Financial Conditions Monitor: Tracking Market-Implied Growth, Inflation, and Fed Expectations

We systematically track the evolution of financial conditions and their underlying drivers. This monitor is a reflection of how we think macroeconomic and policy dynamics are affecting financial conditions and, by extension, our assessment of the economic growth outlook.

We systematically track the evolution of financial conditions and their underlying drivers. We intend to share regular updates of these systematic monitors with our donors on a more exclusive basis (so long as it does not compromise our public mission). This monitor is a reflection of how we think macroeconomic and policy dynamics are affecting financial conditions and, by extension, our assessment of the economic growth outlook. If you are interested in becoming an Employ America donor, feel free to reach out to us here.

Takeaways:

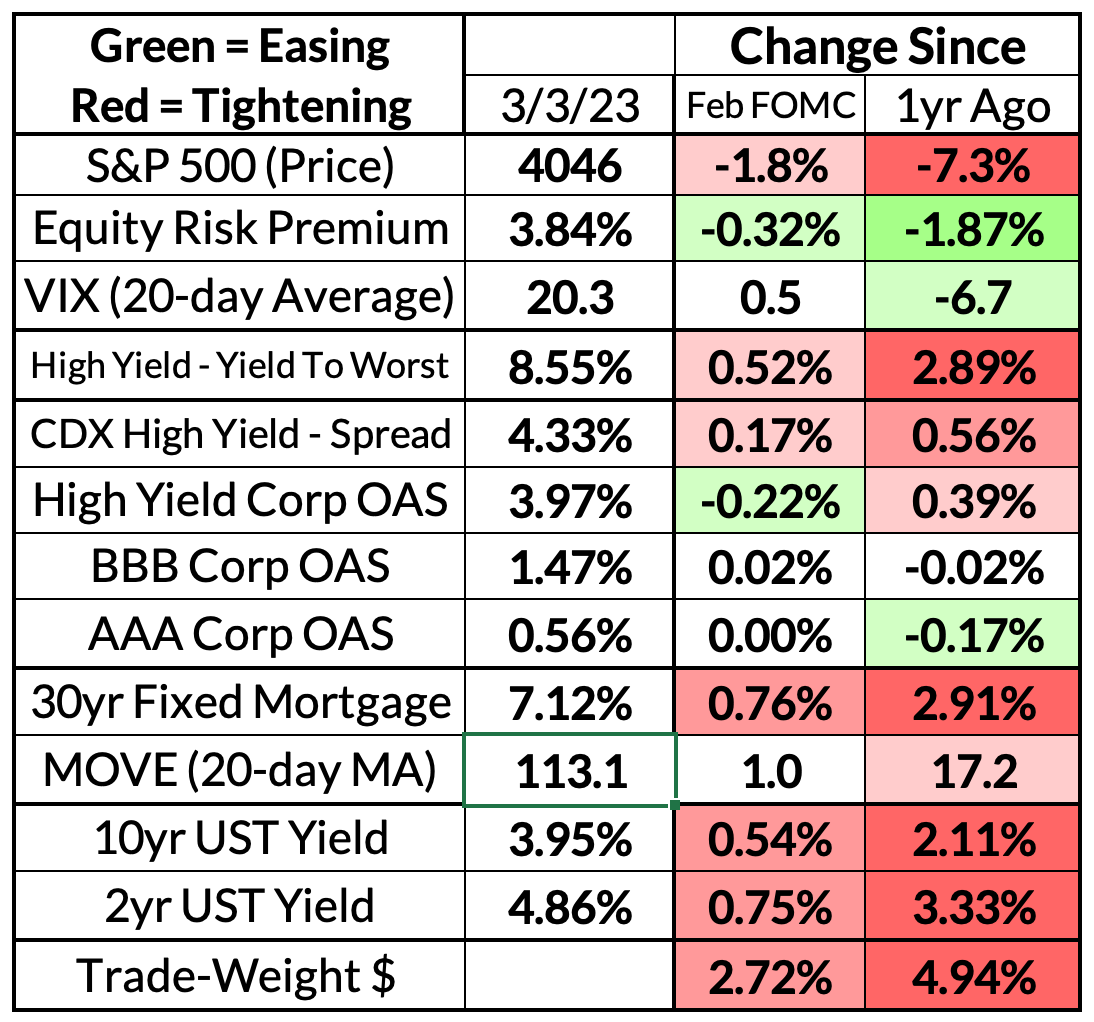

Financial conditions have tightened since the February FOMC meeting largely in response to stronger growth and inflation information. This certainly does not seem like a recessionary tightening of financial conditions. At an asset class level, Treasury yields, credit spreads, and the dollar are the source of tightening. In the context of hot PCE inflation, resilient US growth, and market-implied expectations of both, it is not a surprise for Fed policy rate expectations to also rise.

We are still observing net tightening in most of the relevant barometers, after a mini-reversal in December and January. As of now, this tightening seems to be in response to strong growth and inflation, rather than an original cause of weaker growth. Conditions are still much tighter than they were a year ago.

There are asymmetric risks of the Fed engaging in hawkish panic. Residual seasonality is still showing its face in Q1, both in strong labor market data and strong inflation data. The risk now is that the Fed reaccelerates back to 50bp hikes as a result. We think this would be an overreaction, but the Fed's hawkish posturing does raise a scenario which is not factored into financial conditions and the baseline growth outlook: what if February CPI comes in hot and financial markets price in a 50 basis point hike at the March meeting (during the blackout period)? We think/hope that the Fed would simply use the dot plot to signal marginal hawkishness, but there is a risk the Fed tries to opportunistically preserve all tightening that is already priced in. These issues will still lurk ahead of the May FOMC meeting.

Financial Conditions Components

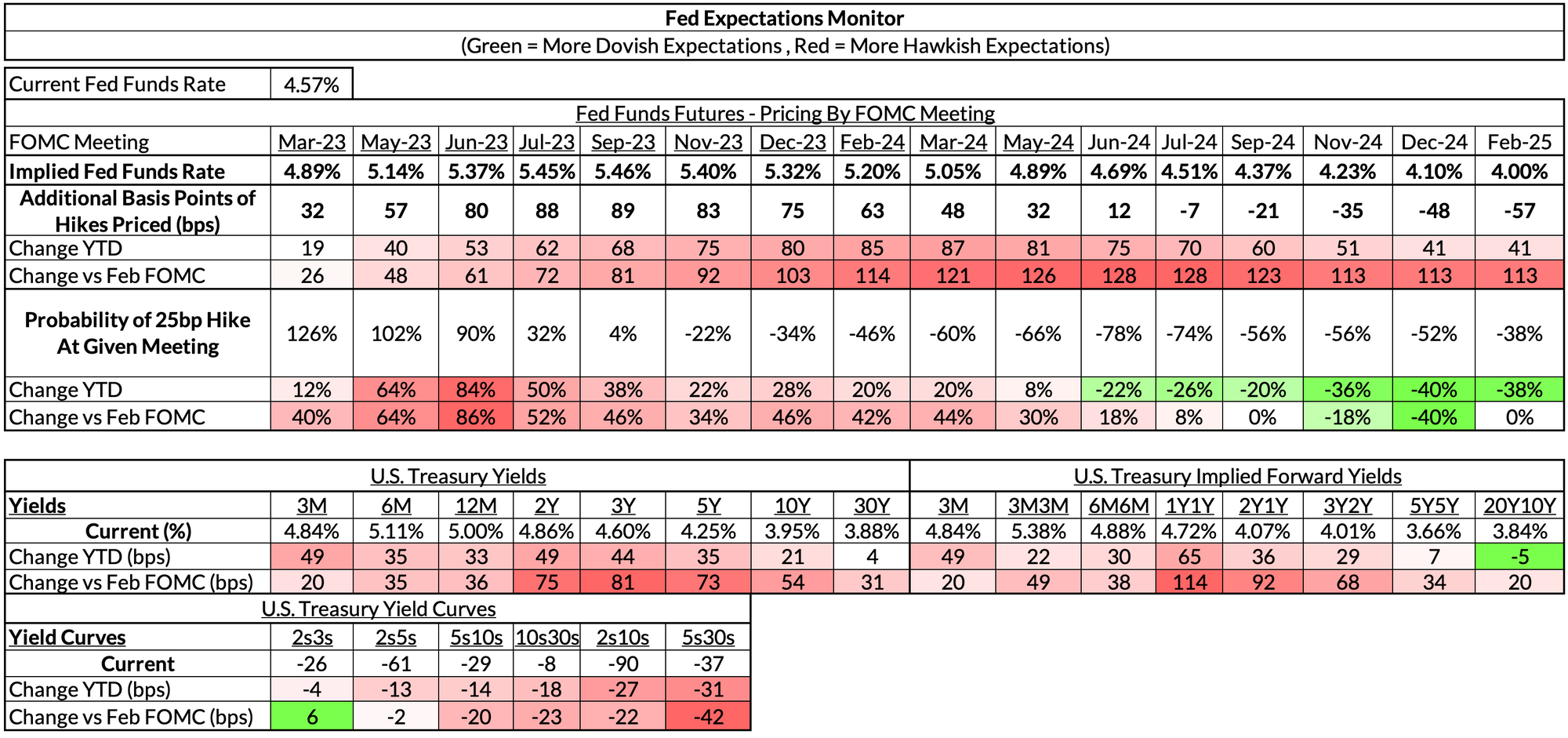

Fed Pricing

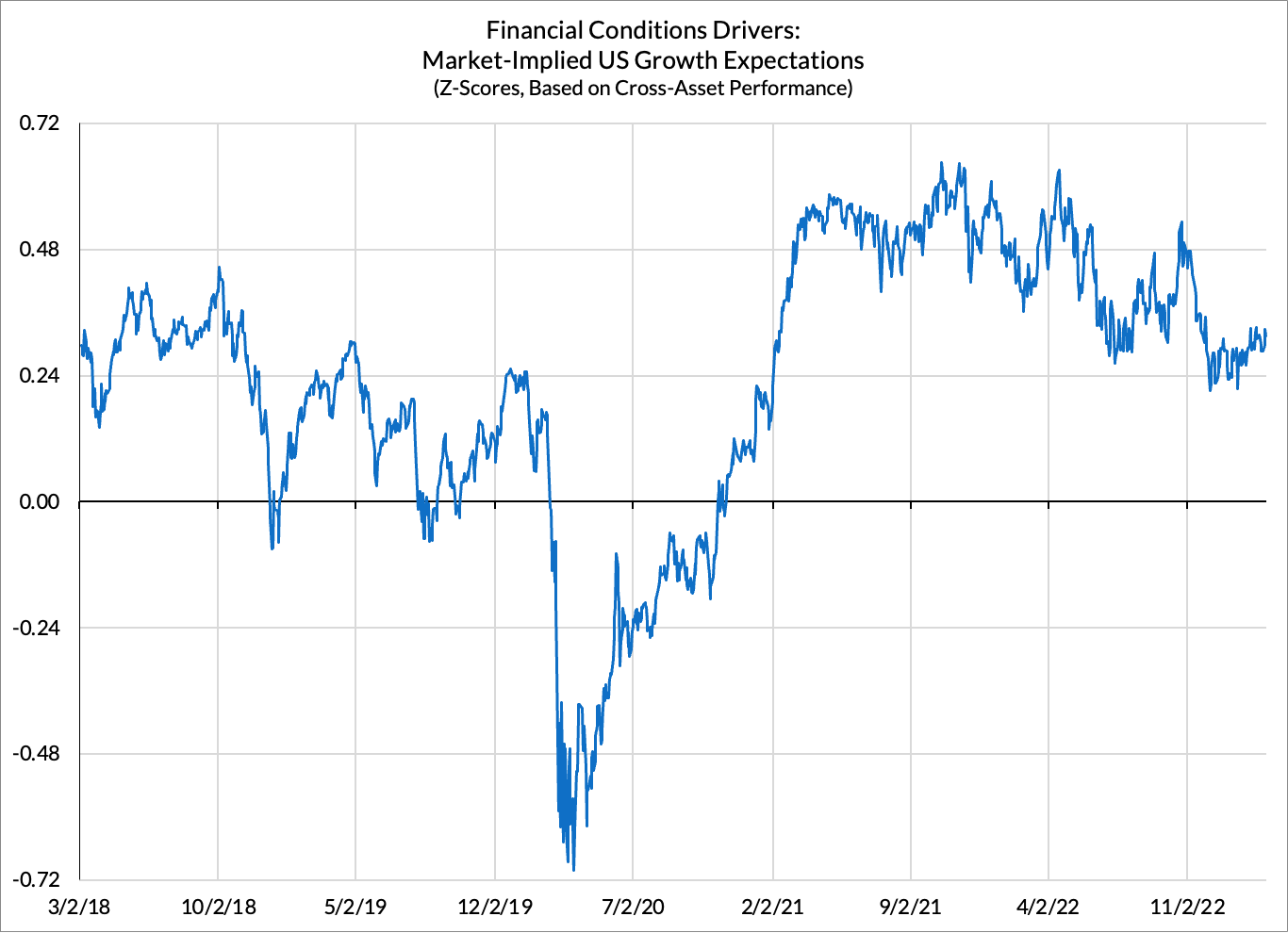

Market-Implied Growth Expectations

While we see financial conditions tightening tempering the growth outlook, it's worth being clear that financial conditions are themselves responding to a more upbeat growth outlook. Typically long-term interest rates do not move higher when a recessionary dynamic is firmly afoot.

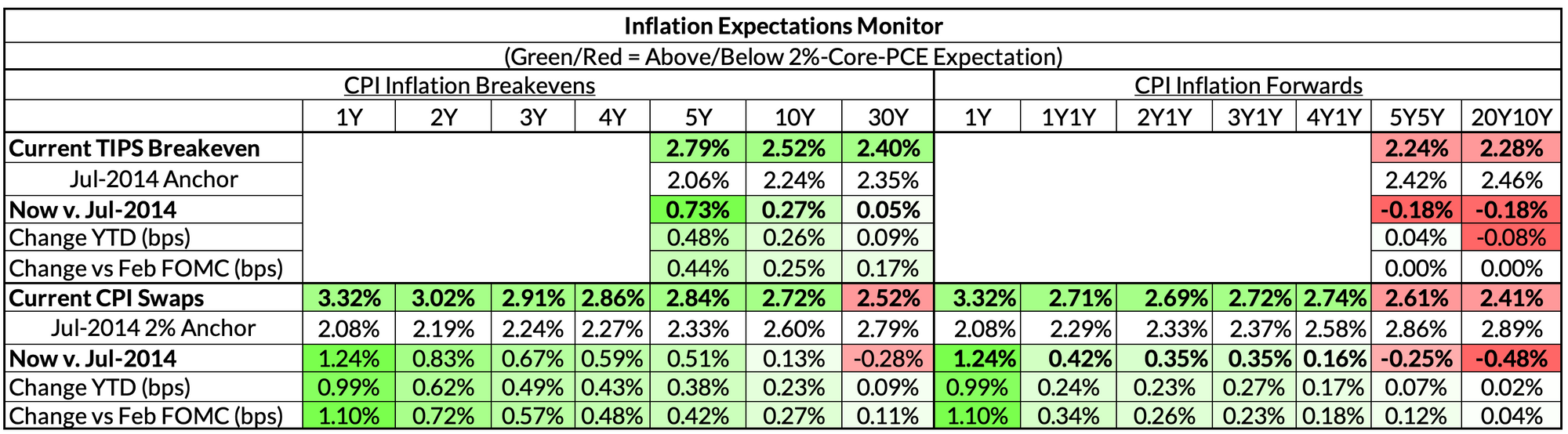

Market-Implied Inflation Expectations

Inflation expectations have moved firmly higher in the past month. As is typically the case, this is most apparent in pricing over the upcoming 12 months, which have repriced over 1.1% in the last 4 weeks. We suspect much of this is a recognition that the lags associated with rent and OER inflation will affect CPI longer than previously anticipated. Nevertheless, this upward rerating of inflation expectations is also adding ~0.3% to expected CPI in 2024, 2025, and 2026 and about 0.4% above what would be consistent with 2% PCE. While we are skeptical of most inflation expectations measures, we think market-implied expectations are the most compelling. More importantly, the Fed is surely paying attention.

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.