Fed Note: Why We Think Risks Are Tilted Towards A Hike

We see the FOMC moving towards a tightening bias and raising rates at some point in the next twelve months—with or without Warsh.

We see the FOMC moving towards a tightening bias and raising rates at some point in the next twelve months—with or without Warsh.

Our current Fed base case:

Inflation is greatly outperforming the Fed’s projections for this year. The median projection for both headline and core PCE inflation in the March SEP was 2.7%; after the PPI data, we expect those figures to come in at 3.8% and 3.3%, respectively, in April. PCE inflation would have to average just 1.3% annualized for the remainder of the year for PCE inflation to come in at 2.7%.

Many analysts and commentators have primarily been attributing the overshoot to tariffs and the commodities shock from the Strait of Hormuz closure. Standard monetary policy practice tells you to look through those as they are seen as one-time price level adjustments rather than underlying inflation, as long as expectations remain anchored. While we agree with those assessments, a closer look under the hood of the data paints a more concerning picture. Inflation has been running hot even prior to the Hormuz shock, which was one of the reasons we made the call of an indefinite hold from the Fed prior to the shock.

Tariff effects are running hotter than what the Fed projected and there is still scope for more tariff-driven inflation. Tariffs have yet to hit auto inflation but we anticipate it could later this year. Moreover, some firms have held off on passing costs onto consumers due to legal uncertainty and the tariff whiplash experienced since Liberation Day. With the court striking down IEEPA, the administration is going to implement tariffs under legal authorities such as section 232 and 301s. Implementing tariffs via these measures make tariffs more predictable, durable, and diminishes policy uncertainty. When these are implemented – the admin has signaled sometime in 2H2026 – there is scope for more upside tariff-inflation risk. At best this means the median member of the committee will want to maintain rates at best, absent clear labor market and financial market risk. The bigger risk is if services adjacent to tariffed goods (e.g. auto goods tariffs bleeding into in auto services inflation) create another period of extended price acceleration. If this dynamic starts to occur, it will become difficult for a majority of the FOMC to “look-through” tariffs.

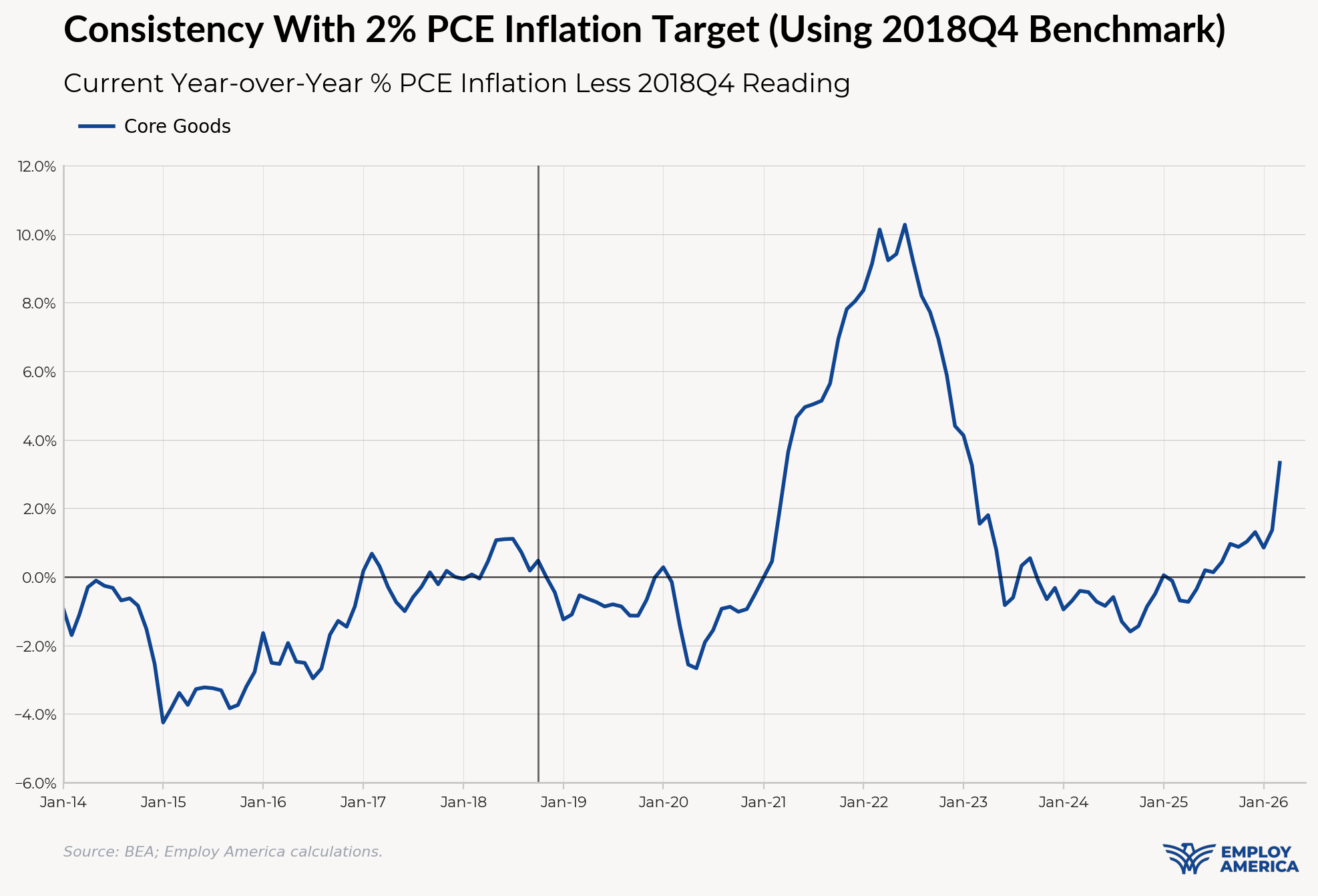

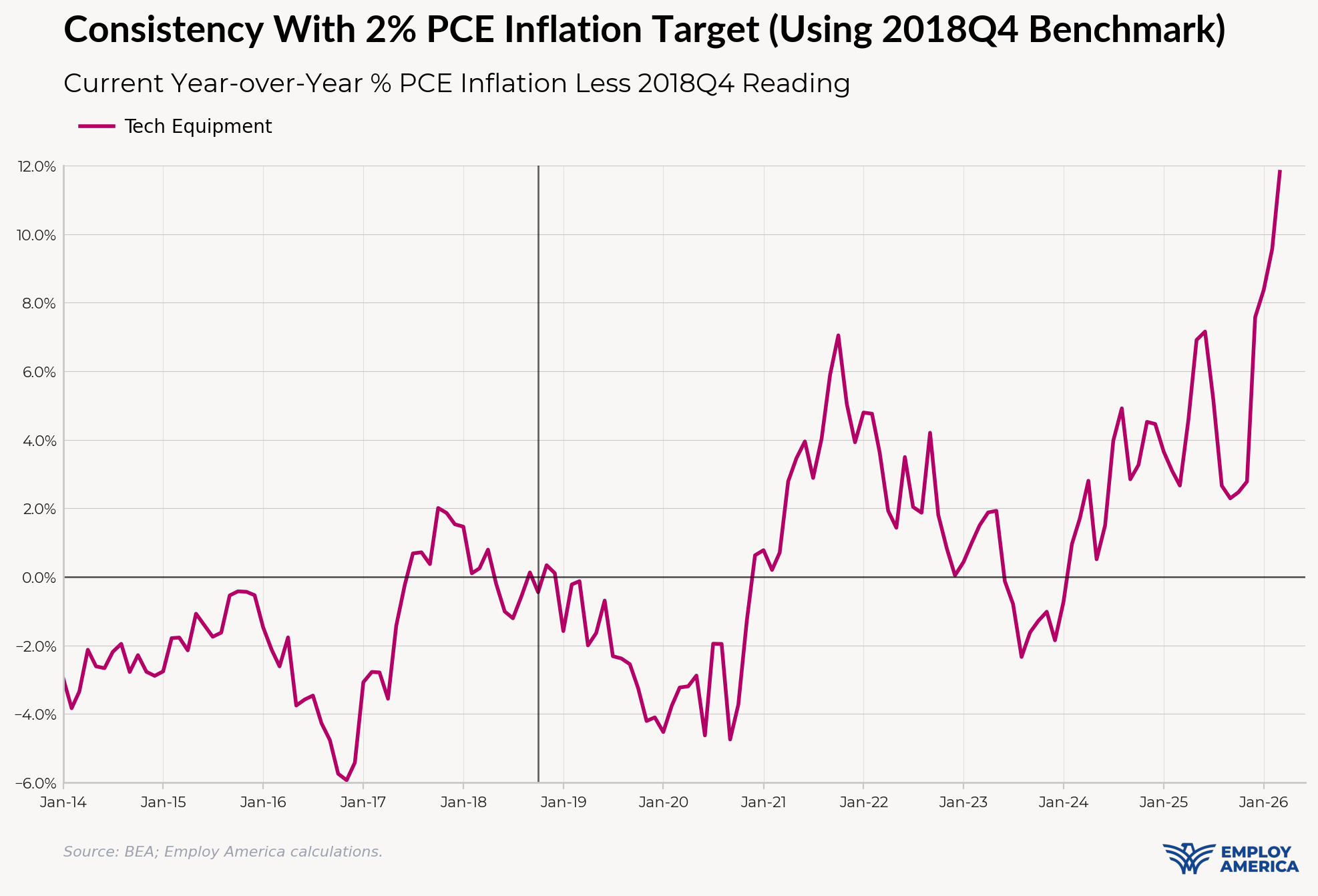

There is also a wave of goods inflation stemming from bottlenecks in the AI-boom that have led to inflation for computer hardware and smartphones. This is primarily driven by a shortage of dynamic random memory access (DRAM) as of now. DRAM is an input that goes into several consumer goods such as motor vehicles, TVs, appliances, and streaming and gaming devices. Computers, smartphones, and components such as semiconductors are currently exempt from tariffs. While hedonic adjustments could cancel out the inflationary impact, more persistent shortages could lead to production declines which could push up inflation in these categories. There have also been reports of shortages of other inputs such as transformers, aluminum, copper, wiring, switchgear, circuit breakers, and natural gas turbines.

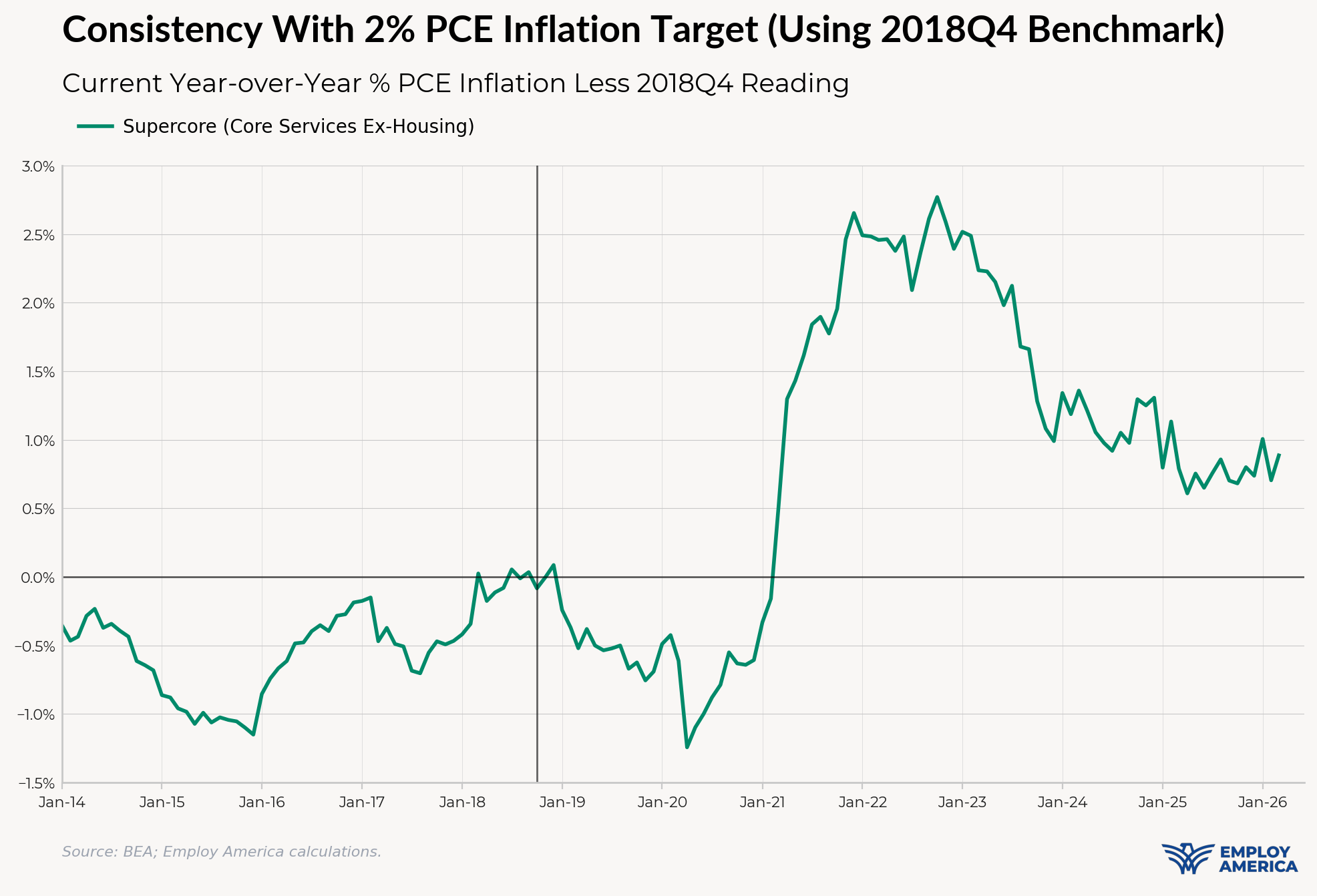

Perhaps the most problematic measure for the FOMC right now is Supercore (core services, ex-housing). Food services, airfares, healthcare have been running hot for several months now and lodging has recently picked up. We see upside risk for these categories ahead. The Hormuz shock is adding upside risk to airfares and food services. There are also food price dynamics unrelated to the Hormuz shock that add upside risk to food services. World Cup-related tourism demand could also add further upside risk to lodging, transportation services, and potentially food services.

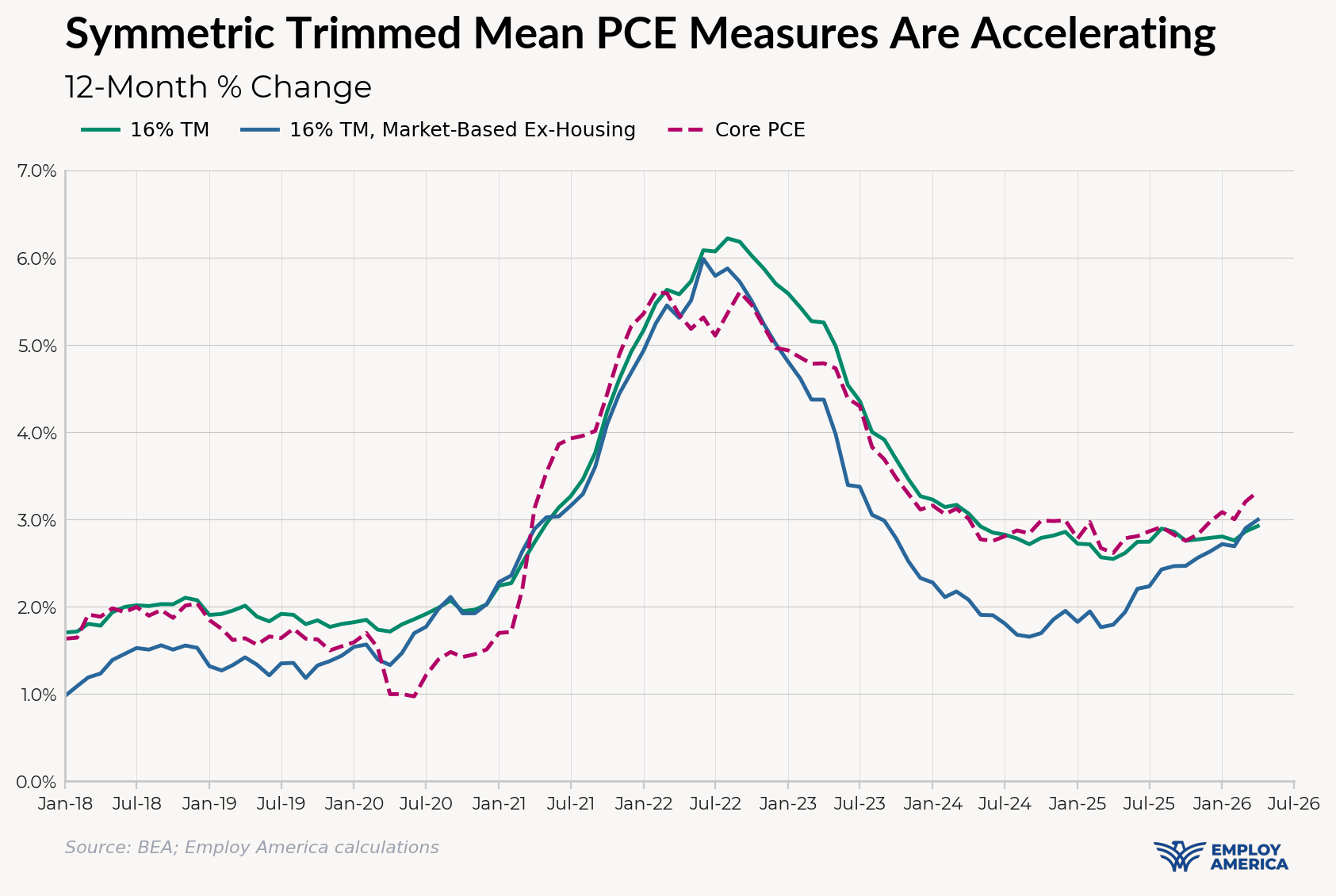

It’s one thing for the Fed to stomach looking through “transitory” inflation coming when there is just one cause to look through; it’s quite another thing for them to look through a multi-causal story. The more complicated the story, no matter how supply-side or one off in nature, the more skeptical Fed officials tend to behave in practice. Symmetric trimmed mean measures of PCE inflation (which FOMC members are likely watching) are already accelerating and make it hard to simply cherry pick flattering inflation gauges.

Meanwhile, the labor market appears to be solidifying, with nascent signs of acceleration. We got a relatively clean read of the labor market with April’s data, and there wasn’t much to worry about. Prime-age employment has held steady near its pre-pandemic peak for three months. The unemployment rate is 4.34%, under the last SEP’s projection for 2026, and has been slowly falling in early 2026. The three-month pace of nonfarm payrolls growth is at about 50k, comfortably within (and perhaps above) where FOMC members see breakeven jobs growth. Cyclical industries’ payroll growth has picked up and has been outpacing acyclical industries’ payroll growth over the last three months. Hiring rates may have troughed and posted wages have been climbing. While it’s too early to call this a labor market reacceleration, these are all signs of a labor market that is picking back up rather than falling apart.

The FOMC ending its easing bias is a foregone conclusion; the remaining questions are (a) how that will interact with having Kevin Warsh as a dovish chair and (b) if and when the Committee pivots to a tightening bias.

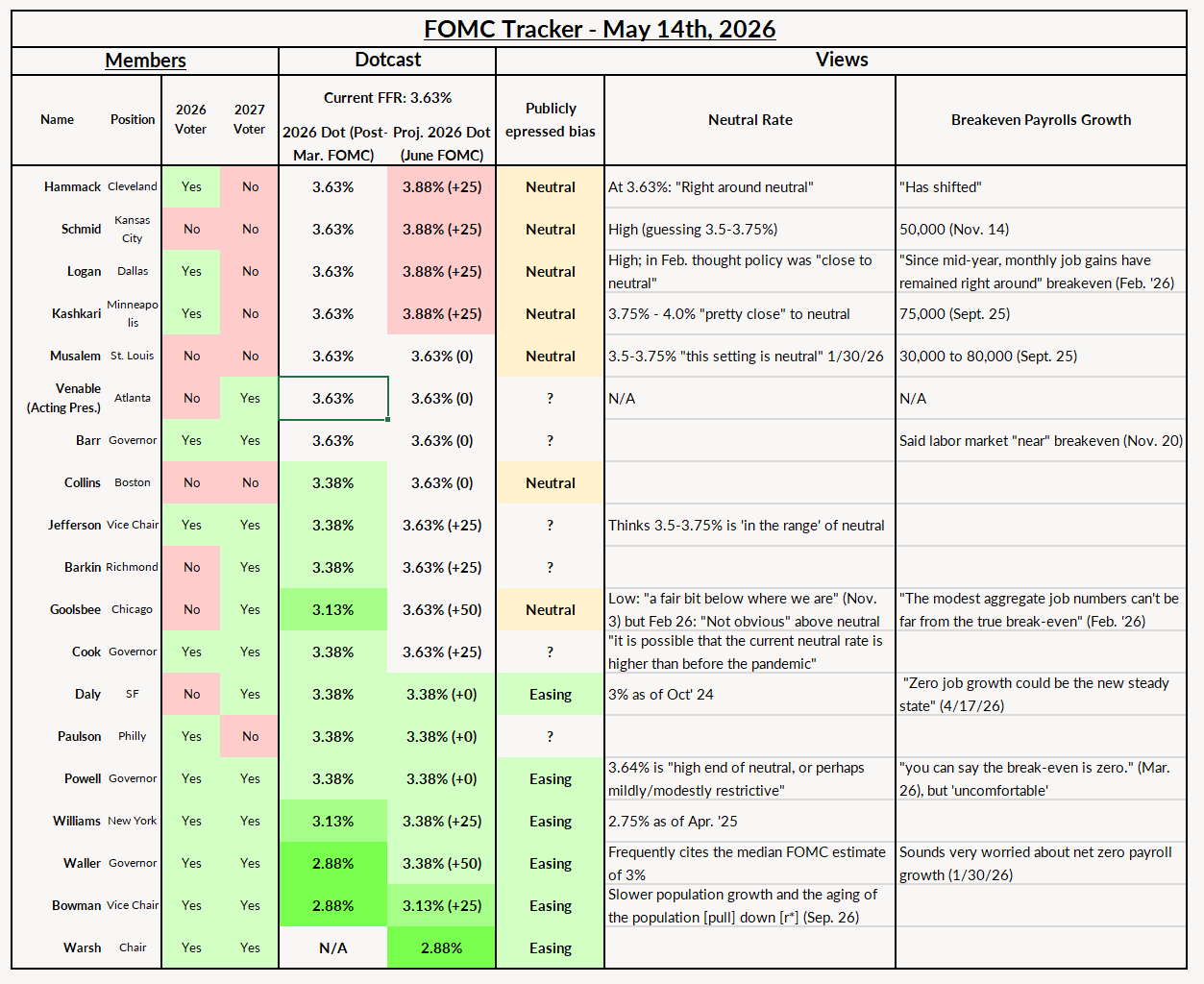

We are at the point where about half of the Committee is either symmetric in its interest rate outlook or will adopt at least an implicit tightening bias. In the wake of the FOMC meeting earlier this month, we’ve heard explicit expressions of a symmetric outlook from the dissenters as well as additional non-voting members of the FOMC.

This is our run-down of where the FOMC members are (2026 voters in bold, 2027 voters in italics), from most hawkish to dovish:

From Kevin Warsh’s perspective, his advantage is that the voting power on the Committee is heavily skewed towards the Board of Governors. He may not be able to get cuts, but with six votes from himself, Bowman, Waller, Williams, Powell, and one of Paulson (2026 voter) and Daly (2027 voter), he could prevent hikes. Warsh’s position as Chair may command some deference from the rest of the Committee, but his arguments for easing (cherry-picked soft inflation measures and a strong belief in the potential productivity growth) have generally been met by strong skepticism from the Committee.

In short: the path to a hike as the next move likely lies through the constellation of data arranging in a way that some combination of at least Daly, Paulson and Powell are willing to go against the Chair and vote for a hike. Of those, Daly is still talking dovish (even after last week’s labor market data), and Powell will probably be reluctant to be seen as leading a revolt against the Fed Chair. If we hear Paulson give up her easing bias soon, it makes a 2026 hike more likely given the voting rotation this year.

We should also point out that we are entering uncharted territory here. It is unprecedented for the Chair of the FOMC to be this far from the central tendency of the overall Committee. How exactly that plays out is subject to a lot of uncertainty. While we've seen signs from the most hawkish part of the Committee that they're willing to go against the Chair, he may still get enough deference from the swing voters to avoid a hike. We will be watching with great interest any statements from the likes of Jefferson, Cook, Daly, Paulson and Powell for signs of where the center of the Committee is headed.

They’re not there yet publicly, but if we continue to see inflation run this high (especially if inflation expectation measures start rising) and/or the labor market reacceleration to materialize, we see the FOMC moving towards a tightening bias and raising rates at some point in the next twelve months—with or without Warsh.