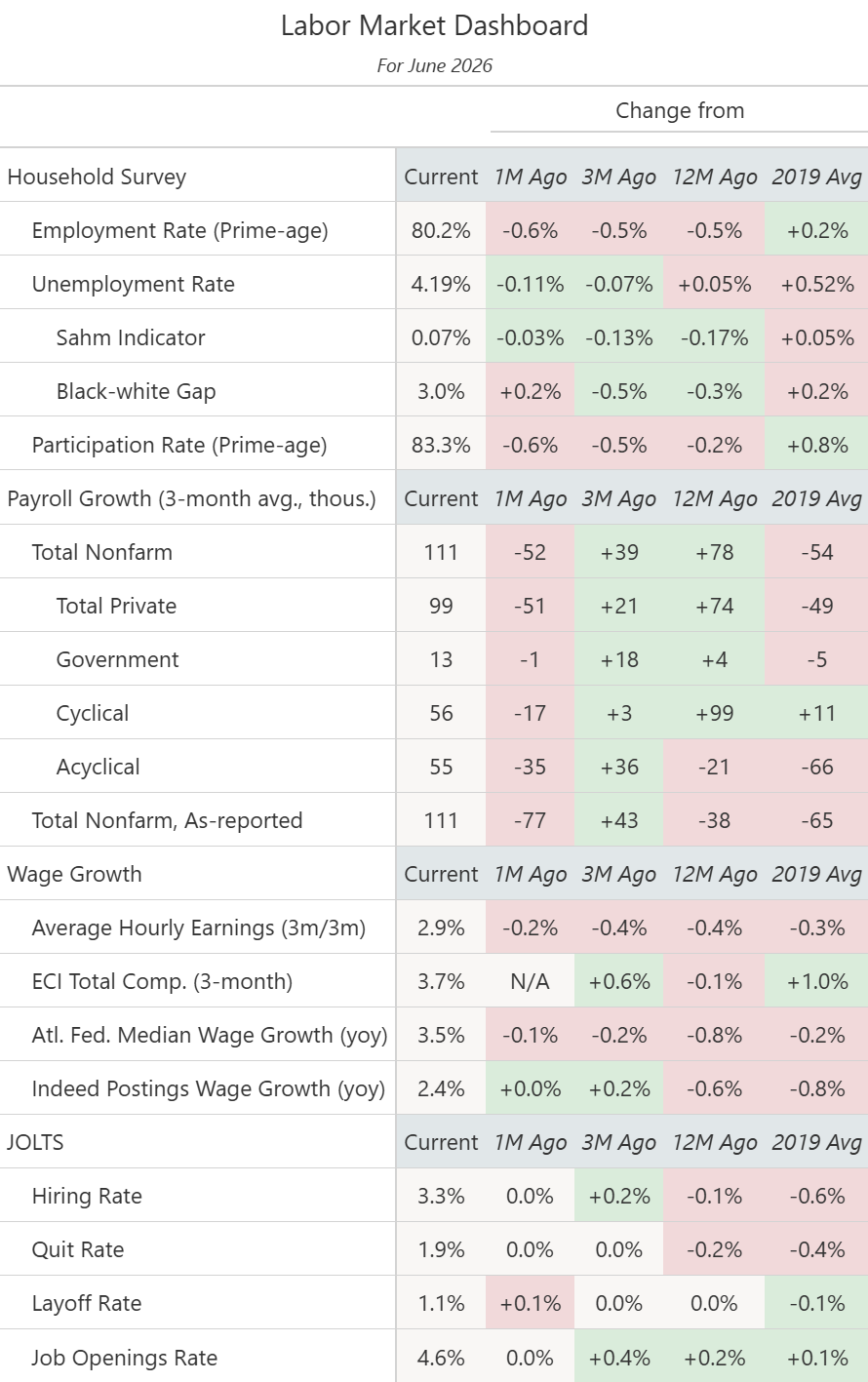

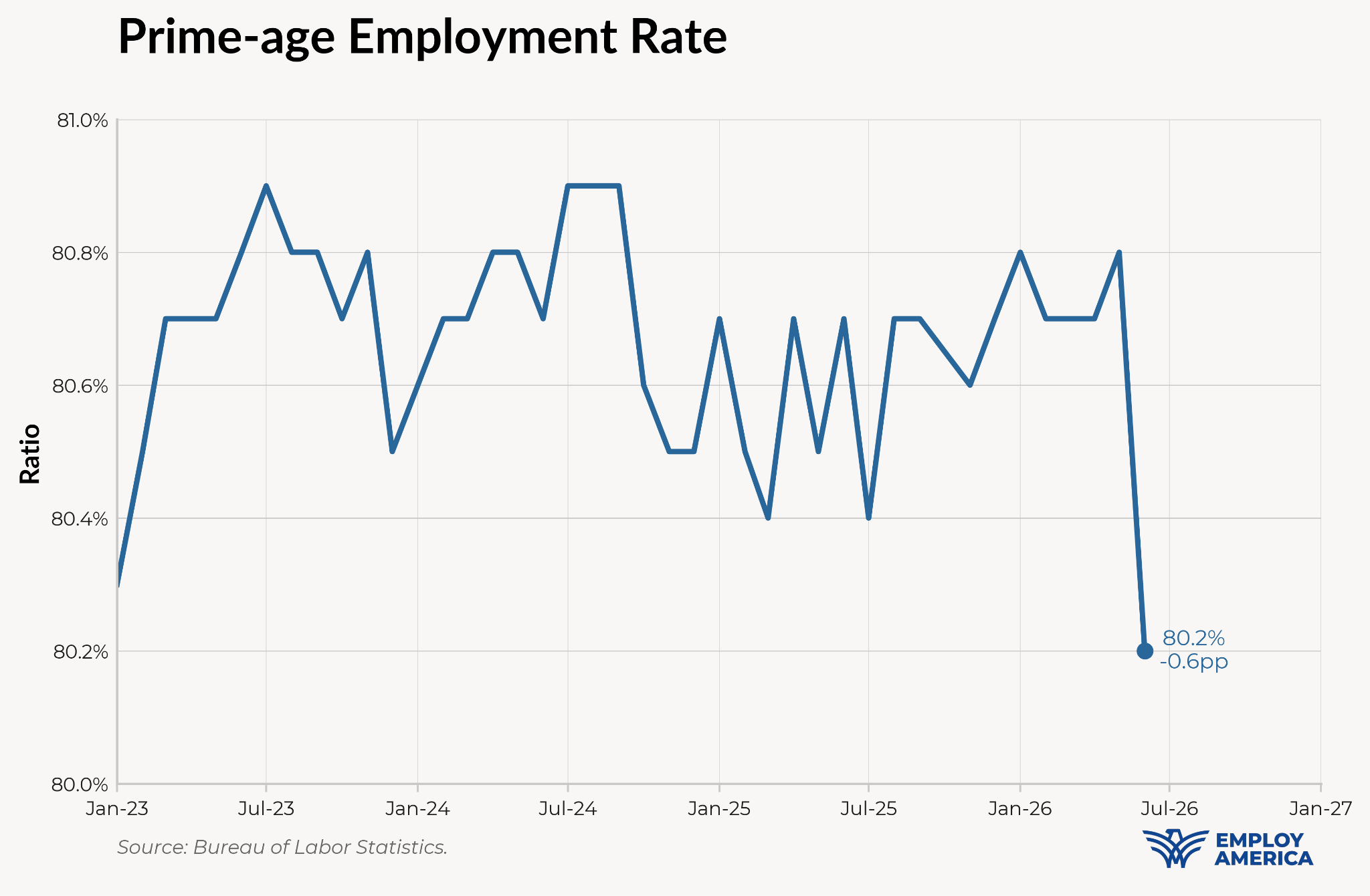

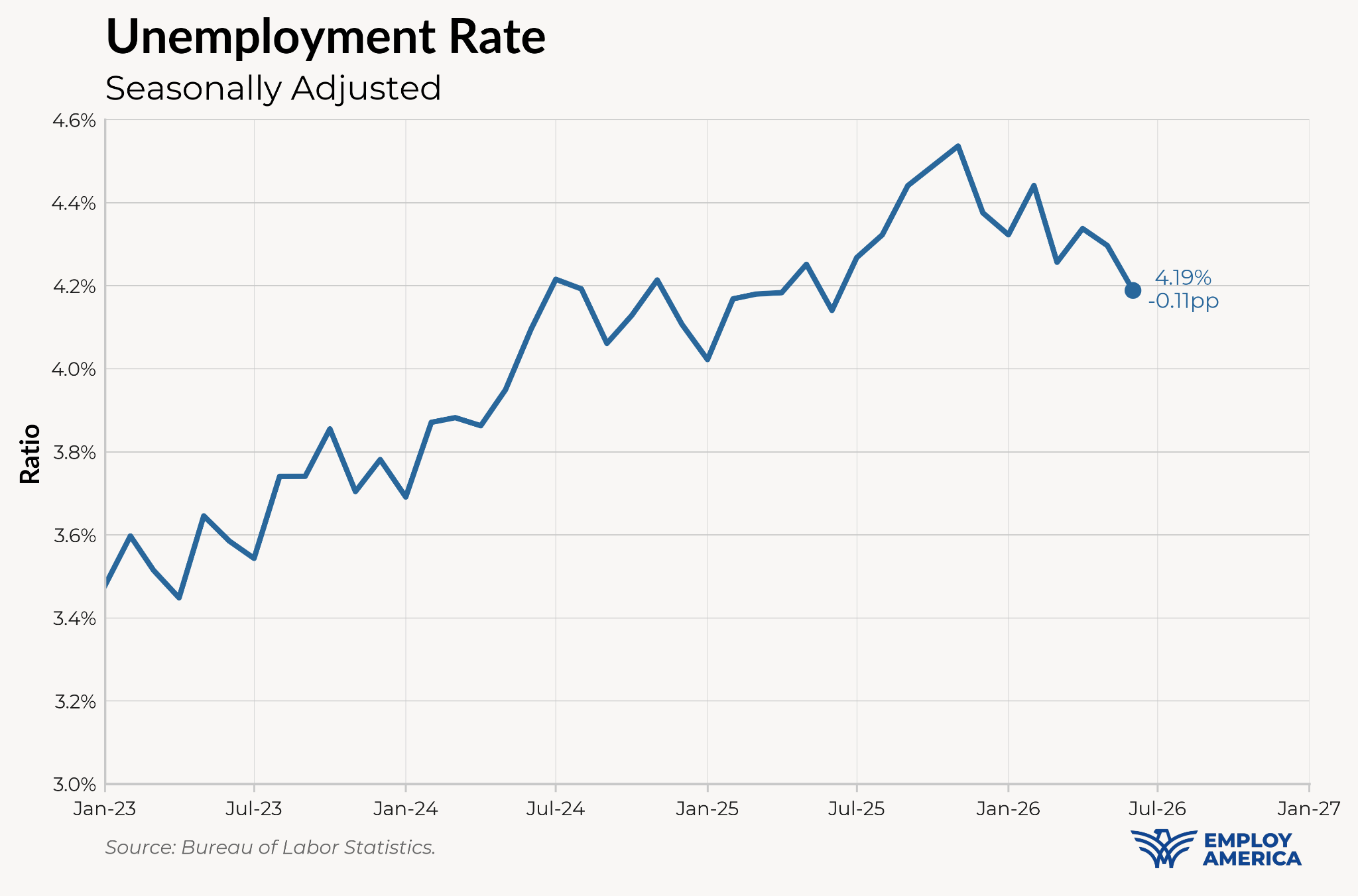

The prime-age employment rate fell by 0.6pp in June, its fourth largest drop in the 21st century. At the same time, the unemployment rate fell by 0.11pp and non-farm payrolls added 57,000 jobs, albeit with sizable downwards revisions to previous months. This is one of the strangest reports we have seen in a while, with no obvious explanation. The household survey response rate, at 66.2%, was not abnormal relative to recent months, but response rates have been trending down for the CPS.

As a whole, this report takes away some of the strength of the labor market we saw over the past couple of months. Things are not as dire as the drop in the prime-age employment rate would signal alone, but the case for a labor market acceleration is weaker. That uncertainty over the labor market shaves off some of the probability of an early Fed rate hike at the July or September meetings as the Committee awaits more data.

Source: Bureau of Labor Statistics, Author’s Calculations. Red indicates weaker labor market development; green indicates stronger.

Stripped of any context, a 0.6pp drop in the unemployment rate is disastrous. Outside of June 2009, March 2020, and April 2020, the labor market has never seen a drop in prime-age employment of this scale.

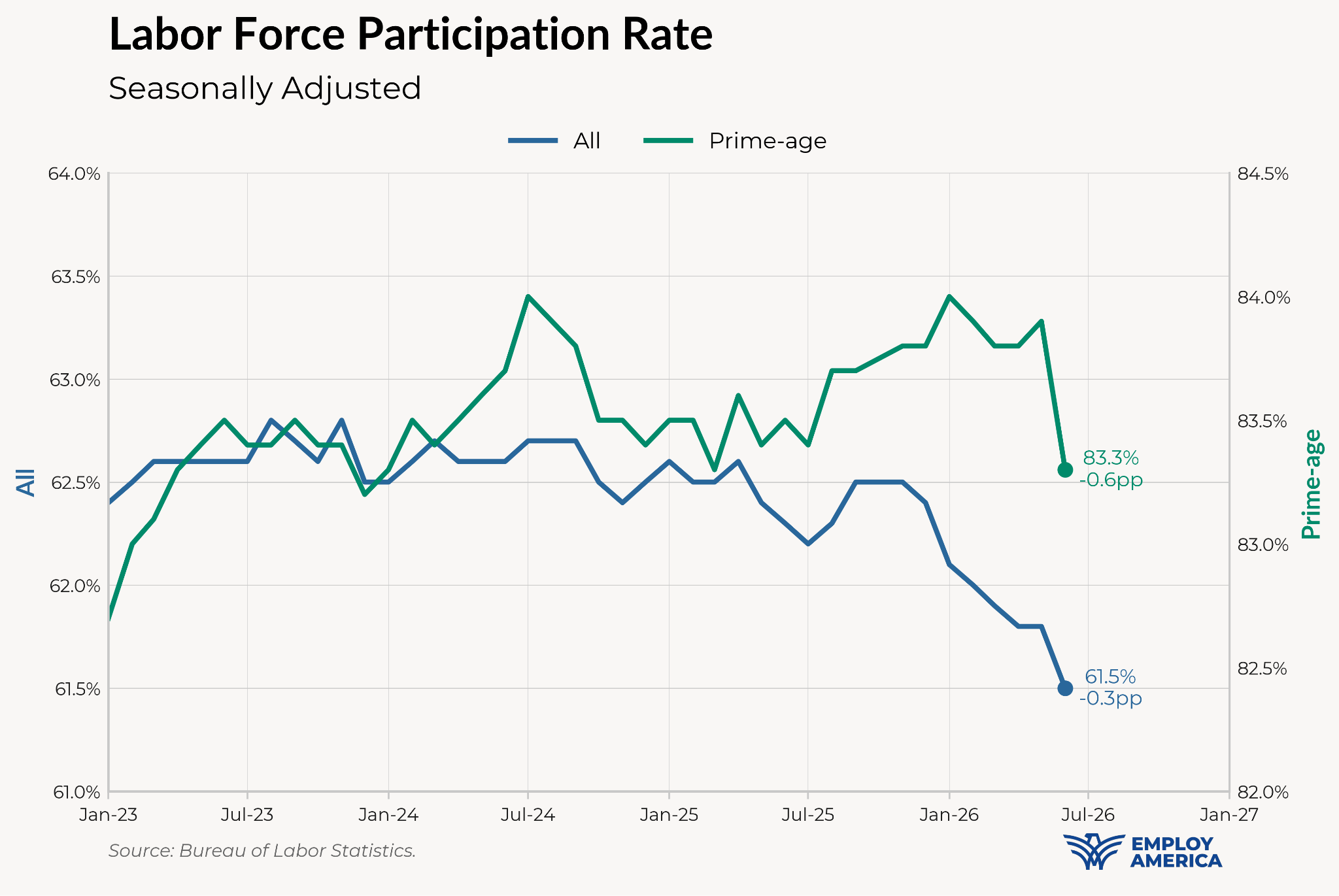

But those other drops in employment rates were accompanied by steep increases in unemployment. Instead, we saw a decline in the unemployment rate, paired with a steep decline in labor force participation.

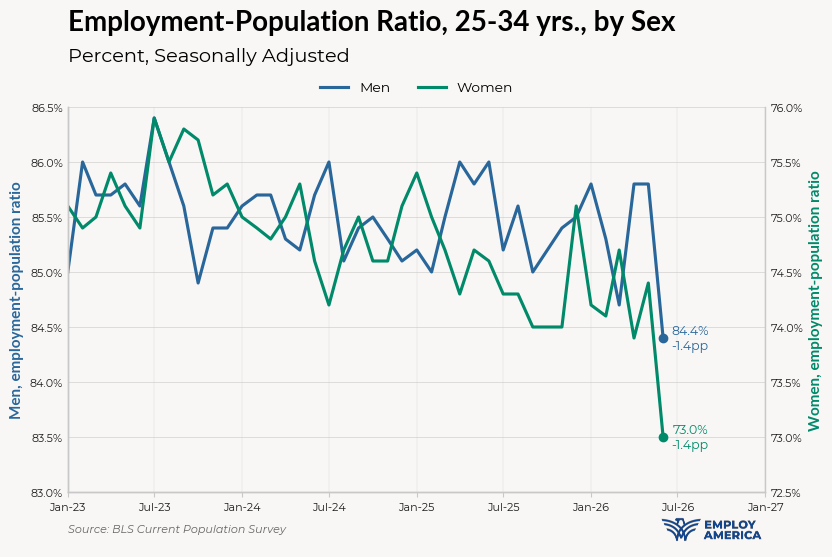

The decline in the prime-age employment-population rate is overwhelmingly attributable to declines in employment and participation in the 25-34 age category. Here, employment fell amongst both men and women. Declines were strongest amongst the hispanic and latino population, but employment also fell significantly among 25-34 white workers as well.

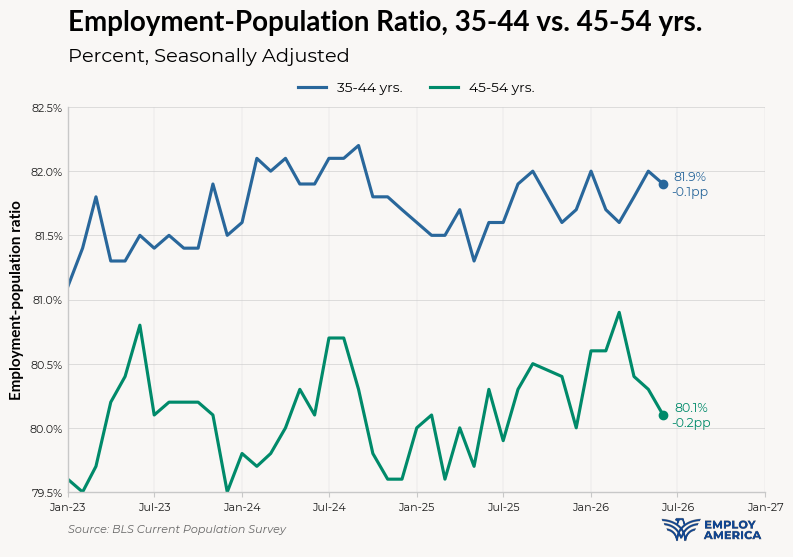

Looking elsewhere in the prime-age cohort, employment rates fell by 0.1pp and 0.2pp in the 35-44 and 45-54 age groups. These declines are well within the normal range of month-to-month variation.

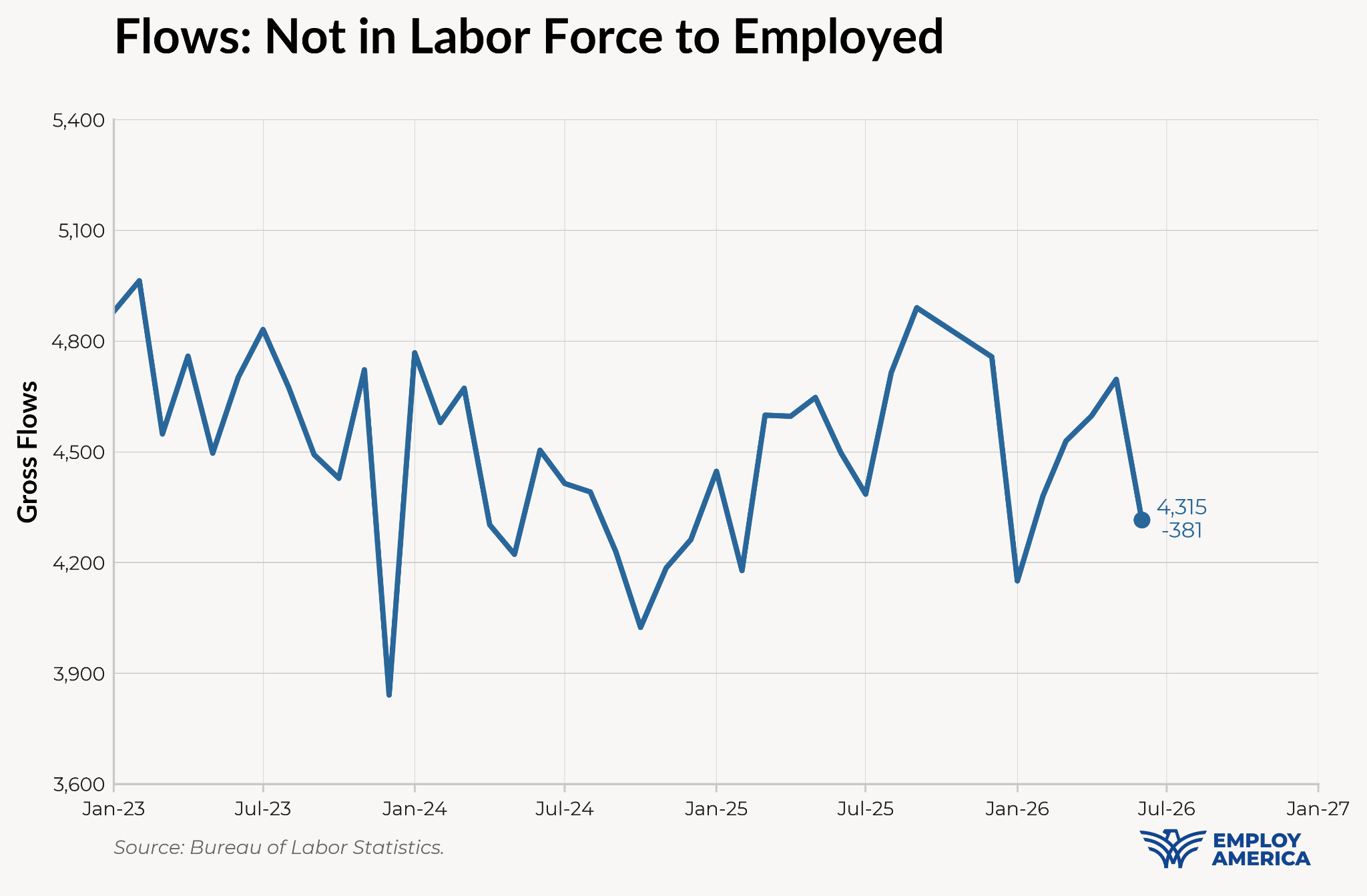

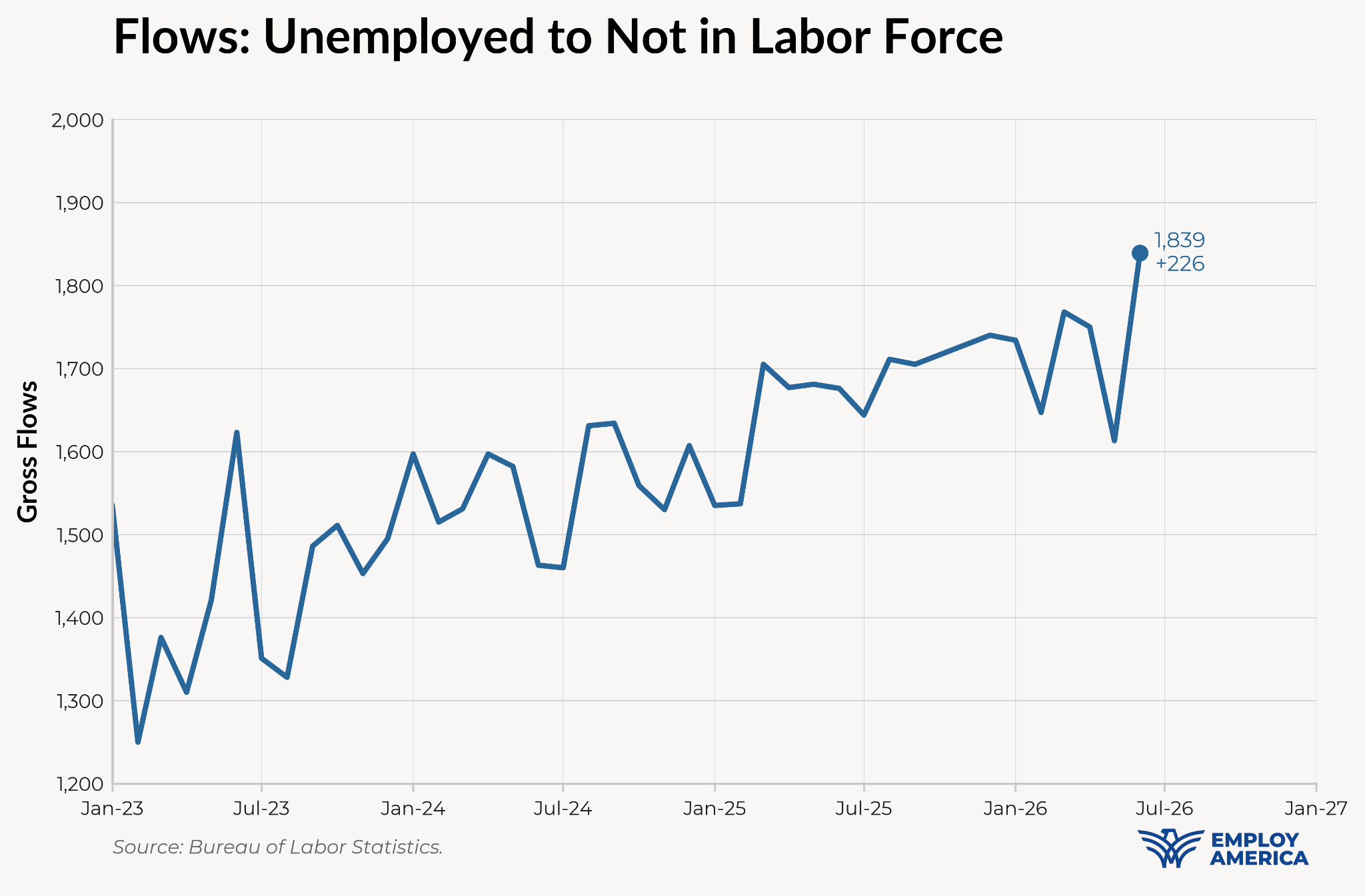

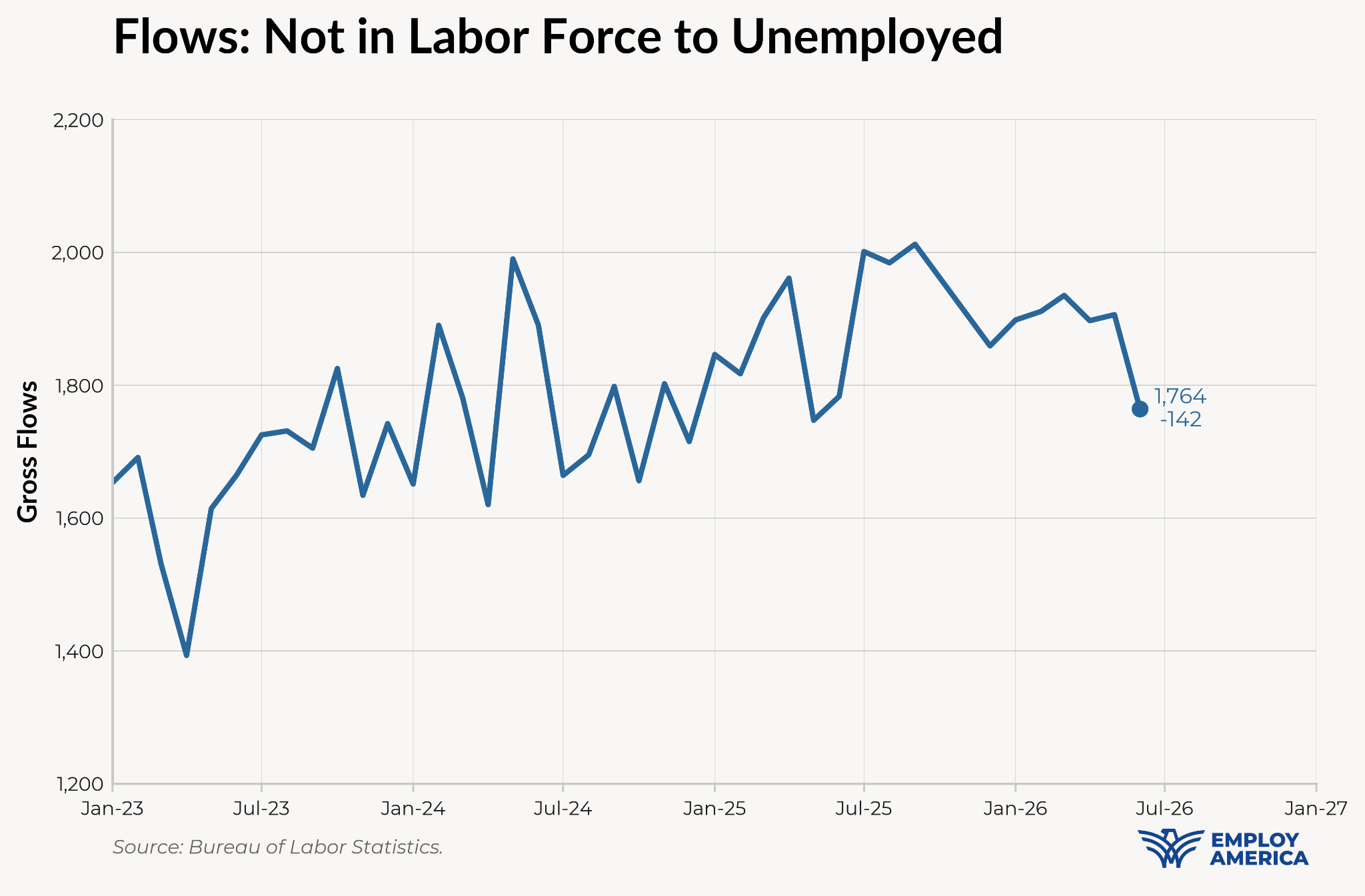

There isn’t a smoking gun for the decline in employment and participation amongst 25-34 year olds. If we squint at the gross flows data (which aren’t broken out by age), we see a decline in people entering the labor force, and an increase in unemployed persons leaving the labor force.

While the number of employed that left the labor force was up, the increase was small (+128,000) relative to the drop in nonparticipants that found jobs (-381,000). In short, the decline in participation and employment is probably more due to fewer nonparticipants finding jobs and less due to employed persons quitting their jobs.

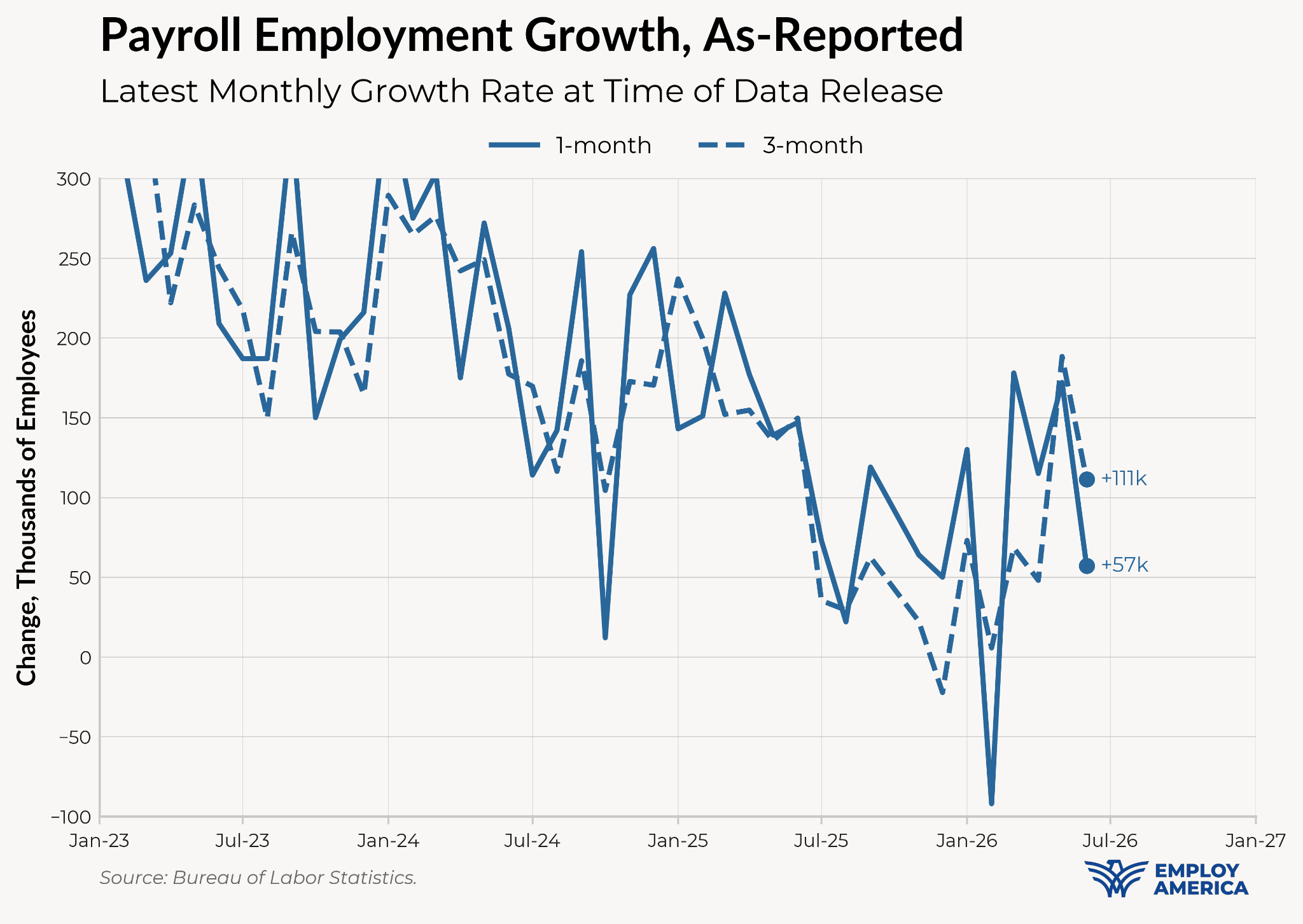

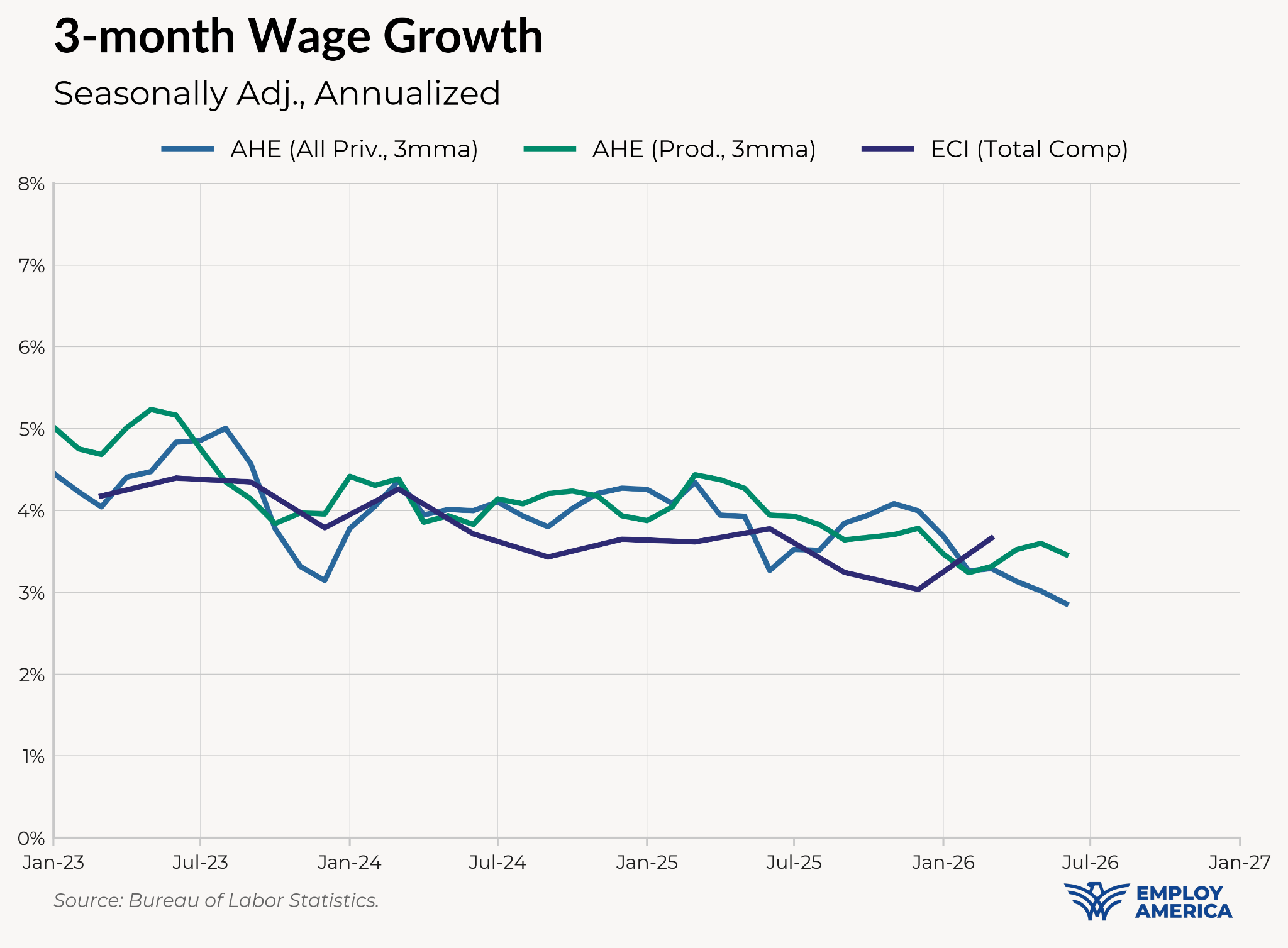

Turning to payrolls, the increase in 57,000 jobs is comfortably above the 0 job growth breakeven that some Fed officials surmised might be the case late last year. Still, the decline in job growth alongside a continued decline in wage growth reduces some of the confidence we have in a labor market reacceleration.

Less Confidence in the Labor Market Shades the Chances of an Imminent Rate Hike

This is a noisy labor market report, and it’s hard to say with any confidence exactly what it means. The decline in employment amongst 25-34 year olds is too large to dismiss, but the lack of breadth of the decline amongst other age groups is too odd for us to take it as a broad signal of labor market deterioration. Looking more broadly, we do see smaller declines in employment amongst other prime-age groups, and there is some more softness in the payroll data (including negative revisions) and wage growth data.

With inflation above target and lower confidence in the labor market, the tradeoff for the Fed is going to get harder. This labor market report will provide confirmation for the likes of Williams and Waller, who have been arguing for a hold rather than a hike. Some of the more marginally hawkish members may be willing to push back their timeline for rate hikes as they await further clarification on how the labor market is trending.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.