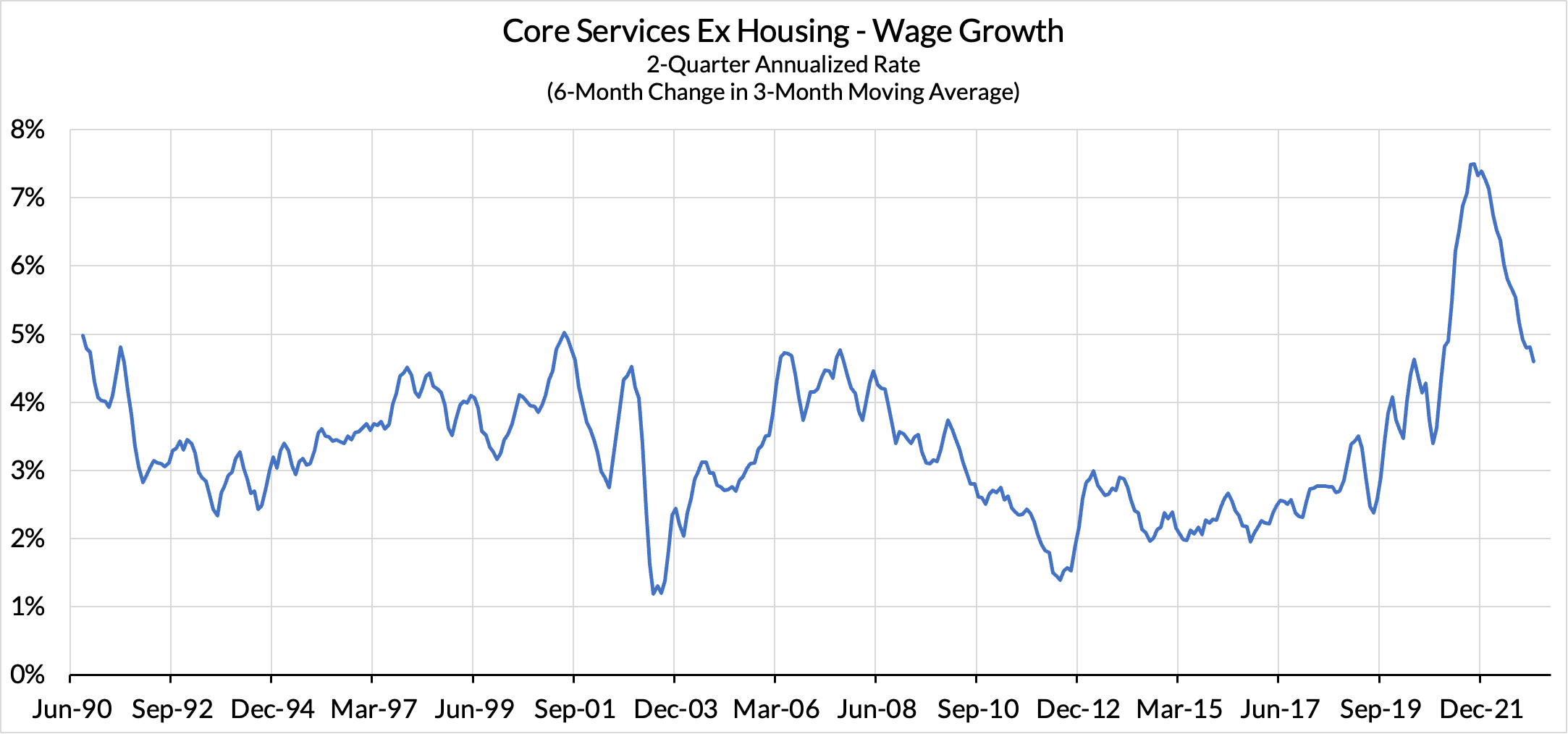

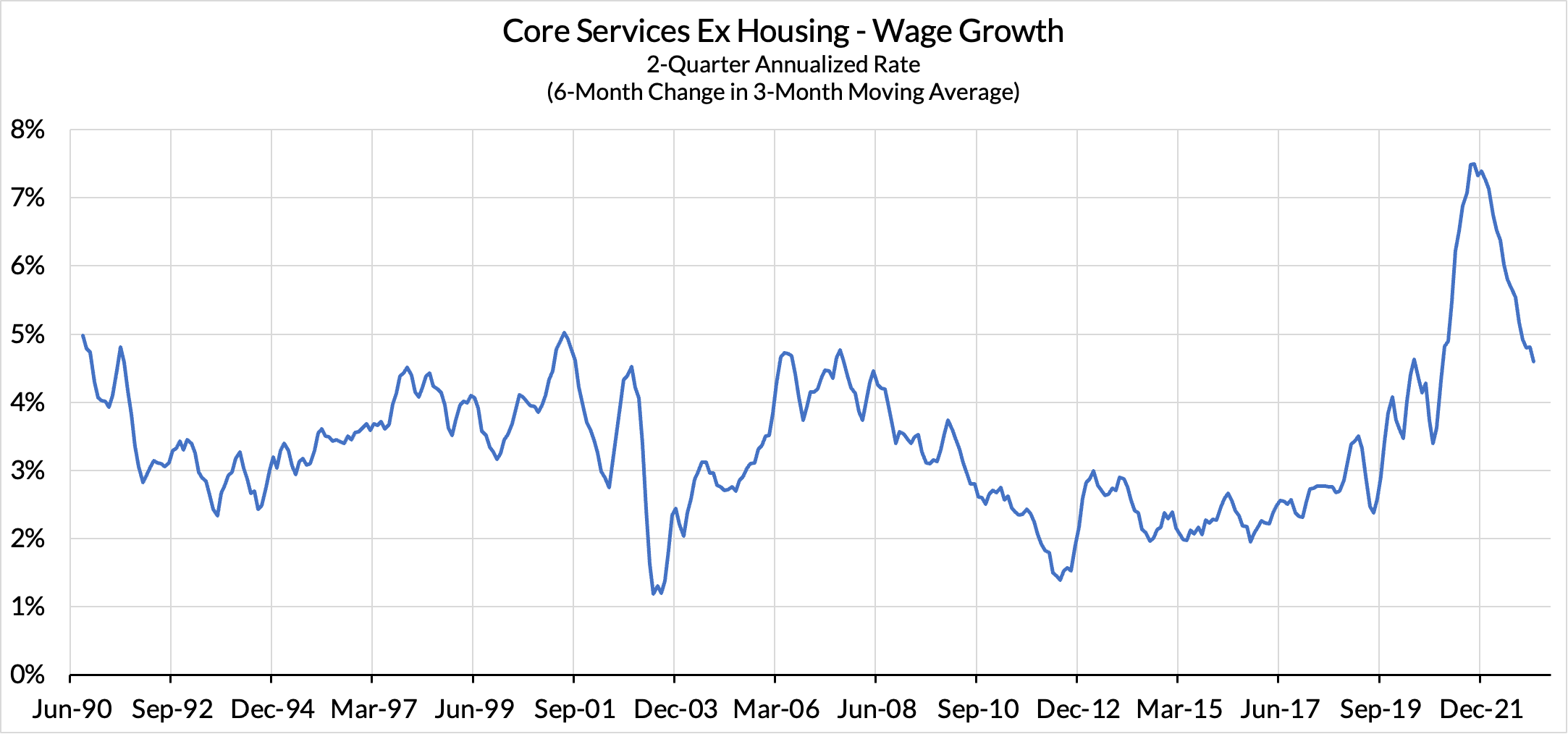

Summary: If we focus on the domestic labor that contributes to "Core Services Ex Housing PCE" output, we see that wage growth is no longer looking so hot. Labor cost pressures on "Core Services Ex Housing" PCE inflation are diminishing. Within the Fed's preferred framing of inflation dynamics, this wage deceleration dynamic should firmly diminish the case for further rate hikes to tame inflation. As it stands now, the Fed still has yet to appropriately acknowledge this labor cost dynamic.

The data is showing two clear facts: (1) labor cost pressures surged around the reopening process subsequent to the pandemic but also (2) have been decelerating for over a year now. Smoothed near-term growth rates show that CSXH wage growth is now running at the same growth rate as it did 2006-07 and 2000-01.

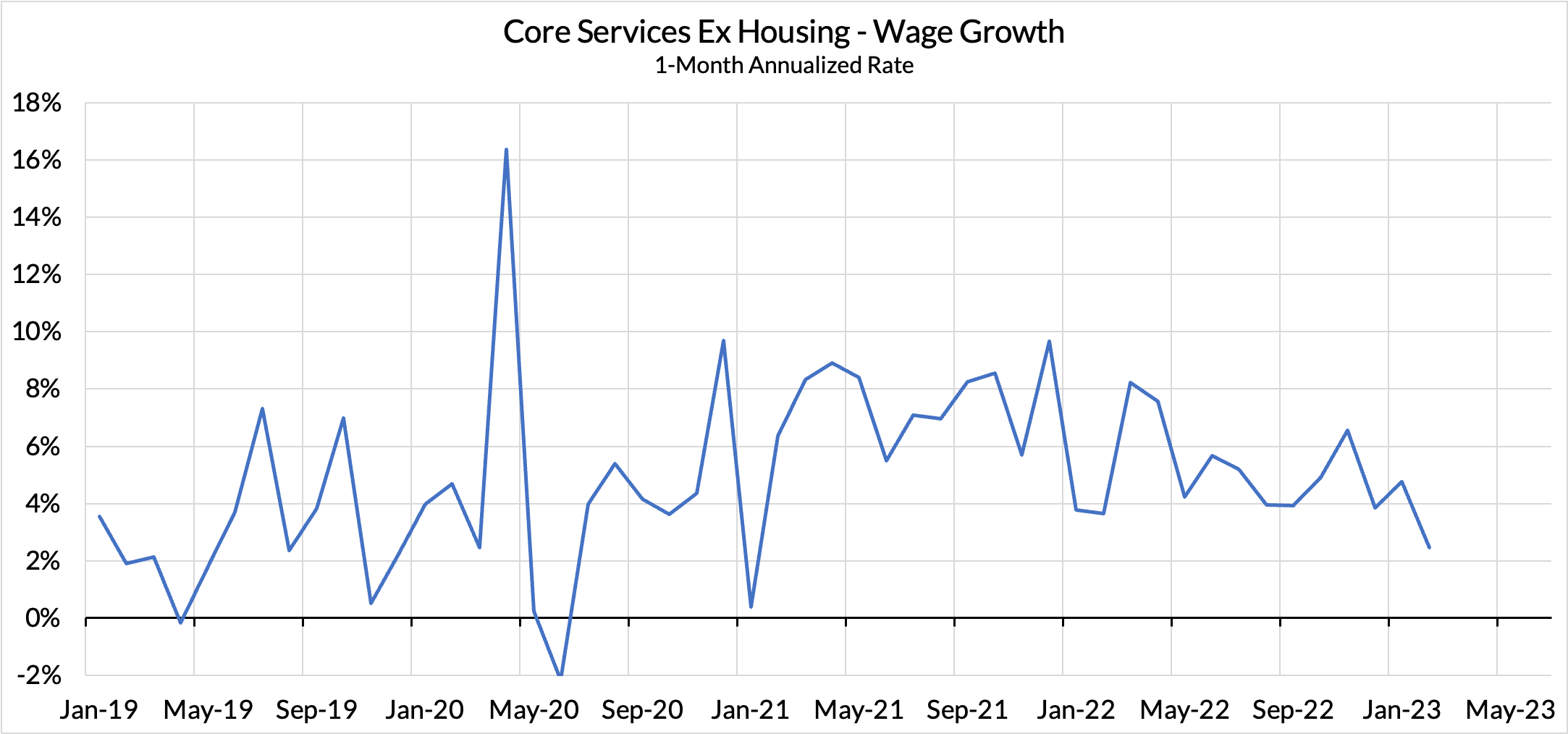

More strikingly, the near-term data has reflected more deceleration than what is captured in the above "smoothed" measure.

If the Fed believes that its policies work on inflation primarily through the labor market (we agree there), and the labor market's pressure on non-housing services inflation is dissipating, the Fed's case for weakening the labor market further should also diminish.