Core-Cast is our nowcasting model to track the Fed's preferred inflation gauges before and through their release date. The heatmaps below give a comprehensive view of how inflation components and themes are performing relative to what transpires when inflation is running at 2%.

Yesterday's CPI release showed so much promise for April PCE and yet today's PPI largely squashed those hopes. PPI came in strong a number of key dimensions, most notably within financial services (portfolio management) and international airfares. The import price data tomorrow also provides inputs for international airfare PCE and will thus have some outsized impact on the nowcast this month. While most of these processes are noisier and there was real forward-looking signal from CPI (especially in food services), the narrative inflection point is delayed. The Fed will not see a clear path to 2% following the upcoming PCE release. That moment will likely have to wait longer.

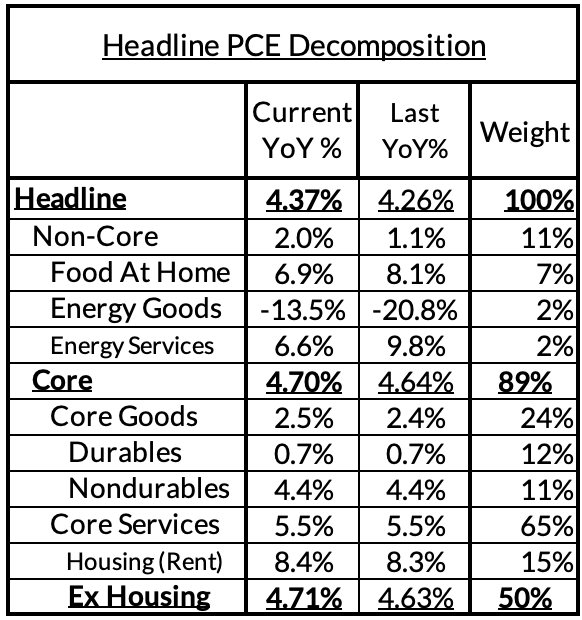

Headline PCE is now on track to rise, from 4.26%* year-over-year in March to 4.37% in April. (0.30% monthly increased, revised up from yesterday's 0.14% nowcast). *PPI revisions will push up year-over-year readings from 4.16% to 4.26% for April.

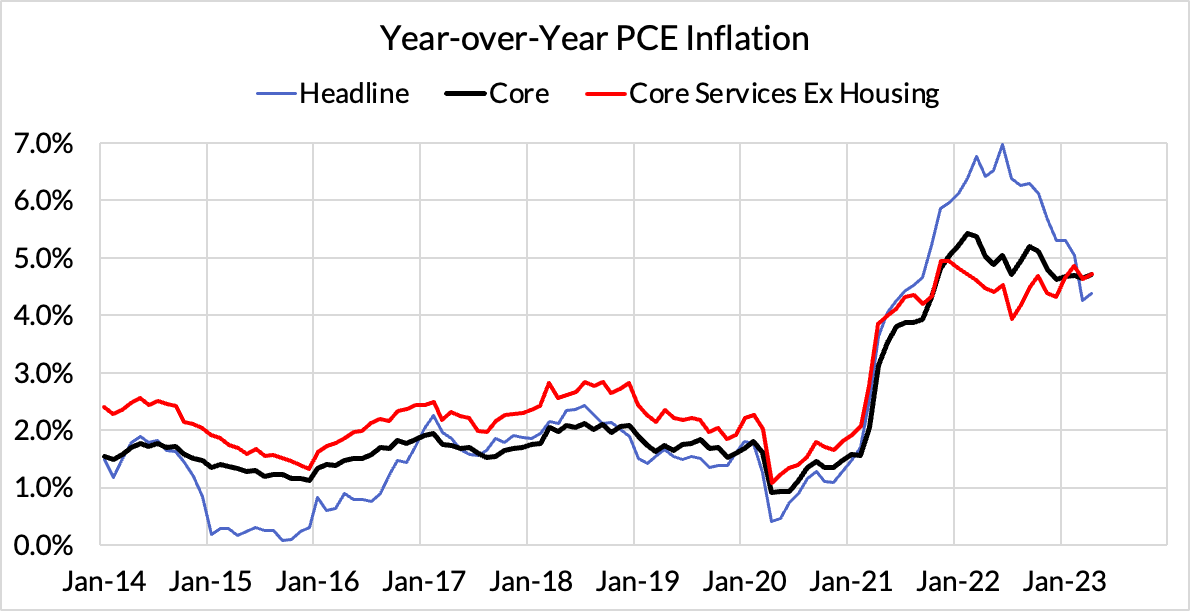

Core PCE is now on track to rise too, from 4.64%* year-over-year in March to 4.71% in April (0.38% monthly increase, revised up from yesterday's 0.20% monthly increase). Our cautionary notes about the importance of PPI bore fruit. *PPI revisions will push up year-over-year readings from 4.60% to 4.64% for April.

Core Services Ex Housing PCE (CSXHP) is now on track to rise, from 4.63%* year-over-year in March to 4.71% in April. (0.42% monthly increase, revised up from yesterday's 0.12% nowcast). *PPI revisions push up March year-over-year readings from 4.52%. We would still caution that the combination of revised consumption weights and the 'dark spaces' of PCE can still lead to decent shifts with where are nowcast is tracking. When core PCE is running at 2%, CSXHP typically runs at 2.68%. The current overshoot is effectively 203 basis points (195 basis points as of March).