May Inflation Preview: The Rent & OER Relief Are Poised To Add Downside Risk Throughout The Summer

This is a truncated version of the preview initially made available to our exclusive distribution this past Monday. Core-Cast is our nowcasting model to track the Fed's preferred inflation gauges before and through their release date. The heatmaps below give a comprehensive view of how inflation components and themes are performing relative to what transpires when inflation is running at 2%.

Most of the Personal Consumption Expenditures (PCE) inflation gauges are sourced from Consumer Price Index (CPI) data, but Producer Price Index (PPI) input data is of increasing relevance, import price index (IPI) data can prove occasionally relevant. There are also some high-leverage components that only come out on the day of the PCE release.

If you'd like to start a 90-day free trial of our exclusive content, you can do so using this link. If you have any questions or would like to see samples of our past content, feel free to get in touch with us.

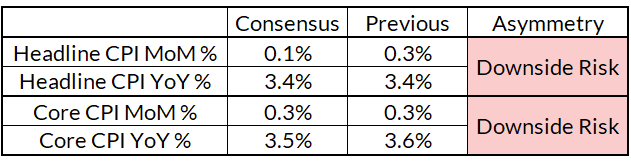

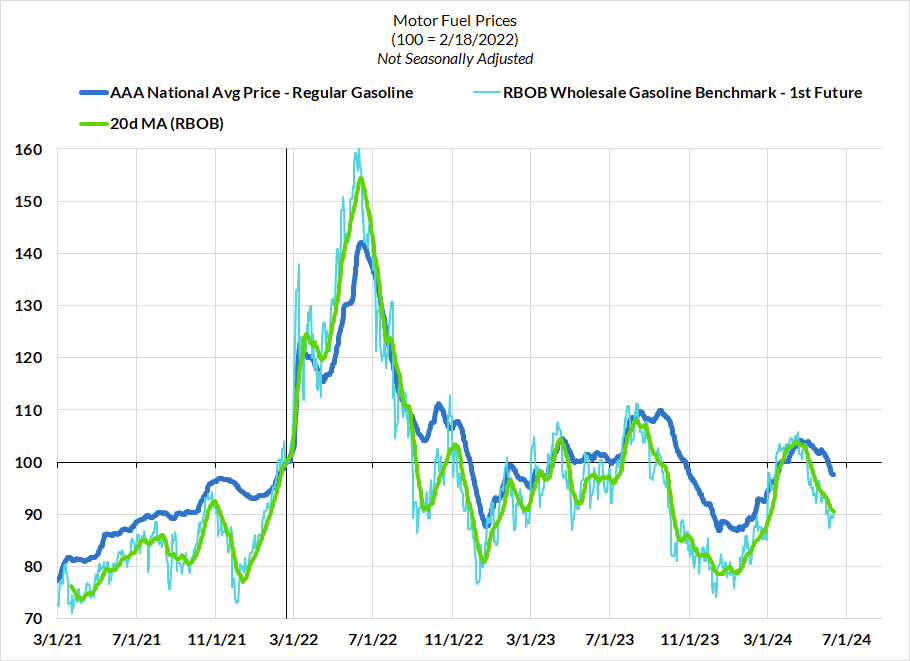

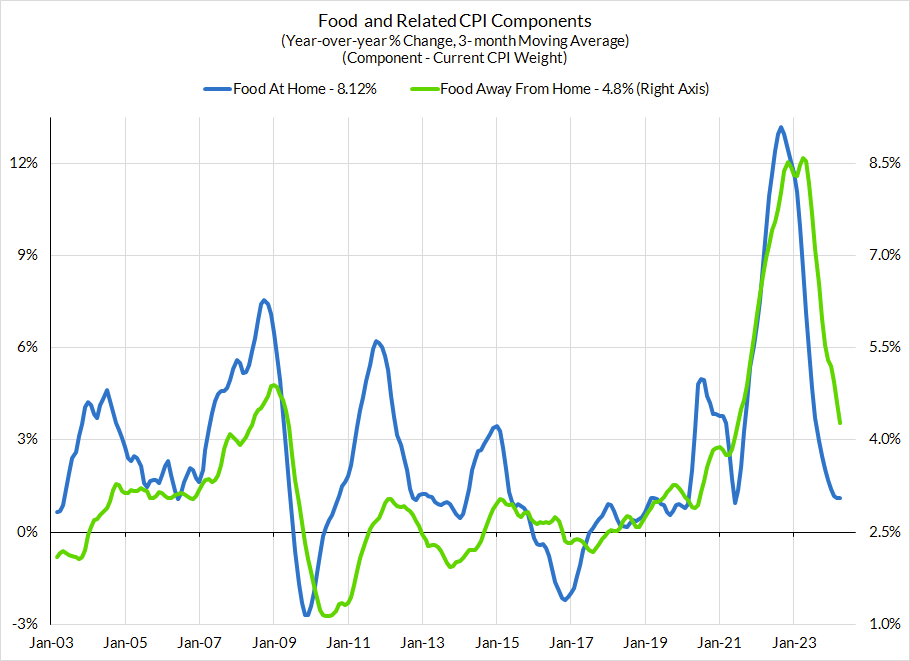

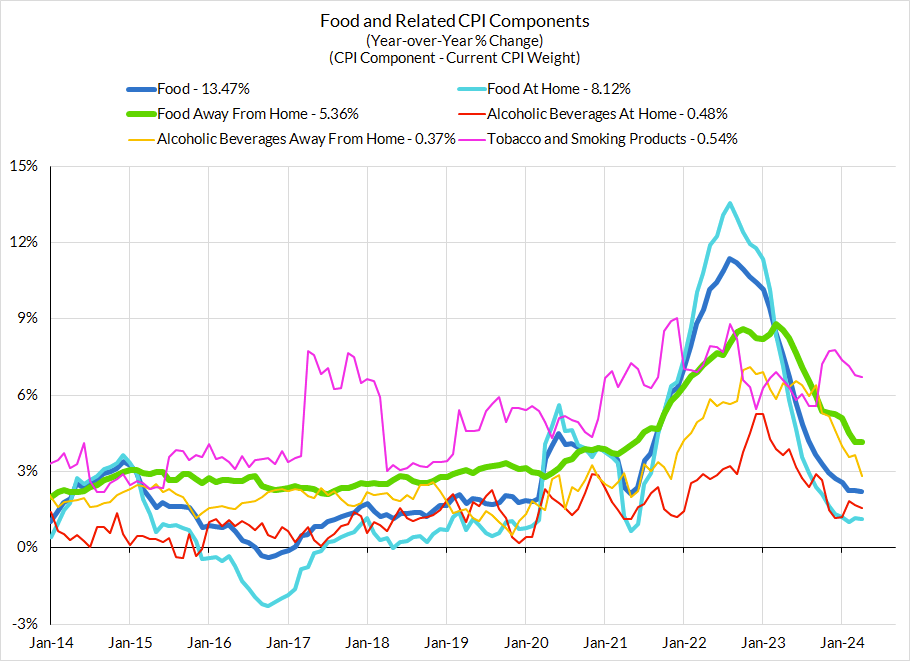

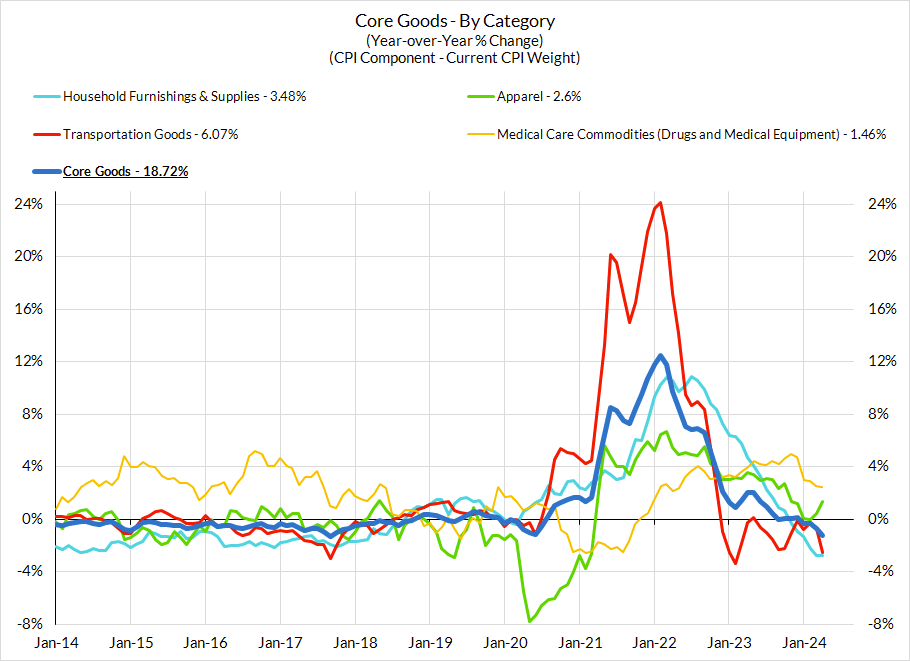

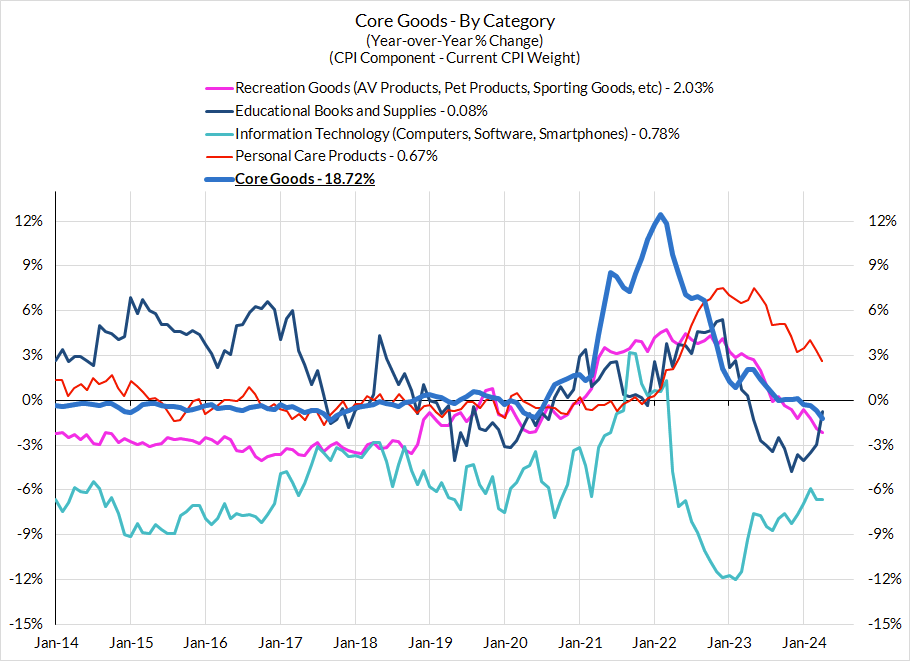

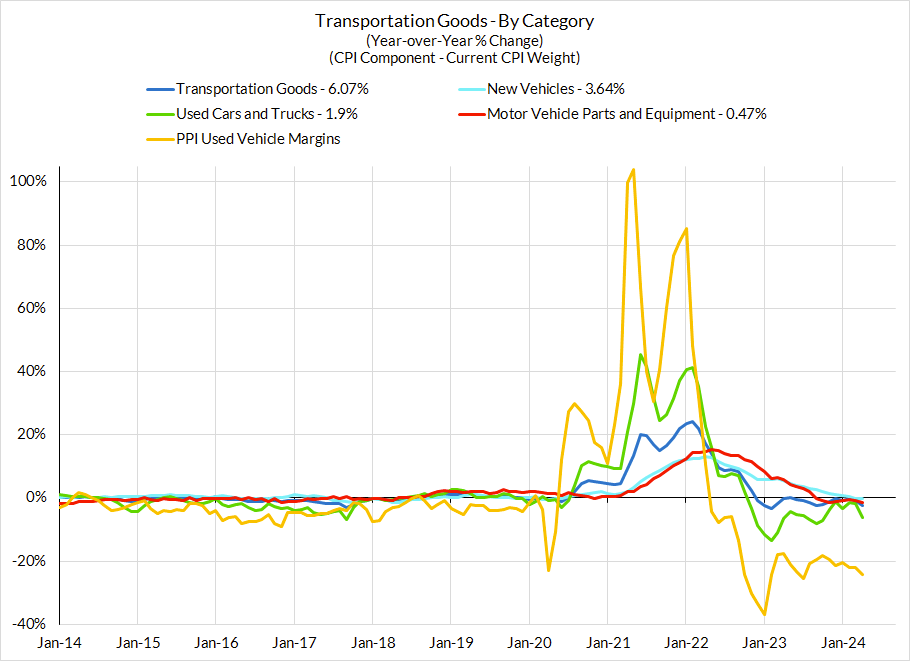

We see more downside risk vs consensus on both headline and core inflation: At the thrust of our inflation views is a more visible deceleration in rent (and owners' equivalent rent), new vehicles, and apparel inflation. These three have run stronger for different reasons but the combination of fundamental deceleration and favorable seasonals suggests at least less heat, if not meaningful cooling in outright terms. Energy prices are also poised to show more relief as gasoline prices begin falling through May and the first half of June, atypical for summertime. Falling grocery prices and decelerating food services prices should also aid "non-core" inflation.

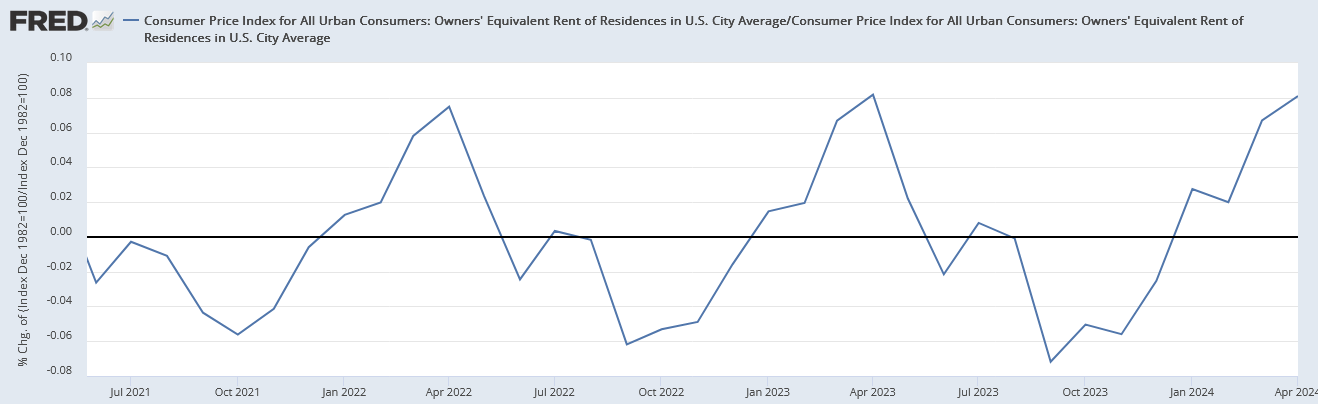

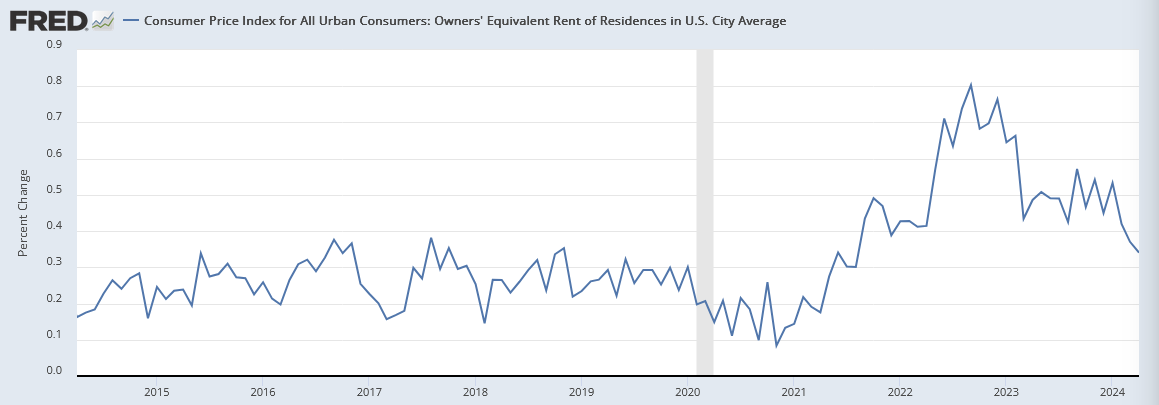

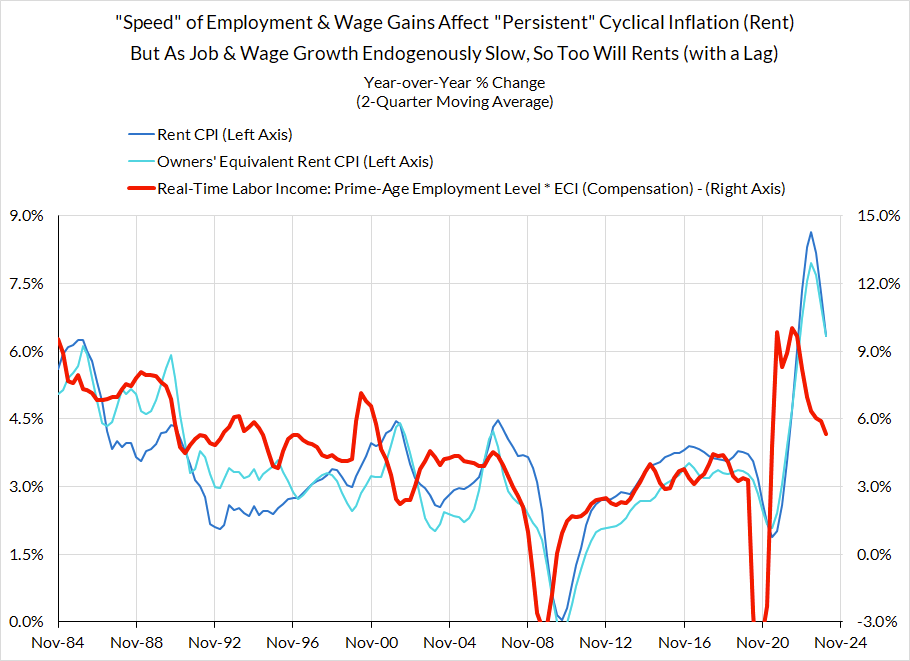

(1) Rent and OER are primed to show more visible seasonally adjusted deceleration: Rent and OER are showing more visible deceleration in the not-seasonally-adjusted (NSA) series than the seasonally adjusted series. While there is some seasonality in these time series, the latest revisions of the seasonal factors exaggerate how much of the deceleration in the first few months of the year is attributable to seasonality. Seasonal factors are currently adding 8 basis points to the NSA m/m OER CPI reading as of April. That support shifts to a 7 basis point drag by September, a net 15 basis point swing. This is technically of low relevance to aggregate core and headline CPI, but will be of relevance to Fed assessments and to how PCE inflation gauges get aggregated.

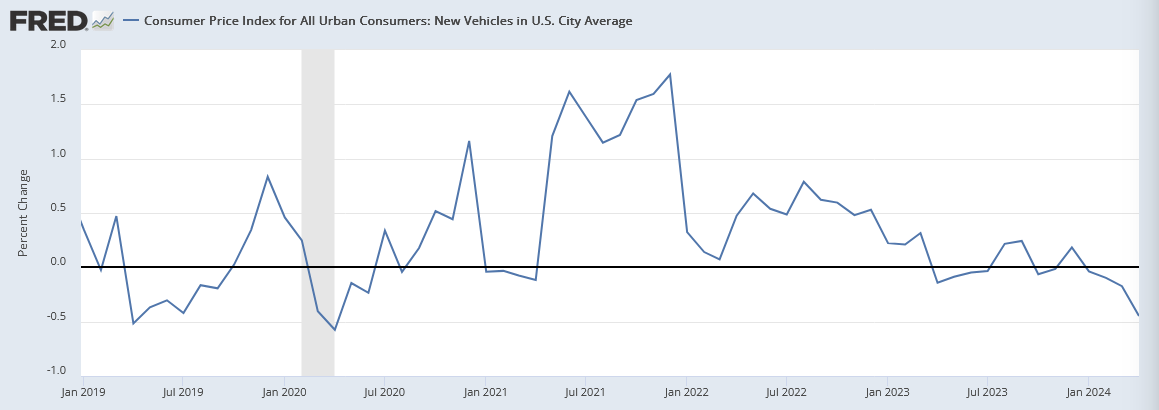

(2) New vehicle price deflation is finally poised to show up more meaningfully in the coming months. In April we saw what should be the first of multiple and sizable declines in New Vehicles CPI. Private sector data on new vehicle prices have long been signaling sizable price declines and CPI methodology choices suggest good reason for latency. That latency should ultimately give way to realized price declines through much of 2024.

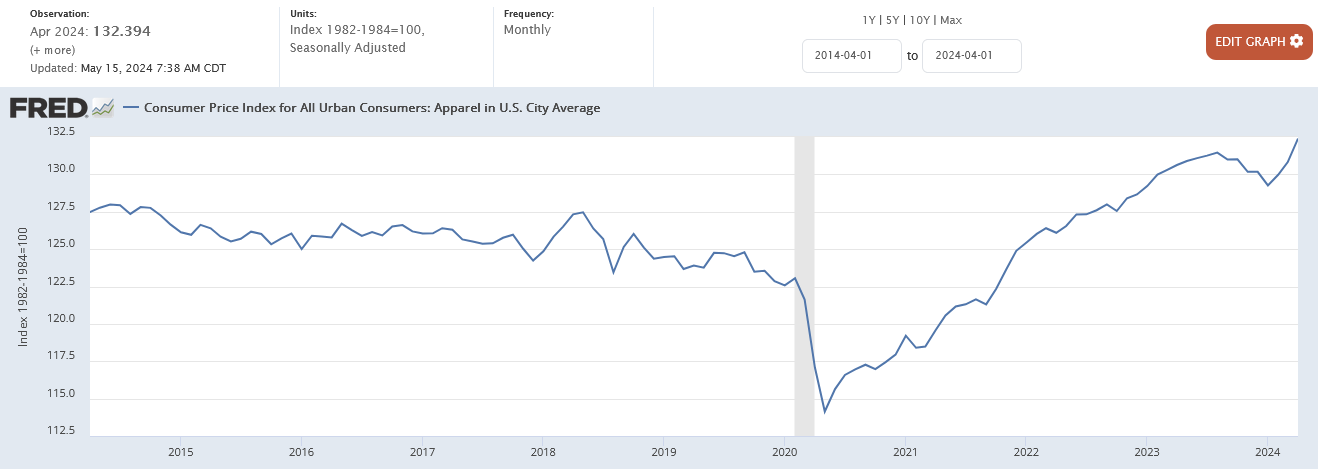

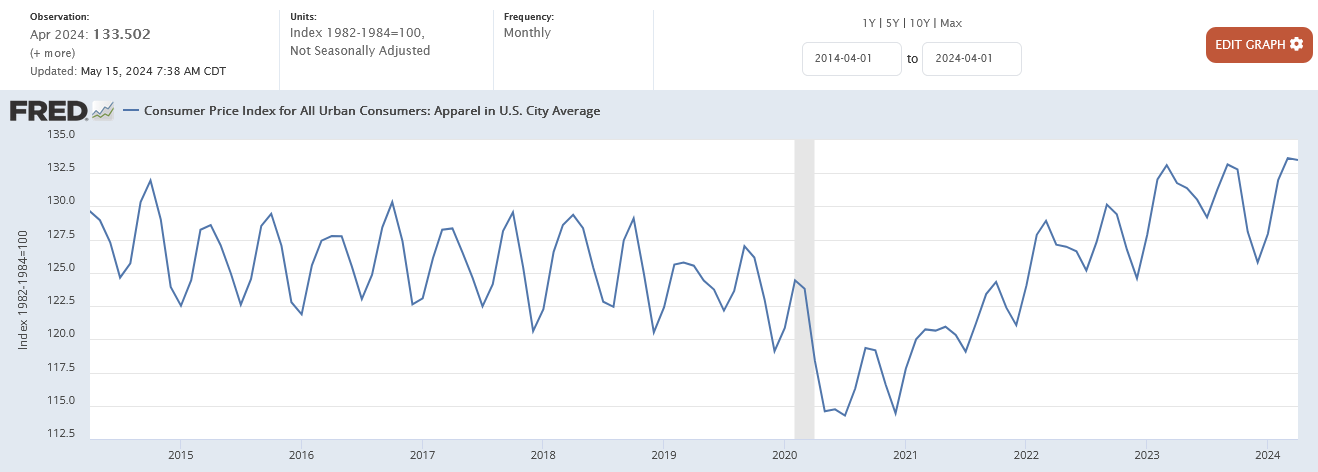

(3) Is there really genuine apparel inflation afoot? Judging from just the first four months of the year and the seasonally adjusted series of Apparel CPI, the answer would be most obviously yes.

But unlike OER, where seasonality is likely overestimated, Apparel seasonal dynamics are likely being underestimated (residual seasonality). It's possible much of the H2 deflation reflected this as well, but we are skeptical that the the last 4 months deserves extrapolation. Nominal spending and real consumption of apparel have been tepid to outright weak in recent months and quarters.

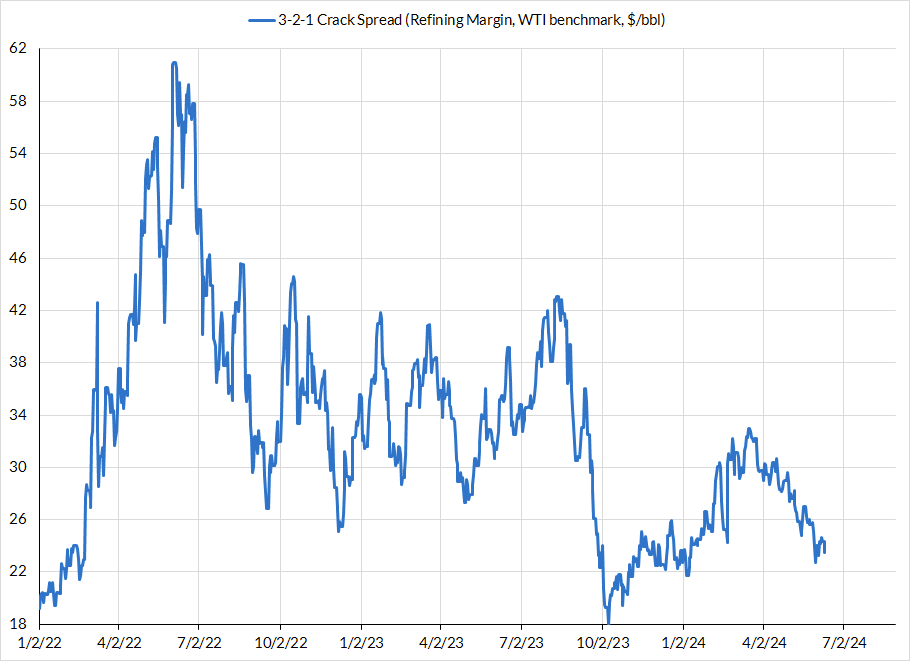

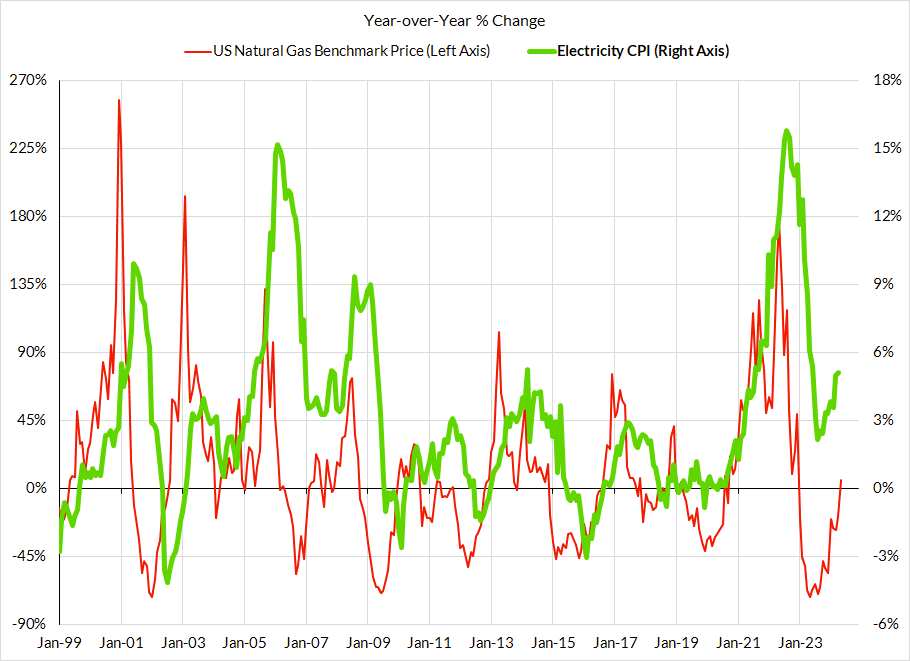

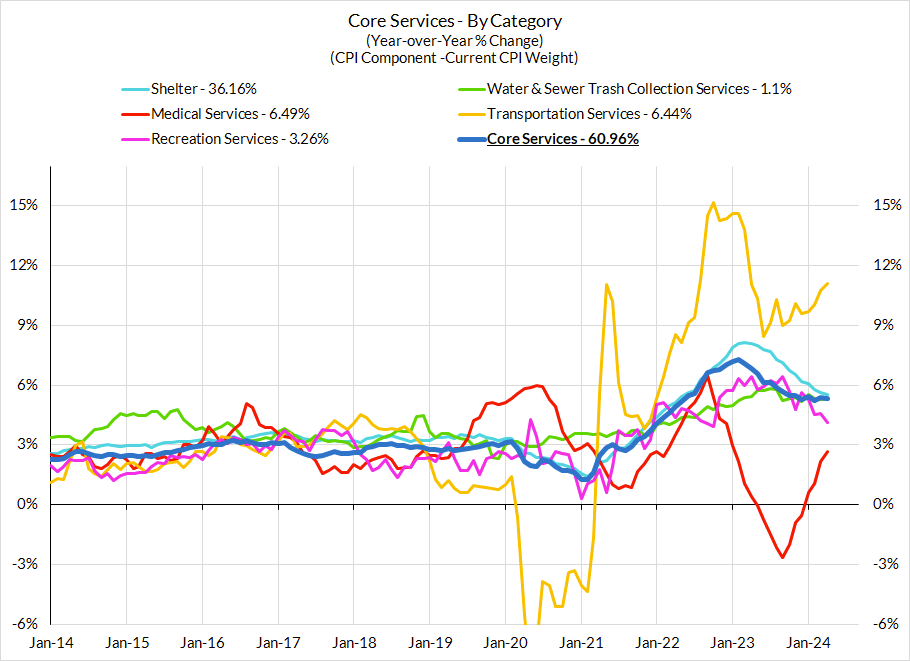

(4) Commodity price deflation and stabilization aids the Core Services PCE outlook. Falling energy prices do not just matter for headline measures of inflation. Two critical linkages flow to major segments of Core Services PCE: airfares & food services. Jet fuel prices staying stable with a bias to falling (as a result of falling refining margins) bodes well for airfares to remain in a stable price and inflation range. Diesel prices also showing more deflation has tangible benefits to food distribution costs, which enables grocery and restaurant prices to remain stable. While restaurant pricing is not a part of Core CPI, it is a major part of both Core and "Supercore" PCE aggregates. We expect to see more food services deceleration in the months ahead

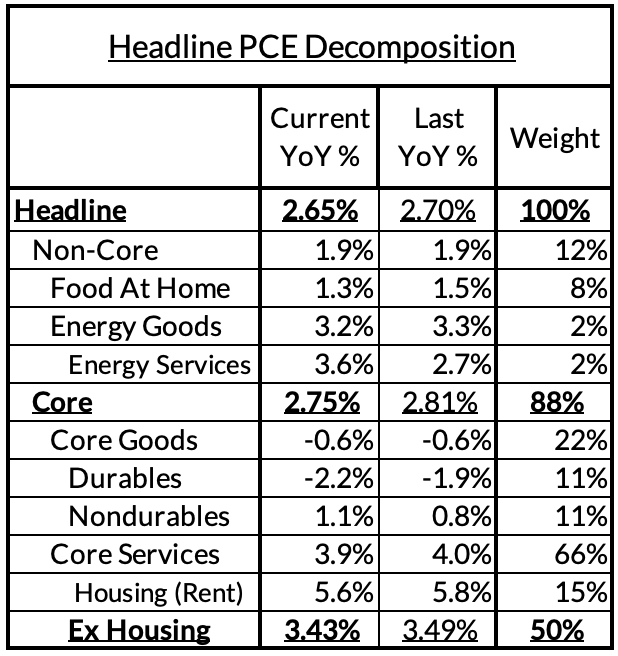

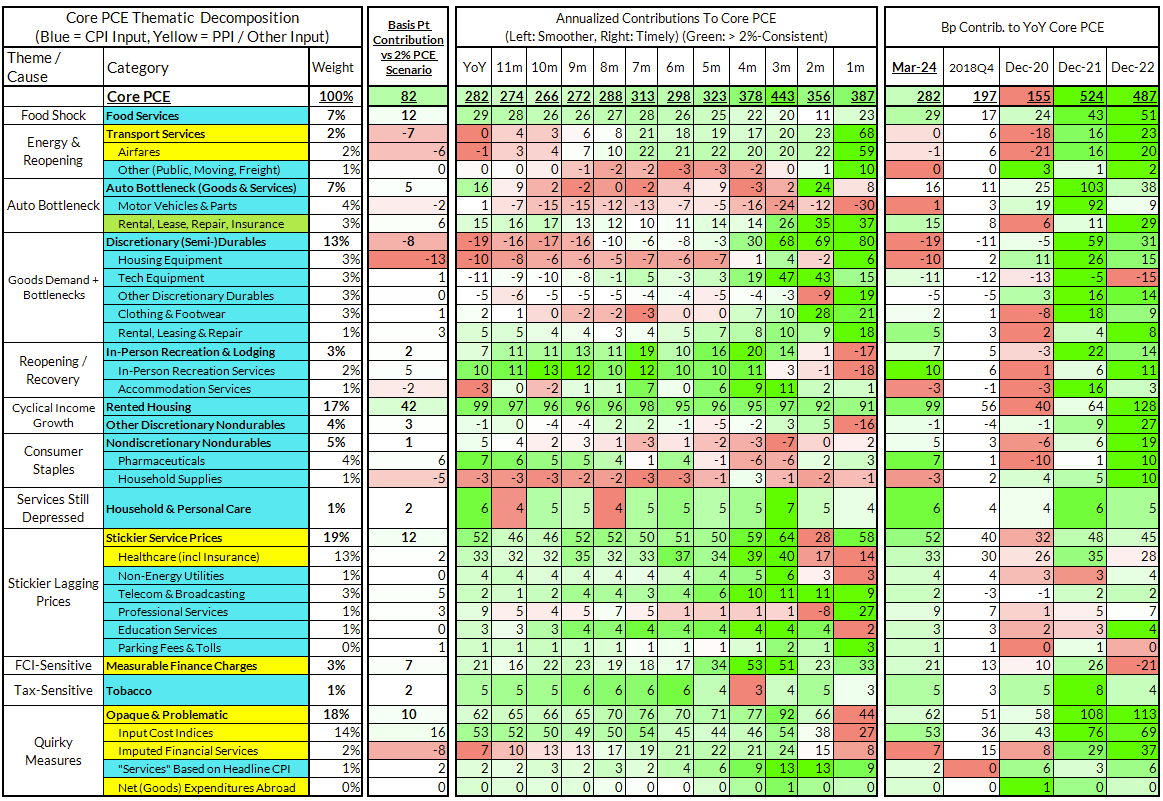

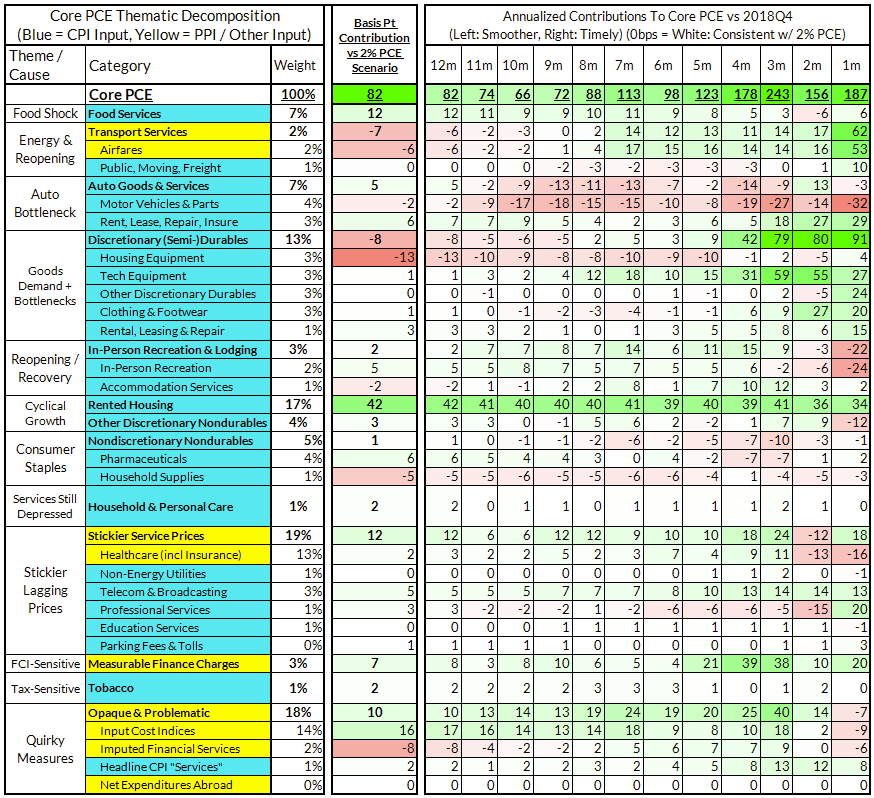

Core PCE (PCE less food products and energy) ran at a 2.82% year-over-year pace as of March, 82 basis points above the Fed's 2% inflation target for PCE. That overshoot is disproportionately driven by catch-up rent CPI inflation in response to the surge in household formation (a byproduct of rapidly recovering job growth) and market rents in 2021-22. Rent is contributing 42 basis points to the 86 basis point core PCE overshoot.

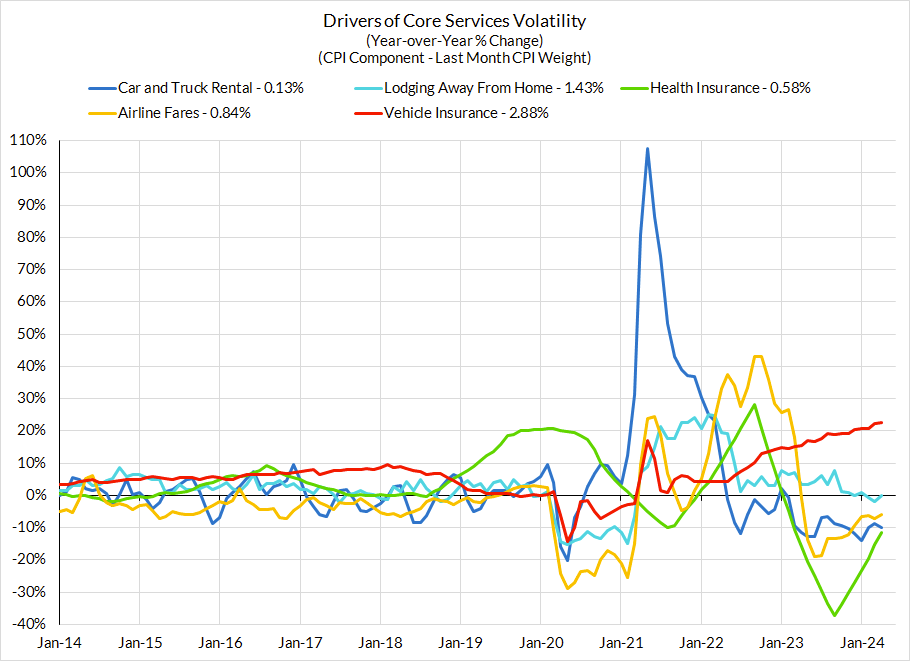

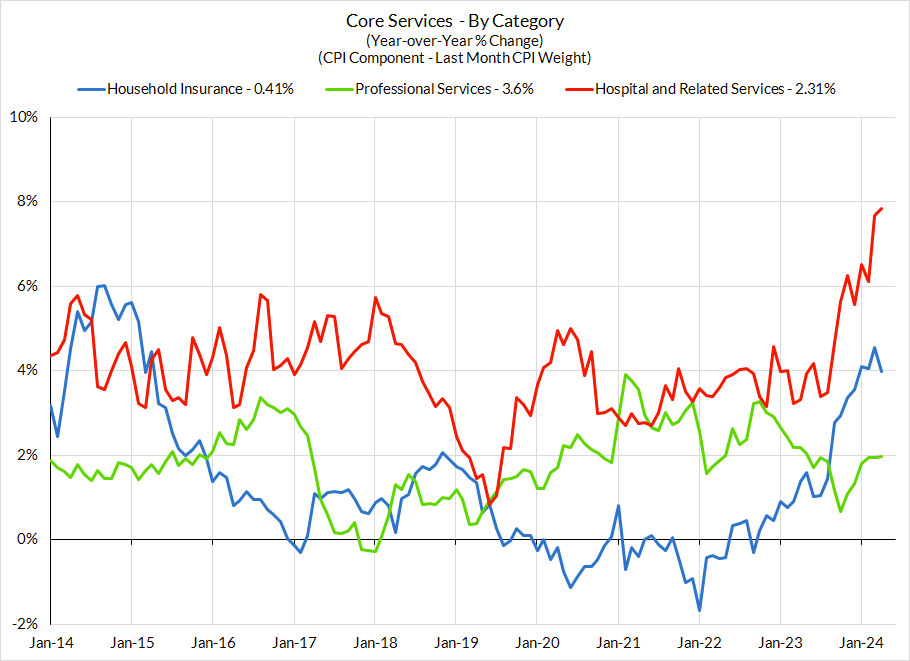

There are other contributors to the overshoot:

The final heatmap below gives you a sense of the overshoot on shorter annualized run-rates. March monthly annualized core PCE yielded a 187 basis point overshoot vs 2% target inflation (3.87% annualized).

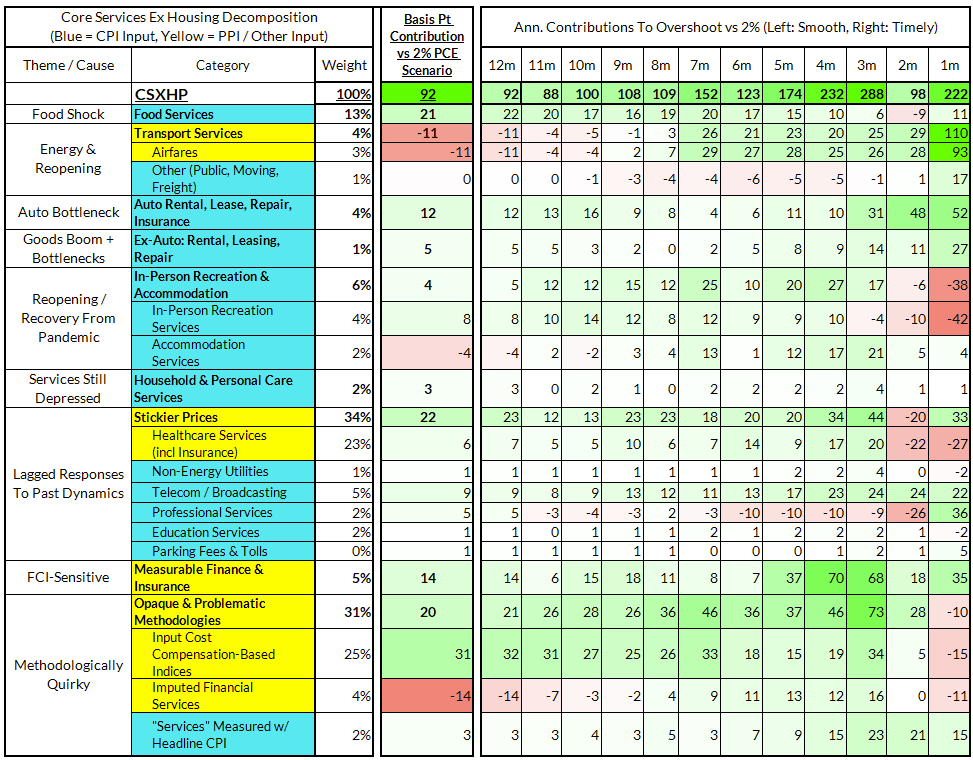

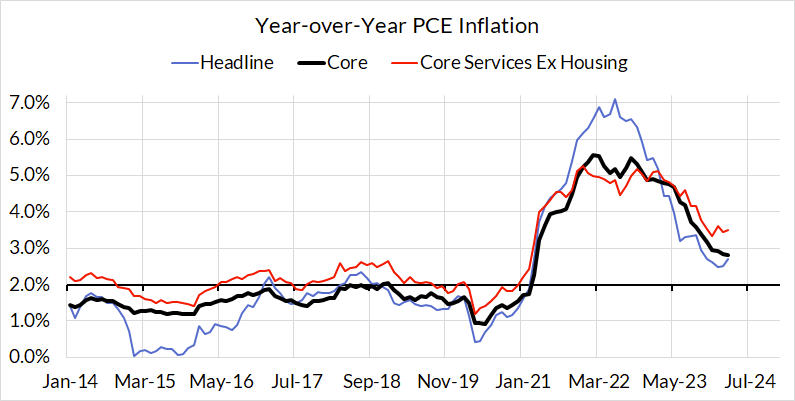

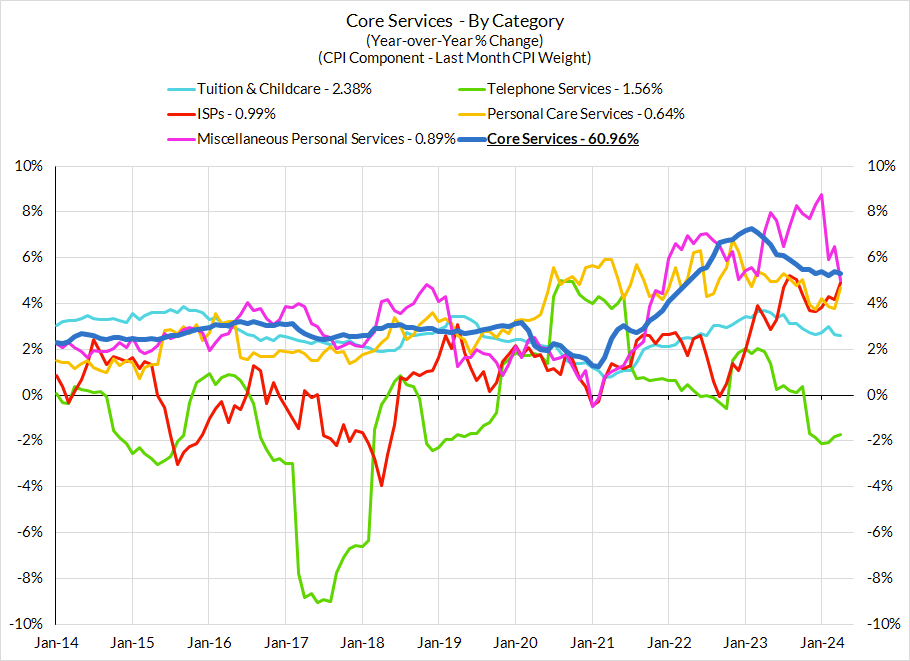

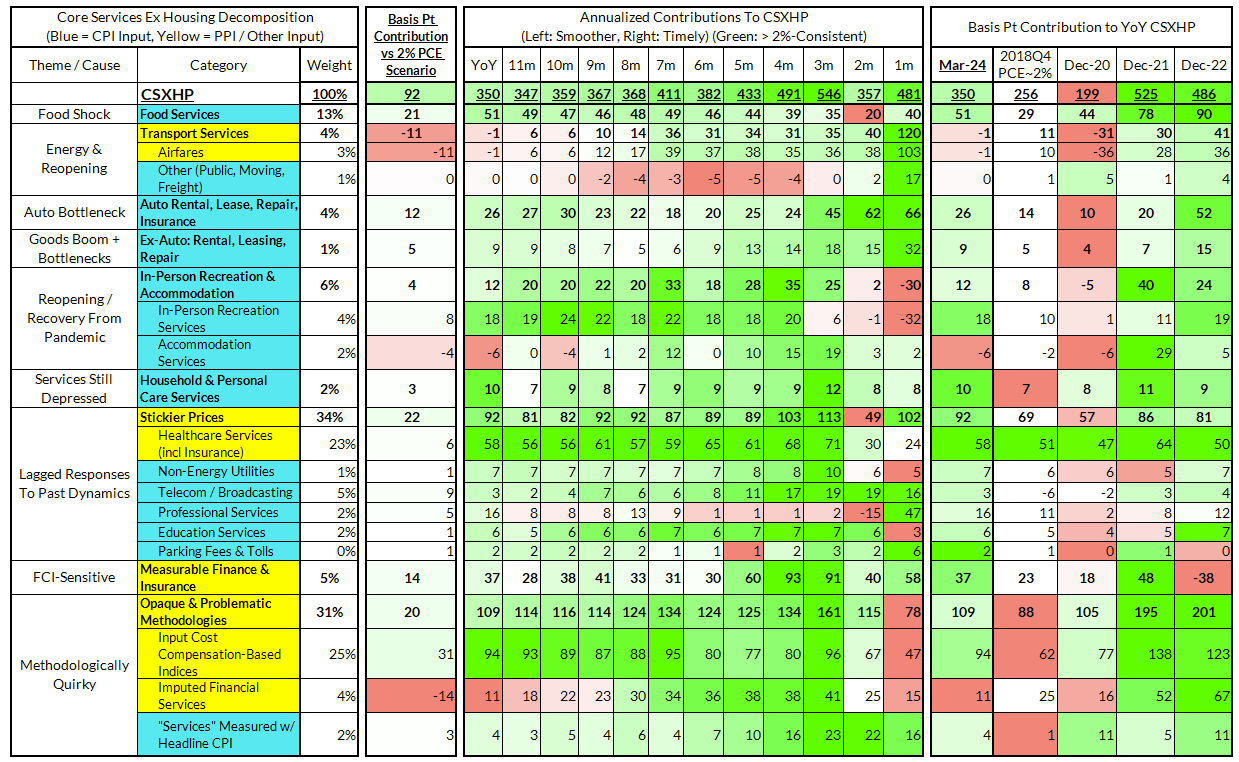

The March growth rate in "Core Services Ex Housing" ('supercore') PCE ran at 3.50% year-over-year, a 92 basis point overshoot versus the ~2.59% run rate that coincided with ~2% headline and Core PCE.

March monthly supercore ran ata 4.81% annualized rate, a 222 basis point annualized overshoot of what would be consistent with 2% headline and core PCE.