with the birth-death model, the most recent jobs reports have been relatively clean.

The Fedspeak has quickly shifted hawkish over the past few weeks. Prior to the April meeting, even the most hawkish members of the Committee were only expressing a neutral bias when it came to future policy. Now, we are hearing more explicit hiking biases from that side of the Committee. Meanwhile, more dovish members have shifted over to neutral, including key voting members that Warsh would be relying on to deliver cuts. And all of that hawkish Fedspeak came before the strong jobs report from last week, which came out right before the blackout period.

We also heard from members on their thoughts on productivity-backed disinflation. Most members don't put a lot of weight on the probability that productivity growth will allow for rate cuts—a key argument that Warsh is leaning on.

Hammack: "if recent trends continue, it may soon be appropriate to act"

Schmid: "Is it temporary...or do we act? Do we say, okay, now it’s time to raise rates a quarter or two and see if we can’t tamp this thing down?"

Logan: "These conditions indicate that monetary policy is not restraining the economy. I am increasingly concerned that higher interest rates could be necessary later this year"

Daly: "We are prepared to respond either way, whatever the economy brings"

Cook: "I am prepared to raise rates, if the expected disinflation does not appear in a timely manner."

Musalem: "If we don't see disinflation in the next one to two quarters, that would concern me"

Goolsbee: "The bigger the hype about future productivity, the more rates may need to rise to prevent overheating"

Williams: “an increase in trend productivity growth raises real interest rates in the long run.”