There's a great deal of literature on the connection between tighter credit conditions, economic activity, hiring, and inflation. Very large body of literature. The question is, how significant will this credit tightening be and how sustainable it will be.

Jerome Powell, March 22, 2023 FOMC Press Conference

In the wake of the SVB failure, we argued that the Federal Reserve should be specific about how the tightening of financial conditions trickles down into economic activity, unemployment, and inflation. Intended or not, the failure of SVB itself is a manifestation of (among many other things) the Federal Reserve’s interest rate policy. At the FOMC press conference last week, Powell himself said of the tightening financial conditions after SVB, “we're thinking about that as effectively doing the same thing that rate hikes do. So, in a way, that substitutes for rate hikes.”

How might this episode of financial turmoil pass through to the real economy? At this point, little is certain. For now, the risk of bank runs appears to be contained to the very particular business model that SVB was engaged in, but the impact on lending behavior has yet to be determined. With that in mind, the Fed should be watching for more granular signs that its interest rate policies are showing up in the real economy. The history of financial crises suggests that the effects on Main Street are not felt evenly and linearly; rather, the particular relationships that banks and firms have matters for where we might see things play out.

Relationship Banking Matters

As Powell alluded to at last week’s FOMC press conference, there is a large literature about the connections between credit conditions and economic activity. An important subset of that literature examines the effects of declining credit supply to firms arising from shocks to specific banks. When the supply of credit from one particular bank declines, firms connected to that bank often can’t cleanly substitute by going to a different bank. Bank-firm relationships are frictional, and the ramifications of a pull-back in lending at specific banks will depend on the industries and types of firms that the particular bank works with.

Chodorow-Reich (2014) examines banking relationships during the Global Financial Crisis and finds that firms that had pre-crisis relationships with lenders that reduced their lending by more were less likely to obtain a loan, paid higher interest rates, and decreased their employment by more than firms that had relationships with healthier lenders. This effect was stronger at small- and medium-sized firms. Amiti and Weinstein (2018) use matched bank-firm lending data from Japan to show that idiosyncratic reductions in bank lending negatively affect investment at the firms those banks lend to. Numerous other studies confirm the same result: relationship lending matters.

In light of this phenomenon, where specifically might the fallout from the SVB events be felt in the labor market? Since the fall of SVB, deposits at small banks dropped sharply. While it is still too early to say for certain how this will continue to play out, it is worth thinking about where stresses in financial markets may show up in the real economy if we see a pullback in lending from small and regional banks. As is well-known, small and regional banks are disproportionately involved in commercial real estate lending. Small banks also have an important role to play in lending to small businesses; while business credit card lending is dominated by larger banks, small banks have an outsized role in making loans over $100,000 to small businesses.

Employment at small businesses and in sectors reliant on commercial real estate, which not only include construction but parts of professional business services related to offices and retail fronts.

The Labor Market in these Areas is Already Under Stress

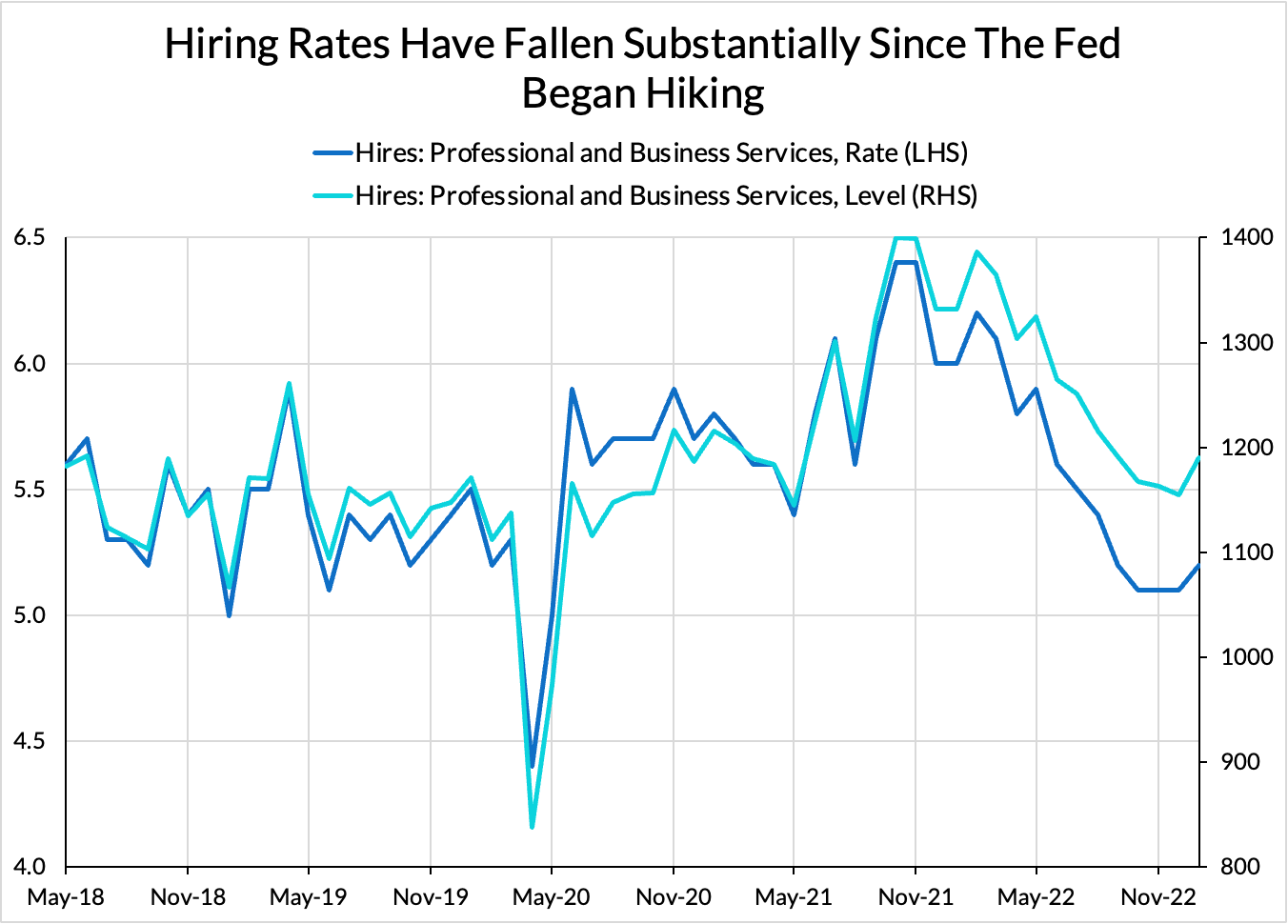

The evidence for a softer labor market within Professional and Business Services in the JOLTS data is strongly suggestive. Hires are down, but down from historic peaks. Notably, the hiring rate has slowed faster than the hiring level, as smaller numbers of hires are being divided into a larger employment base.

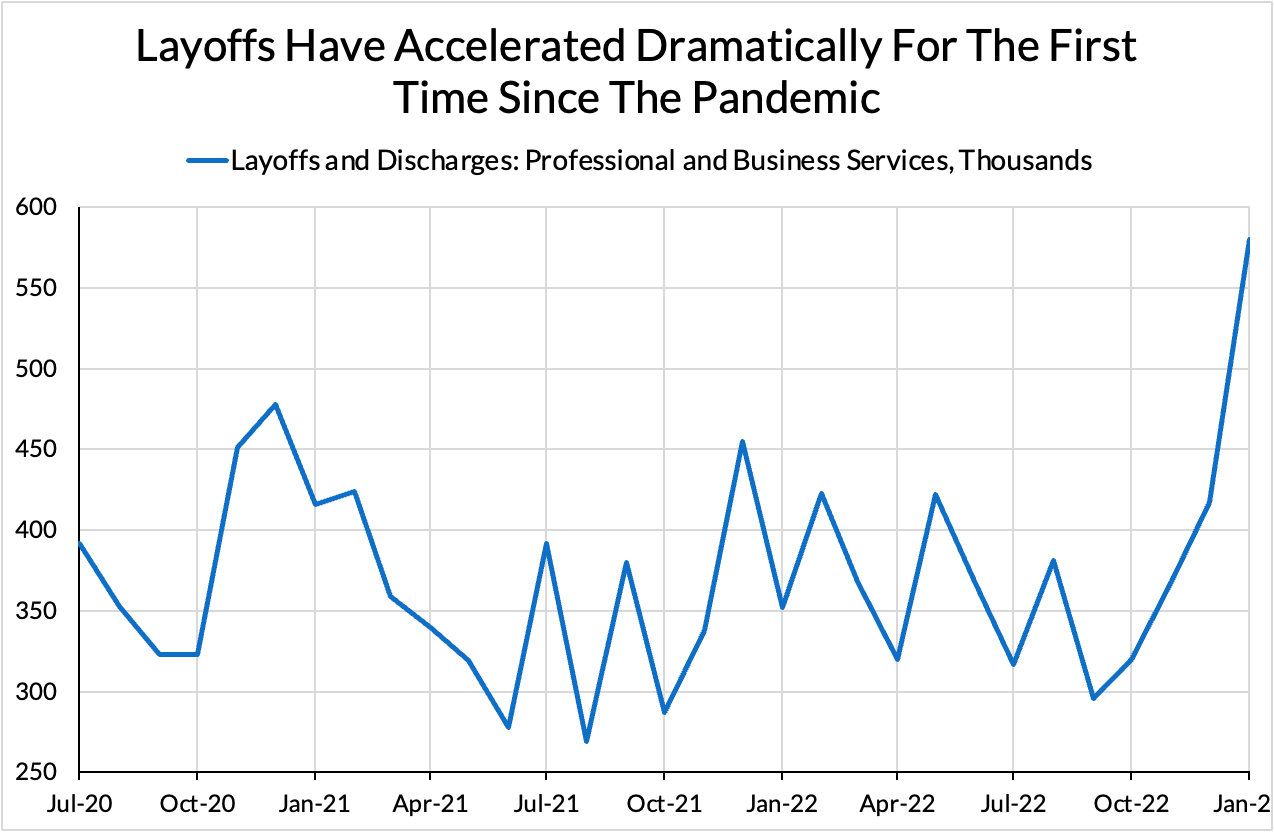

Layoffs are up so far this year, but some of this may be from the very highly publicized tech sector layoffs.

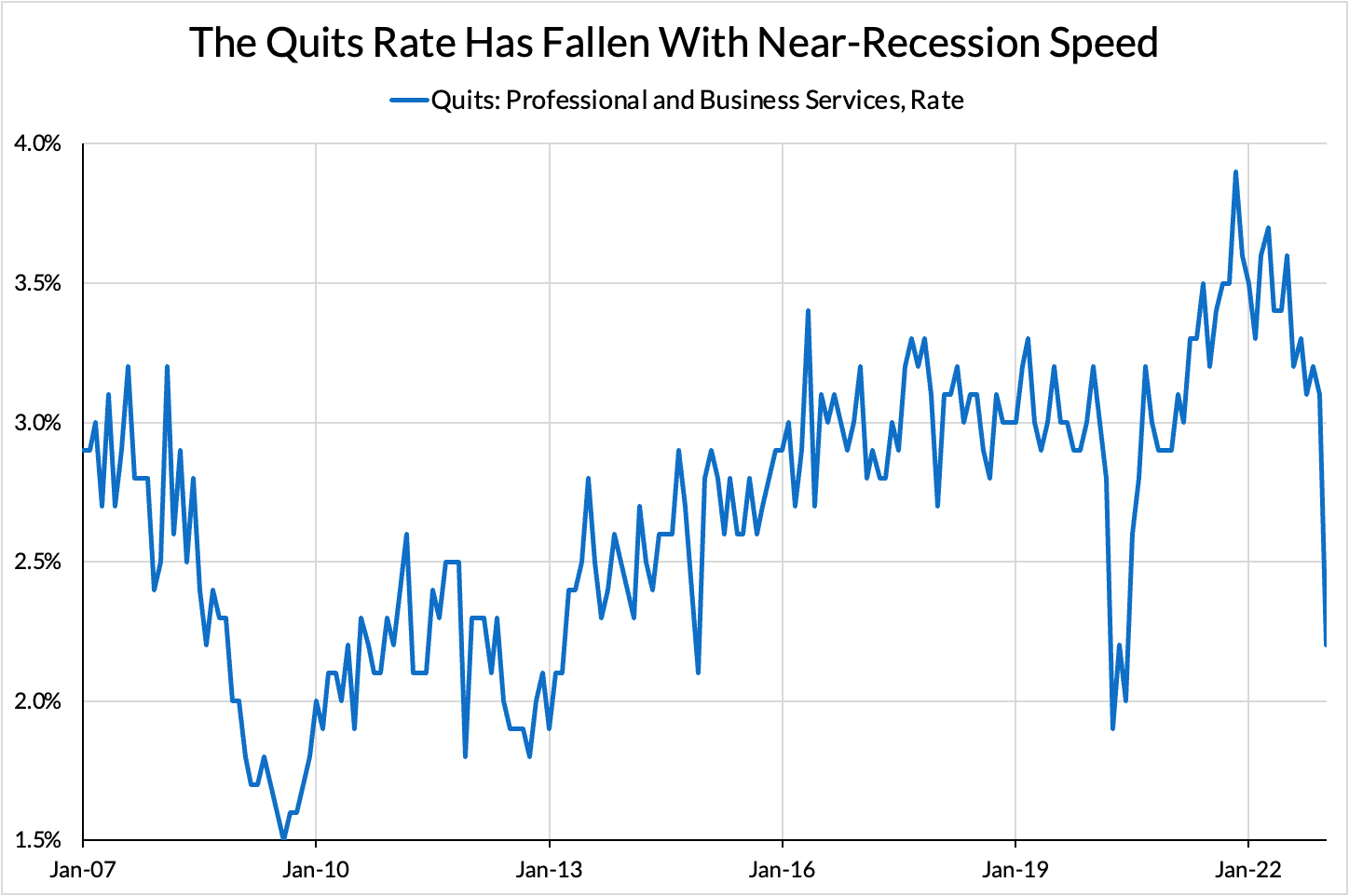

Most interestingly, quits appear to have fallen very dramatically, suggesting that workers may be feeling the chill in hiring or have become more sensitive to the risk of recession.

It’s also important to bear in mind that these data points are still preliminary and subject to revisions. Potential differences in the calculation of seasonal effects following the pandemic disruption add a second potential grain of salt to take this data with.

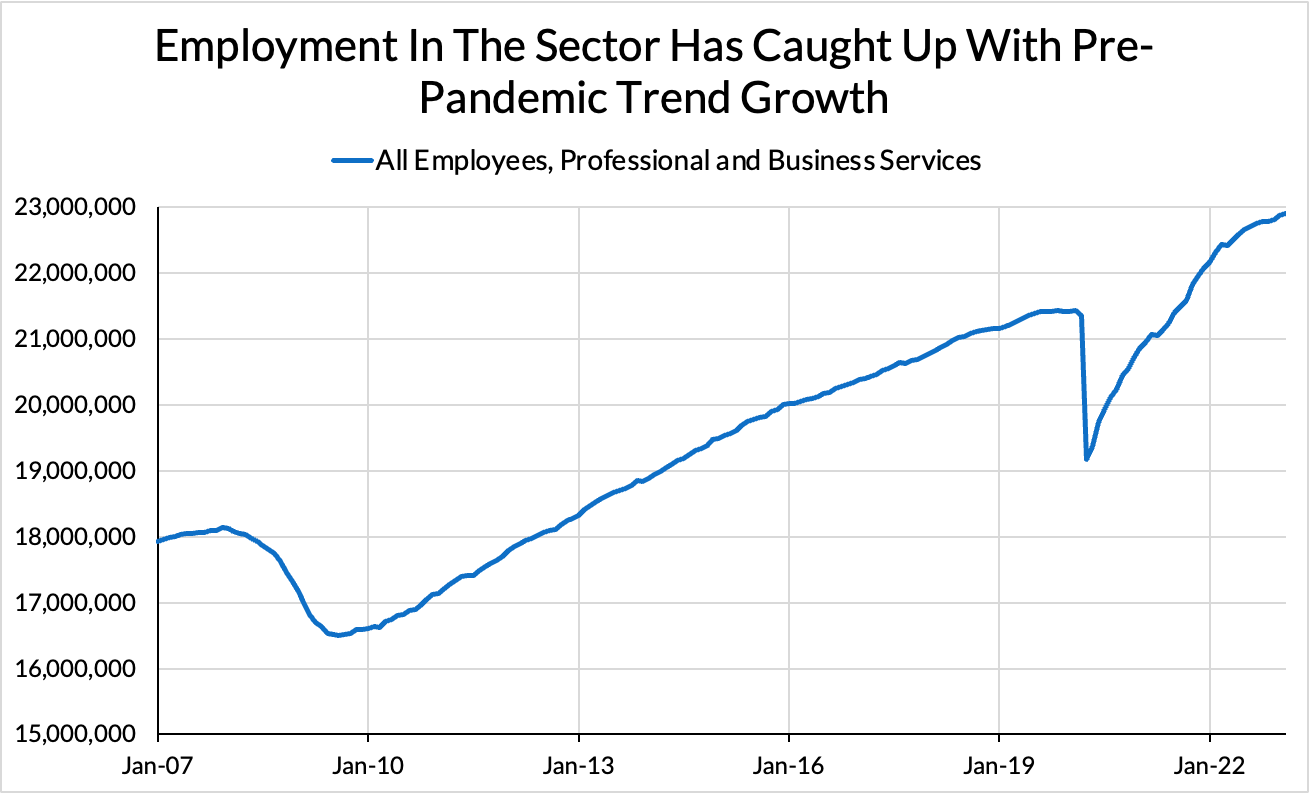

On the one hand, this labor market outcome looks like a soft landing. Employment is still growing, just at a slower pace, after the sector caught up with its pre-pandemic trend. Continued labor market cooling along these lines — an “endogenous slowdown” — would likely help the economy exit the pandemic recovery without a sharp recession or need of very-high interest rates to slow activity.

However, digging in closer, we see that Professional and Business Services is made up of a handful of sectors whose labor markets differ from one another in ways that will likely matter in the event of an industry-wide slowdown.

The first subsector, NAICS 54 is mostly accountants, architects, management analysts, and lawyers, who are seeing hiring begin to soften a bit, but who have notched significant employment gains since the onset of the pandemic. The second subsector, NAICS 55 is a similar group, mostly accountants and financial managers, with a number of supervisors and operations managers included as well. Hiring in this subsector shows less sign of slowing.

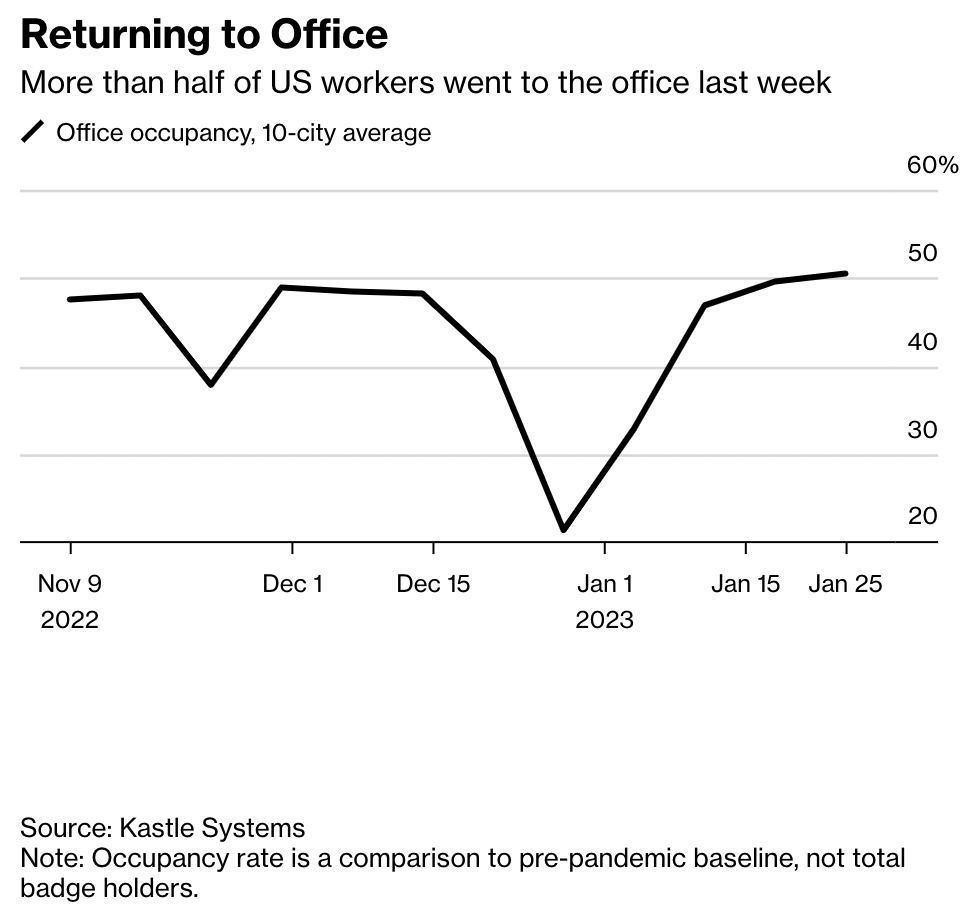

Unlike the first two subsectors, NAICS 56 has seen hiring stagnate as office occupancy rates stall out around half pre-pandemic rates. This is more straightforward once we recall that this sector is mainly the janitors, landscapers, security guards, office clerks, and freight workers who keep buildings running day to day. Compared to NAICS 54 and 55, workers in this sector tend to have lower wages, less job security, and will be vulnerable to a further downturn in commercial real estate if one arises.

As a recent article from Bloomberg shows, occupancy has struggled to reach even half of its pre-pandemic rates.

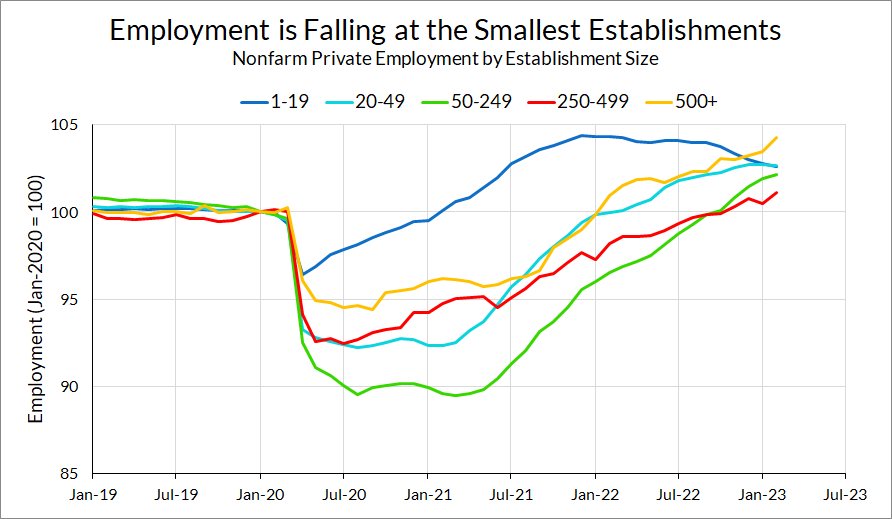

Turning to employment at small vs. large employers, employment at the smallest establishments has been falling over the course of 2022, while employment growth at larger establishments remains relatively strong. One potential explanation for this pattern is that the tight labor market has enabled people to job-hop to higher-paying employers which are generally larger.

In short, employment related to commercial real estate and small businesses is already under stress from post-pandemic recovery dynamics. These are also the parts of the labor market that would suffer disproportionately from a pullback in lending from small and regional banks. A further collapse in employment in these areas isn’t guaranteed, but it is something the Fed should be on the lookout for as the fallout from this month’s events in financial markets settles.